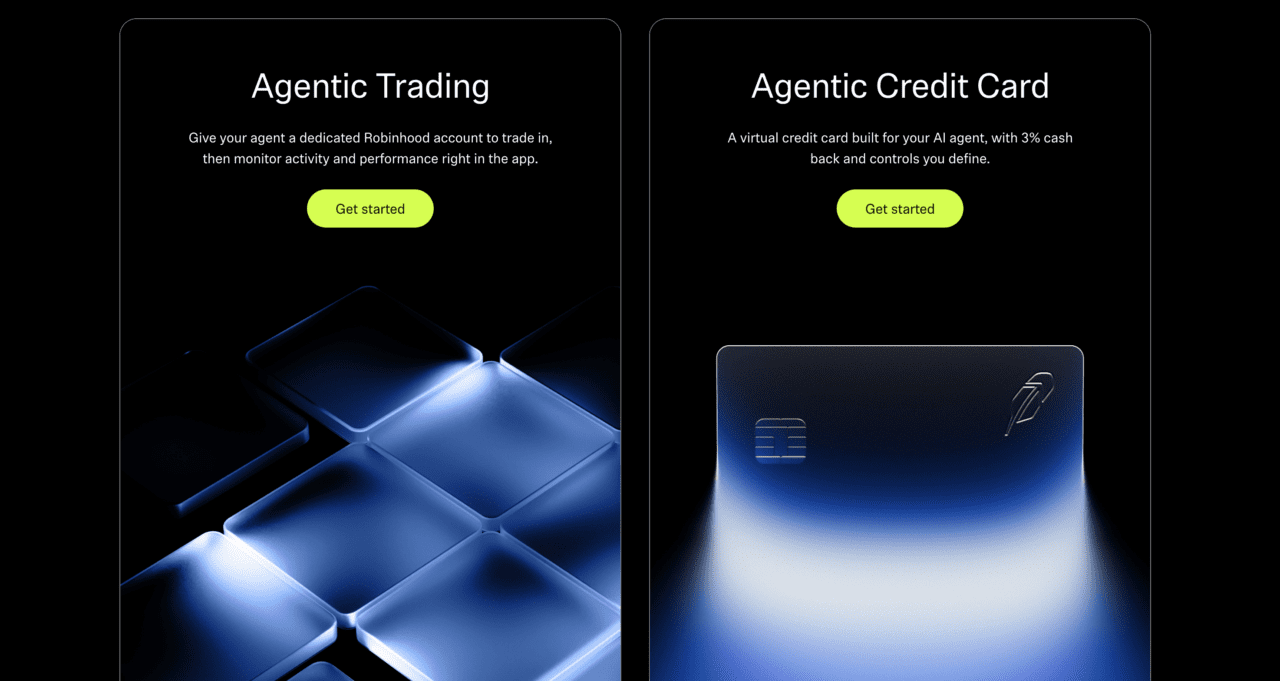

- Robinhood launched Agentic Trading and an Agentic Credit Card, enabling AI agents to trade stocks and make purchases directly on consumers’ behalf through Robinhood’s infrastructure.

- The new tools allow users to connect external AI agents via Robinhood’s MCP servers while maintaining guardrails such as spending limits, dedicated accounts, manual approvals, and real-time activity monitoring.

- The launch marks a major shift in financial services from AI as an advisory assistant to AI as an authorized participant capable of directly executing financial transactions and trades.

The agentic future is slowly becoming a reality in 2026. Ready for this reality, Robinhood is launching Agentic Trading and the Agentic Credit Card, which will allow AI agents to trade and make credit card purchases on consumers’ behalf.

While building agents is still not mainstream, the value they can bring to financial tasks is irrefutable. In the investing world, they can automate and execute a specific trading strategy and make trades faster than humans can. When it comes to payments, they can purchase scarce, limited release items such as concert tickets, sneakers, or flights to get the best price.

The new Agentic Trading and Agentic Credit Card tools allow users to give agents direct access to Robinhood without workarounds. Users can bring their agent from anywhere and connect them to Robinhood’s Model Context Protocol (MCP) servers to integrate seamlessly into Robinhood’s offerings.

Robinhood believes agentic finance will become an increasingly important interface for how consumers interact with financial services in the years ahead. “Our mission has always been to democratize finance for all, and now, that mission extends to AI agents,” said Robinhood CEO Vlad Tenev.

Robinhood’s new agentic trading tool allows users to open a dedicated agentic trading account separate from their traditional portfolio, which restricts agents to only access the funds available in that account. Robinhood sends users push notifications when the agent makes a trade and offers users a view of real-time trading activity. Robinhood’s Agentic Trading is launching today in beta and currently supports equities only with plans to support options, crypto, event contracts, futures, and more in the future.

The Agentic Credit Card allows agents to spend on consumers’ behalf by connecting them to Robinhood Banking’s MCP server. Cardholders can connect their agent to a dedicated virtual Robinhood Gold Card, set a specific spending limit, and choose whether or not to require manual approvals. Agents are restricted to that individual virtual card, with no access to the user’s primary credit card number or any of their account information. Agentic credit cardholders can set monthly limits, view their expense history, and have the ability to delete the virtual card at any time.

At launch, both agentic trading and the agentic credit cards are now available to Robinhood Gold cardholders, with plans to open it up to Robinhood Platinum cardholders when it launches later this year.

Any time agents are allowed to interface directly with financial accounts, there is risk involved. Because agent involvement in trading and payments is still new, there are no established consumer protection frameworks, dispute resolution standards, and clear liability structures for situations in which an AI agent acts outside of a user’s intent. However, Robinhood has proactively implemented manual approvals for purchases, trade previews when appropriate, and a fraud detection team to help users resolve disputes between what the user asked the agent to do and what it actually did.

This launch is notable in the financial services space. While both organizations and end consumers have typically used AI as assistants or for advisory purposes, leveraging agentic capabilities hasn’t gone mainstream until today. With Robinhood’s new launch, AI agents are now authorized participants in the financial ecosystem.