As hard as it is to believe, last year at this time only 30 financial institutions had apps in the U.S. iTunes App Store (note 1). And that was a full 18 months after Apple’s phone had opened its OS to third-party programs. A few in the industry still questioned whether smaller banks and credit unions would ever need a native iPhone app.

As hard as it is to believe, last year at this time only 30 financial institutions had apps in the U.S. iTunes App Store (note 1). And that was a full 18 months after Apple’s phone had opened its OS to third-party programs. A few in the industry still questioned whether smaller banks and credit unions would ever need a native iPhone app.

I think that question has been answered: In the past 12 months, the total financial institution app-count has rocketed upwards to more than 1,200, a 40-fold increase. That’s 100 new apps per month for the past 12 months.

In raw numbers, the past seven days have been relatively unremarkable with just 17 new FI apps. But it’s been one of the biggest weeks in terms of major launches:

- BofA Merrill Lynch research library for iPad only (note 4; iTunes)

- Capital One, whose app was released on Sunday, went to #5 Monday and is up to #4 when I checked a few minutes ago (see inset; note 2; iTunes)

- NetSpend (iTunes)

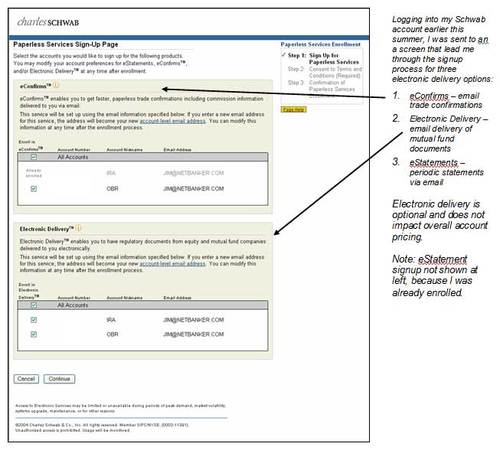

- Schwab, both v1 of its iPhone app (iTunes) and an iPad version of its On Investing magazine (iTunes)

- SmartyPig (pending Apple approval)

- Stanford Federal Credit Union, which used a striking background for its app home page (see below; iTunes)

And while it’s not nearly as crucial as the iPhone, we are waiting for a slew of iPad apps. Apparently, BBVA Compass demo’ed a cool unreleased iPad app at a mobile conference (note 4). And just today, Schwab released its monthly magazine in iPad format, an industry first.

And while it’s not nearly as crucial as the iPhone, we are waiting for a slew of iPad apps. Apparently, BBVA Compass demo’ed a cool unreleased iPad app at a mobile conference (note 4). And just today, Schwab released its monthly magazine in iPad format, an industry first.

——–

Notes:

1. See Online Banking Report #176, Table 18 (link subscription required)

2. Rank is of free apps in the Finance category in the U.S. store. The apps above it are #1 Bank of America, #2 Chase, #3 PayPal

3. HT David Eads in Mobile Manifesto

4. At the same conference as note 3, Bank of America revealed it hit the 6-million mark in active mobile banking users.

{kind=link}

{kind=link}

{kind=link}