This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

What challenges are small and medium-sized businesses facing when it comes to getting the capital they need when they need it? What role does technology – especially enabling technologies like automation and AI – play in helping make it easier for entrepreneurs and SMBs to access critical financing?

This week, Finovate VP and host of the Finovate Podcast Greg Palmer spoke with Marius Silvasan, CEO of eCapital, to discuss these and other issues important to small businesses and the financial services companies that serve them.

“SMBs in this current market are under pressure,” Silvansan explained in his Finovate Podcast interview. “They are challenged. And the reason behind that is we’ve come from an environment in which inflation is coming down, but has been high over the last year-and-a-half. We’ve come from an environment in which borrowing costs were near zero – and they’ve increased substantially over the last several years. And the labor market has been very tight, so it’s been tough for SMBs to hire, it’s been tough for SMBs to retain qualified personnel. So that’s made the environment for SMBs quite challenging over the several years.”

Headquartered in Miami, Florida, eCapital helps small and medium-sized businesses secure the financing they need in order to grow. Founded in 2006, eCapital offers a wide range of financing solutions including freight and invoice factoring, payroll funding, asset-back lending, equipment refinancing, and lines of credit.

What do you as an investor know about the people who manage your money? If your answer to this question is “not very much,” then imagine the challenge of banks and other financial institutions who invest millions of dollars with hundreds, if not thousands of investment professionals.

This is an underdiscussed problem in the investment world: the lack of systematic knowledge about the individuals and teams making investment decisions for millions of individuals, families, and organizations. This can lead to underperformance in terms of investments, as well as inefficient financial advisory.

To this end, we caught up with Thomas Oberlechner, CEO and founder of BehaviorQuant. The company he founded in 2018 gives financial institutions predictive information about the people behind investment decisions. BehaviorQuant leverages behavioral science, machine learning, and automation to learn and analyze the behavior of investment professionals and teams – as well as customers. The insights derived from BehaviorQuant’s automated survey technology enables fund managers to improve their performance and better customize their services to their customers.

Headquartered in Vienna, Austria, BehaviorQuant demoed its technology at FinovateEurope earlier this year.

What problem does BehaviorQuant solve and who does it solve it for?

Thomas Oberlechner: We developed BehaviorQuant because every financial decision is ultimately made by a person or a team. BehaviorQuant solves a core problem that underlies the entire investment industry: we don’t have systematic knowledge about the people and teams behind investment decisions. And that’s true for financial professionals and clients alike.

Financial players – for example, banks, funds, financial advisors – are used to having access to vast amounts of financial data and information. But without BehaviorQuant, they don’t have systematic knowledge and data about the people and teams behind this data. Yet it is the people and teams behind the visible financial results that play the key role in investing. You can see this everywhere — in the performance of investment teams, in the selection of fund managers, in the efficiency and success of wealth advisors.

For example, in our research we found that 37% of the performance of top decision makers at world-leading financial institutions is based on their behavioral characteristics. However, there is no product to easily measure and quantify the behavioral characteristics of decision-makers. This lack of insight into the behavioral aspects and decision-making tendencies leads to underperformance of asset managers, missed profit opportunities for investors, unrecognized fund manager selection risks, costly staffing mistakes, and churn among dissatisfied clients.

How does BehaviorQuant solve this problem better than other companies?

Oberlechner: Our behavioral finance technology combines the highest level of expertise in behavioral science, personality and decision research with machine learning. For the first time ever, we are capturing the people and teams behind the visible investment decisions. And we give our customers predictive knowledge about themselves and about others – about their own investment teams, about the fund managers they allocate their money to, about their clients. Our solutions solve three distinct problems: first, they help asset managers to improve their performance; second, they help allocators choose the best fund managers; and third, they enable advisors to tailor their advice highly efficiently to each individual client.

As we all know and often forget, markets are made up of people. And financial decision makers have very different ways of processing information, personalities, values, goals, and decision paths. Before BehaviorQuant, there was no systematic knowledge of these aspects. But it is exactly these aspects that are critical to how successfully you steer your course through the rough waters of financial risks and returns.

So BehaviorQuant enables you to efficiently personalize your client advice, optimize your investment decisions, and avoid invisible risks in capital allocation and manager selection.

Regardless of how experienced you are as a financial professional, you will always benefit from a system that gives you systematic, quantitative knowledge about people. Our clients receive predictive knowledge about asset managers, investment teams, and clients. And they make far better decisions — whether they want to interact more effectively with their clients, optimize their team’s decision-making, hire promising professionals, or select compatible external fund managers. BehaviorQuant effortlessly makes them a master of these tasks.

Who are BehaviorQuant’s primary customers. How do you reach them?

Oberlechner: The lack of knowledge about the actual decision makers is pervasive, and it affects three kinds of financial companies in particular. These companies are also our main customers. First, we work with financial companies and asset managers who actively invest in the markets and who want to optimize the returns they generate by improving their own decision processes. Second, we work with family offices and other allocators who use BehaviorQuant to evaluate and select fund managers. And thirdly, we cater to banks and investment advisors who want to excel in advising their clients. They want to advise in a highly personalized way that is truly aligned with their clients.

How do we reach these customers? We’re proud that our first clients found us, not the other way around. Of course, in the meantime, we have grown our sales and marketing team and expanded our outreach efforts by maintaining an active presence on social and other media and attending of relevant conferences — like Finovate. And we’re finding that word of mouth from customers who love our solutions is increasingly supporting our efforts to win new customers.

Can you tell us about a favorite implementation or deployment of your technology?

Oberlechner: We have been receiving enthusiastic feedback from users on both sides of the Atlantic. It makes me and the team happy when they tell us that BehaviorQuant should be a mandatory tool in any decision-making process, when they emphasize how BehaviorQuant’s solutions help them to make better decisions in a systematic and sustainable way, and when they express their enthusiasm about how it helps them deepen their customer relationships.

But my personal favourite deployment of our technology is something that has only very recently come to market. It allows us to impact many more customers without them having to contact our friendly sales team first. Just in time for the 2023 fall season, we’ve introduced an all-new, self-service option for our financial and wealth advisors. They can now effortlessly get detailed information on our website and actively try out BQ Advisory. Then they can purchase single product uses for their work with clients. They can do this directly on the website, on a credit-by-credit basis. This self-service option and the ability to join on a credit basis alongside our attractive licensing offerings have made the of BQ Advisory much easier, especially for the many independent advisors who advise a limited number of clients. And it’s also great for advisors in large institutions who use us already and now want to easily show their colleagues what BehaviorQuant can do.

What in your background gave you the confidence to respond to this challenge?

Oberlechner: I was initially trained as a clinical psychologist in Vienna and always have been fascinated by the differences between people and the way they make decisions. As a university professor for many years, I have focused on how people actually make financial decisions — and the fact that we are all different financial decision makers. I have been fortunate to work with dozens of the world’s leading financial institutions for my research, from Goldman Sachs to Merrill Lynch to UBS. My female cofounder, Dr. Gerlinde Berghofer, and I both have PhDs and strong backgrounds in behavioral science. We have spent years doing research at Harvard, MIT, and Columbia University. We have worked with and studied hundreds and thousands of investment decision makers, from top fund managers to banks, advisors, and financial clients. From academia, we moved first to Silicon Valley and now to Vienna to translate this research into turnkey behavioral technologies for investment professionals.

Our solutions are therefore based on our many years of scientific work with many of the world’s leading investment institutions. And we have gone to great lengths to empirically test their benefits. For example, we have systematically tested the predictive power of BQ Performance with professional portfolio decision makers. While their average annual performance was about 10%, the annual performance of those whom the system predicted would outperform was more than twice as high. To give another example, in a comprehensive study of wealth advisory clients, BQ Advisory identified clients at risk of churn with 90% accuracy. Compare this to the 50% accuracy without BehaviorQuant!

Left to right: Dr. Thomas Oberlechner (CEO, Founder) and Gerlinde Berghofer (COO, Co-founder) of BehaviorQuant at FinovateEurope 2023.

What is the fintech ecosystem like in Austria? What is the relationship between techs, fintechs, and traditional financial services companies?

Oberlechner: Austria and Vienna have proven to be a fertile breeding ground for the specific type of fintech that BehaviorQuant offers. Vienna historically has played a large role in the sciences that generate a better understanding of individual and collective behavior, from Freud’s psychoanalysis to the Austrian School of Economics. After spending many years in San Francisco developing fintech, we felt very fortunate that the Austrian government offered us a generous grant to bring BehaviorQuant here.

I would describe the fintech industry as friendly and highly innovative, with some already well-known international players with roots in Austria like n26 and Bitpanda. Collaboration between traditional financial institutions and fintech startups has been a major driver of innovation in the Austrian market. Established banks are turning to fintech partnerships to expand their service offerings, improve the customer experience, and stay competitive in the digital age. Vienna has become a bit of a fintech hotspot, attracting both local and international talent and investment. Fintech companies benefit from Vienna’s consistently high rankings in international surveys of capitals’ attractiveness. The city offers an ecosystem of co-working spaces, incubators, and accelerators that foster collaboration and help fintech startups succeed.

At BehaviorQuant, we maintain close personal relationships with many of Austria’s “traditional” financial firms and banks, and we also have a very active bridge to the U.S. based on our history and our strong network on both the East and West coasts.

You demoed at FinovateEurope in London earlier this year How was that experience?

Oberlechner: Wow! We are absolutely thrilled by the incredible response we’ve received for our products! The interest and the number of new connections we’ve made were really overwhelming. We received amazing support from the organizers throughout the conference, as well as during in the preparation stage for our participation and presentation. The feedback from participants gave us an incredible boost of confidence and motivation. Thanks again to the team for a great and wonderfully rewarding experience!

What are your goals for BehaviorQuant and what can we expect in the months to come?

Oberlechner: Our goal with BehaviorQuant is simple: we want financial decision makers around the globe to become better decision-makers though our systematic behavioral data and decision support. And we want to become the world’s leading provider of predictive behavioral data for financial professionals and investment companies.

I briefly mentioned that we recently launched a self-service payment option for our advisory solution. In the coming months, exciting new self-service options are in the queue for the analysis of financial professionals with BQ Performance. This will allow individual investment professionals to easily get started with a comprehensive analysis of their personal untapped performance potential, as well as possible behavioral bias and performance blockers — before using it in the wider context, for example, with their entire team or company. So stay tuned for our upcoming releases!

How can greater transparency in financial services help improve underwriting, lower risks, and create more opportunities for banks and small businesses alike?

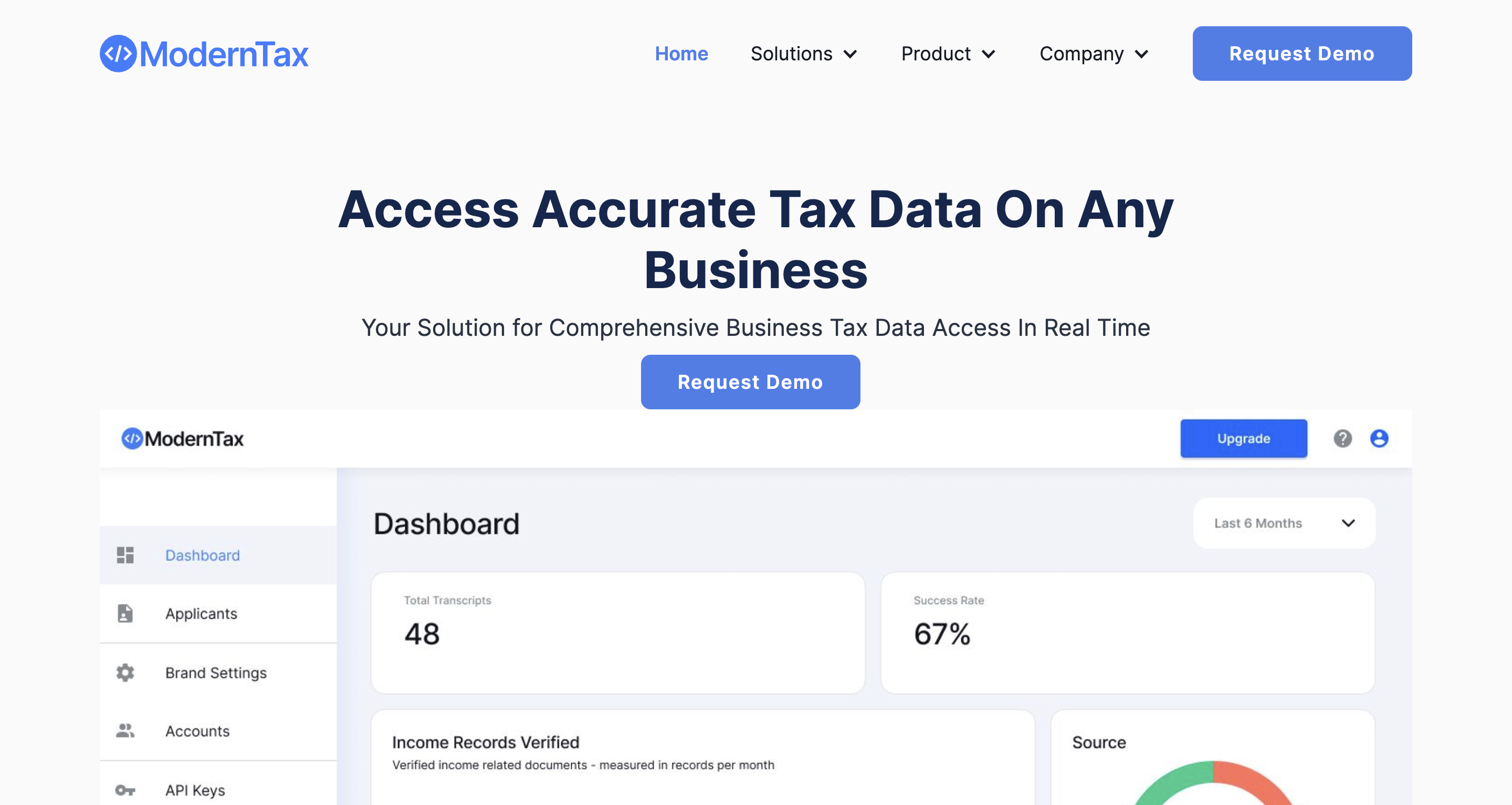

We caught up with Matthew Parker, founder and CEO of ModernTax, to discuss how bringing more transparency to areas of finance like taxation can help credit providers make better decisions.

Founded in 2021 and headquartered in San Francisco, California, ModernTax made its Finovate debut earlier this year at FinovateSpring. At the conference, the company demoed its Business Verification Platform and Verifier API, a secure solution that enables fintechs and banks to verify tax records, business standing and KYC data.

Last month, ModernTax launched its Live Contributory Network for on-demand tax verification. The solution connects licensed tax professionals with ModernTax customers to provide on-demand, secure, and reliable tax verification services.

To start off, what is it about taxes that interests you? Of all the areas of finance, what’s special about taxes?

Matthew Parker: My first job out of college was in social services, specifically working in child support. My responsibilities included calculating the combined income of two people with misaligned incentives. This experience opened my eyes to how broken the world of tax, income, and finance can be at the ground level.

A few years later, I worked in consulting, helping banks understand what went wrong with the mortgage crisis. I then stumbled into my first entrepreneurial endeavor: a franchise tax preparation company. Over three years, I grew from one office to five and learned the ins and outs of the tax preparation business.

In 2017, I caught the technology bug and bought a one-way flight to San Francisco with the goal of starting a tax startup that utilized all of the tax data I had been accessing through my tax preparation business as alternative data to underwrite loans.

Six years later, I am building ModernTax to make use of this data to help underwrite, decrease risk, and create a more transparent financial ecosystem for U.S.-based small businesses.

Can you elaborate on that?

Parker: One thing that has consistently bothered me is the black box of tax information that lives outside of our bank feeds and accounting feeds. There is an entire business that helps accountants export accounting data into tax software (they are a customer), but that is a niche market.

The real problem we are solving is financial transparency. Many businesses that provide financial services are locked out of access to critical financial records, and 99% of U.S. businesses are not required to report any financials. This results in a massive transparency gap. Tax records are one way to fill this gap, with 15 million unique entities and 160 million individual tax returns filed annually in the U.S. alone.

How does ModernTax solve this problem better than other companies, or other solutions?

Parker: ModernTax aims to solve the problem of financial transparency by providing tax information on all U.S. small businesses, which can level the playing field and create a more transparent financial ecosystem. The commercial credit market in the U.S. alone is worth $8.8 trillion annually, and the average company in this industry generates approximately $7 billion in yearly revenue.

By utilizing tax records, which are filed by 15 million unique entities and 160 million individuals annually in the U.S. alone, ModernTax’s strategy revolves around transparency and eliminates the need for countless hours of back-and-forth communication and manual data entry to collect this information, saving commercial providers time and money, and making it easier to evaluate businesses.

What is your primary market? What has the response to your technology been like?

Parker: We primarily sell to commercial credit providers such as banks, online lenders, and other data providers that assist companies in underwriting, fraud prevention, and verifying financial documents for their customers.

We have received positive responses from data providers such as D&B, Experian, and Transunion, as well as from our first paying partner, Enigma Technologies. Moreover, ModernTax has been well-received by direct carrier insurance companies for both underwriting and claims processing on income-related products.

Are there any deployments or features of your technology that are especially noteworthy?

Parker: In the past month, we have added 14 new features. One notable observation is the need for a robust platform that allows our contributors to efficiently provide us with data. Unfortunately, the IRS does not provide adequate tools to help companies maintain transparency in their reporting. We are constantly learning from our contributors on how we can build tools to address this issue.

ModernTax is headquartered in San Francisco and was founded in 2021. What is it like to be a young startup in San Francisco today?

Parker: Personally, it feels surreal to me. I moved to San Francisco in 2017, lived through the pandemic, and experienced the boom of 2021 and the correction of 2022. Nevertheless, San Francisco is resilient. Although there are political and socioeconomic problems that come with being a high-stakes, high- reward city, founders can arrive here with nothing and become paper billionaires and liquid millionaires faster than anywhere else in the world.

This creates a tale of two cities. To be a young startup, you have a ton of resources right in your backyard, but you also realize how competitive it is. There was a new billion-dollar company born every day for a certain amount of time and now, with AI, we are seeing history repeat itself. It’s important to keep your momentum but also not get too distracted.

We also wanted to talk with you as a Black founder and entrepreneur. What advice would you give to other potential founders-of-color?

Parker: Starting a company is hard, full stop. I even joke with my wife that I don’t mind telling my 18-month-old son “no” a lot because it’s just the nature of life in general. As a black founder, I have experienced both ups and downs. George Floyd’s murder created a domino effect of predominantly white people at large institutions feeling guilty, which led to a lot of initiatives that were half-baked and more PR moves than anything. That sentiment wore off pretty quickly, especially as markets turned for the worst in 2022.

If you built your brand “how hard it is to be a black founder”, you are likely bitter right now because we learned that the market didn’t care about you being black or about what happened with George Floyd. We are now seeing pushback with the rollback of affirmative action, the lawsuit impacting Fearless Fund, and I think more challenges will come. So, I would say focus on your business, focus on your customers, and build products. If you play the victim in a game that is already hard, you decrease your chances of winning.

You demoed your technology at FinovateSpring earlier this year. What was that experience like for you and your team?

Parker: This demo helped us think about how our product helps financial institutions and we were able to demonstrate the capabilities that companies can experience by getting access to this information in real-time.

What are your goals for ModernTax? What can we expect from the company over the balance of 2023 and into next year?

Parker: ModernTax aims to provide near-instant access to verified tax and financial information through a network of licensed tax agents to create a more transparent verification process for their customers. Over the balance of 2023 and into next year, the company plans to add eight new customers, launch new features for its contributor portal and business user features, and attend various business development events and in-person client meetings.

Will 2023 be known as the year AI came of age? With the advent of Generative AI and tools like ChatGPT, the technology world got an unexpected boost this year as interest in the potential for artificial intelligence soared.

What does the surge in interest and activity in AI mean for financial services? How can fintechs leverage the technology to help banks, credit unions, and other financial services organizations and institutions better serve their customers with more choice, more security, and more efficiency?

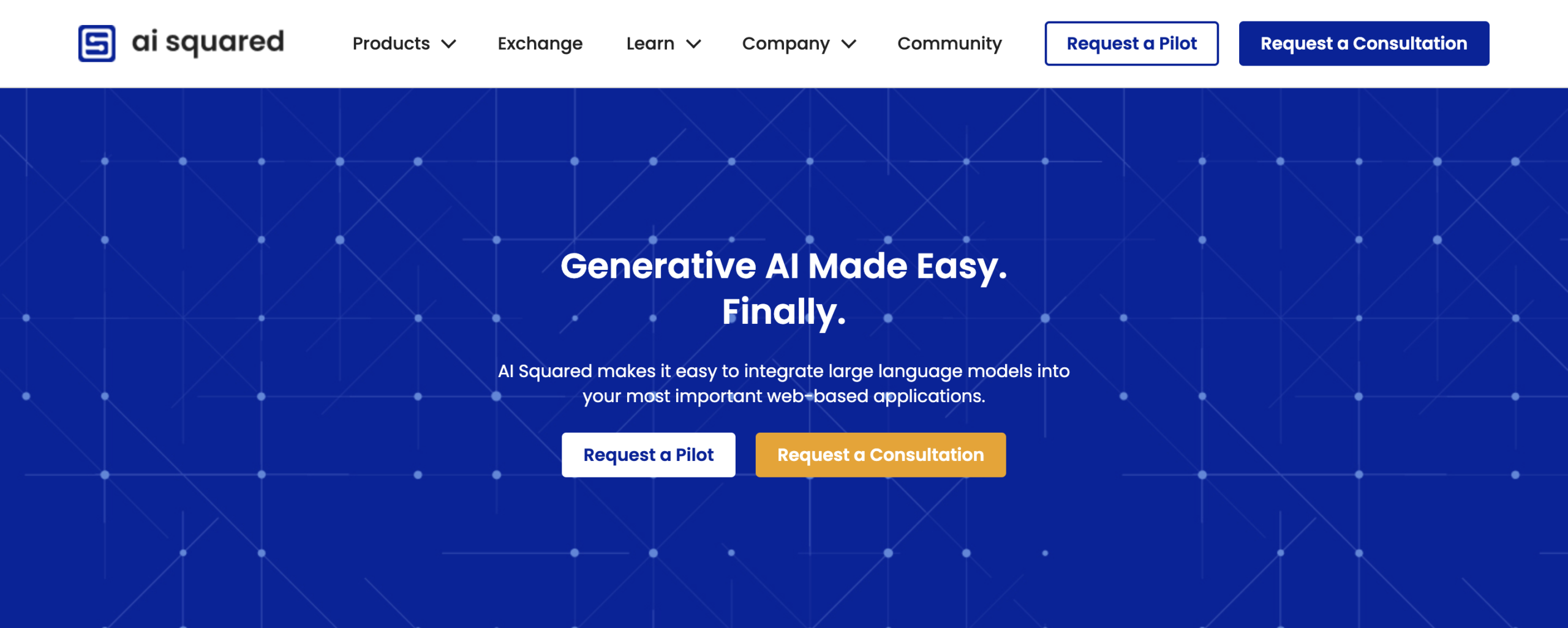

We caught up with Dr. Benjamin Harvey, founder and CEO of AI Squared. Headquartered in Washington, D.C., AI Squared made its Finovate debut earlier this year at FinovateSpring and will return to the Finovate stage next month for FinovateFall. The company specializes in integrating artificial intelligence and machine learning into existing apps. We discussed the rise of AI, the impact AI might have on financial services, and the work of AI Squared in helping businesses take advantage of the emerging technology.

We also talked about the challenges Harvey has faced as an African American entrepreneur and founder in the technology industry. As we commemorate Black Business Month here in August, we are also happy to share his insights and advice on what African American founders and entrepreneurs need to keep in mind when starting out.

Let’s start with a big picture question: what is overhyped about AI, what’s underhyped, and what are we getting right?

Benjamin Harvey: There’s a lot of hype around AI, and some of it is warranted, but not all. One of the most overhyped ideas is that AI will replace humans in the workforce on a large scale. While AI can automate certain tasks, it can’t replicate the creativity, empathy, and critical thinking that humans bring to the table. On the flip side, what’s underhyped is the potential for AI to be simple while being useful. Many AI products have incredible potential but are too complicated for widespread adoption. Simplifying AI and making it more accessible can unlock its true potential and bring about transformative change across industries.

What most observers and commentators are getting right about AI is that it’s here to stay. AI is not just a passing trend; it’s a technological revolution that’s reshaping the way we live and work.

Now let’s turn to your company. What problem does AI Squared solve and who does it solve it for?

Harvey: AI Squared is a platform designed for product owners, data scientists, and enterprise leaders. We empower users to accelerate both predictive and generative AI projects, measure their benefits, and drive significant revenue growth and cost reduction. Our solution is industry-agnostic and loved by our users.

We address a critical issue in the AI industry: 90% of AI and ML models never make it into production or use, largely due to the time and cost involved. AI Squared tackles this problem head-on, reducing the time to production and use of AI and ML models from an average of 8 months to 8 hours or less. We provide a secure environment for accelerating AI projects, enabling users to measure benefits, use no/low code solutions, and deliver trustworthy AI results. By streamlining the AI deployment process, we help organizations harness their data to drive game-changing AI capabilities, driving innovation and growth.

How does AI Squared solve this problem better than other companies, other solutions?

Harvey: We understand that the key to successful AI adoption is seamless integration into existing workflows. Our solution is designed to fit effortlessly into the applications that our customers already use on a daily basis. By embedding AI capabilities directly into these familiar tools, we eliminate the need for users to switch between different platforms, thereby reducing friction and increasing efficiency. This approach not only enhances the user experience, but also drives greater AI adoption across the organization. Our technology is versatile and accessible, making it a valuable asset for teams at all levels, from operational staff to executive leadership. The result is a more informed, agile, and productive organization that can leverage AI to its full potential.

What is your primary market? What has their response to your technology been like?

Harvey: Our primary market is financial services and the response has been overwhelmingly positive! Financial services organizations are constantly seeking ways to improve efficiency, reduce costs, and enhance customer experiences. And our platform has been proven to address these needs by accelerating the deployment of AI and ML models, making it easier for these organizations to harness the power of their data.

When clients see how we can reduce AI implementation from 8 months to 8 hours they’re blown away. We’re proud to say that we’ve turned our clients into our biggest champions. The value we provide goes beyond just the technology; it’s about the tangible benefits that our platform brings to their operations. They appreciate the speed at which they can now bring AI projects to fruition, the ease of integration with their existing systems, and the measurable ROI that our platform delivers.

Are there any deployments or features of your technology that are especially noteworthy?

Harvey: First and foremost, we prioritize data security and privacy. Unlike many other AI platforms, we don’t store or copy our customers’ data. This is a crucial differentiator, especially for organizations in highly regulated industries like financial services, where data privacy and security are paramount.

We offer flexible deployment options to suit the specific needs of our customers. Our on-premises deployment ensures that all data remains within the customer’s own infrastructure, providing an added layer of security. For those who prefer a cloud-based solution, we offer a multi-tenant deployment that still maintains robust data privacy and security measures.

One of our standout features is our Human-in-the-Loop (HITL) capability. This feature allows human verification and corrections to be made to the data generated by Generative AI before it’s used in critical business applications. This ensures a high level of accuracy and reliability in the data, which is essential for making informed business decisions. Our HITL feature is particularly valuable for organizations that need to ensure the utmost accuracy in their AI-generated data, such as those in the financial services sector where even small errors can have significant consequences.

You and many of your team have significant backgrounds in academia and the government. How has the transition into a more entrepreneurial space been?

Harvey: The transition from academia and government to the entrepreneurial space has been both challenging and rewarding. Initially, it was a bit of a culture shock to shift from a focus on the technical aspects of AI to a more value-driven approach. In academia and government, the emphasis is often on the theoretical and technical aspects of AI, whereas in the entrepreneurial space, the focus is on delivering tangible value to customers.

But once we got past the initial adjustment, we found that our diverse backgrounds gave us a unique perspective and a competitive edge. While our experience in academia has equipped us with a deep understanding of the technical intricacies of AI, our government experience has given us insights into the importance of security and compliance, especially when dealing with sensitive data.

We’ve been able to leverage these insights to develop a platform that not only delivers powerful AI capabilities but also addresses the specific pain points and challenges faced by our customers. Our approach is rooted in a deep understanding of both the technical and practical aspects of AI, and we’re able to offer solutions that are tailored to the unique needs of each customer.

Left to right: AI Squared’s Benjamin Harvey, Alvin McClerkin (COO), and Michelle Bonat (CTO) at FinovateSpring.

We also want to showcase AI Squared as part of our Black Business Month commemoration. What challenges have you faced as a Black founder and entrepreneur? What advice would you give?

Harvey: Launching a company as a Black entrepreneur, particularly in the AI/technology space, comes with its own unique set of challenges. One of the most significant hurdles is the lack of resources and representation in the industry. As a Black founder, I often found myself navigating uncharted territory without the benefit of a robust network or role models to look up to. However, I believe that these challenges can be overcome with determination, persistence, and a strong support system.

My advice to aspiring Black tech founders is to build a solid network of mentors, advisors, and peers who can provide guidance and support along the way. Don’t be discouraged by setbacks or rejections; instead, use them as learning opportunities to refine your approach and strategy. Do your homework, stay informed about industry trends, and be prepared to articulate the value proposition of your technology clearly and convincingly. Most importantly, reach out to other Black founders and executives who have walked the path before you. Their insights and experiences can be invaluable as you navigate the complexities of the tech startup ecosystem.

Remember, you are not alone in this journey. There is a growing community of Black tech founders and professionals who are eager to support and uplift each other. By working together, we can break down barriers, create more inclusive opportunities, and pave the way for future generations of Black tech entrepreneurs.

Speaking of African-Americans, AI Squared is headquartered in Washington, D.C. What is the technology scene like there?

Harvey: D.C. is a hotbed of tech innovation, especially in security and intelligence. Being close to the Federal Government and defense agencies, we’re in a unique spot to work on projects that matter for national security. It’s a vibrant scene here, with big tech firms, cool startups, and research hubs all mixing it up. We’re a tight-knit community, always meeting up, sharing ideas, and pushing each other to innovate.

The best part is that if your tech is good enough for national security, it’s good enough for anything. We’re talking finance, healthcare, consumer goods – you name it. Being in D.C. gives us the credibility to branch out into these sectors. It’s an exciting place to be, and we’re happy to be part of it.

You demoed your technology at FinovateSpring earlier this year. What was that experience like for you?

Harvey: The experience of demoing our technology at FinovateSpring was exciting and valuable for us. It provided us with a unique platform to showcase our product to a large audience of stakeholders, and to connect with key decision-makers in the financial services industry. We got valuable feedback on our product.

But the demo wasn’t without its challenges. Some technical difficulties with signing in and that, combined with the strict time constraints of the event, impacted our demo. These are things that tend to happen when demo-ing in a new forum. But it’s in our DNA to adapt and we did – and received positive feedback from attendees and made valuable connections that have since led to fruitful discussions. Overall, the experience was a great opportunity for us to showcase our technology, connect with industry leaders, and learn from the challenges we faced.

What can we expect from AI Squared over the balance of 2023 and into next year?

Harvey: Our primary goal for AI Squared is to continue delivering exceptional value to our customers, with a focus on the financial services sector. We’re committed to optimizing our product to enhance the customer experience and build strong, lasting relationships. As we approach the end of 2023, we are on track to exceed our internal goals, thanks to the dedication of our team.

Looking ahead to next year, we have ambitious plans for growth. We’re preparing to raise our next round of funding with a strategic team of investors who share our vision. This funding will enable us to continue providing world-class service and products. We’re also planning to expand our product offerings and explore new markets. We are excited about the opportunities that lie ahead and look forward to sharing our progress with you!

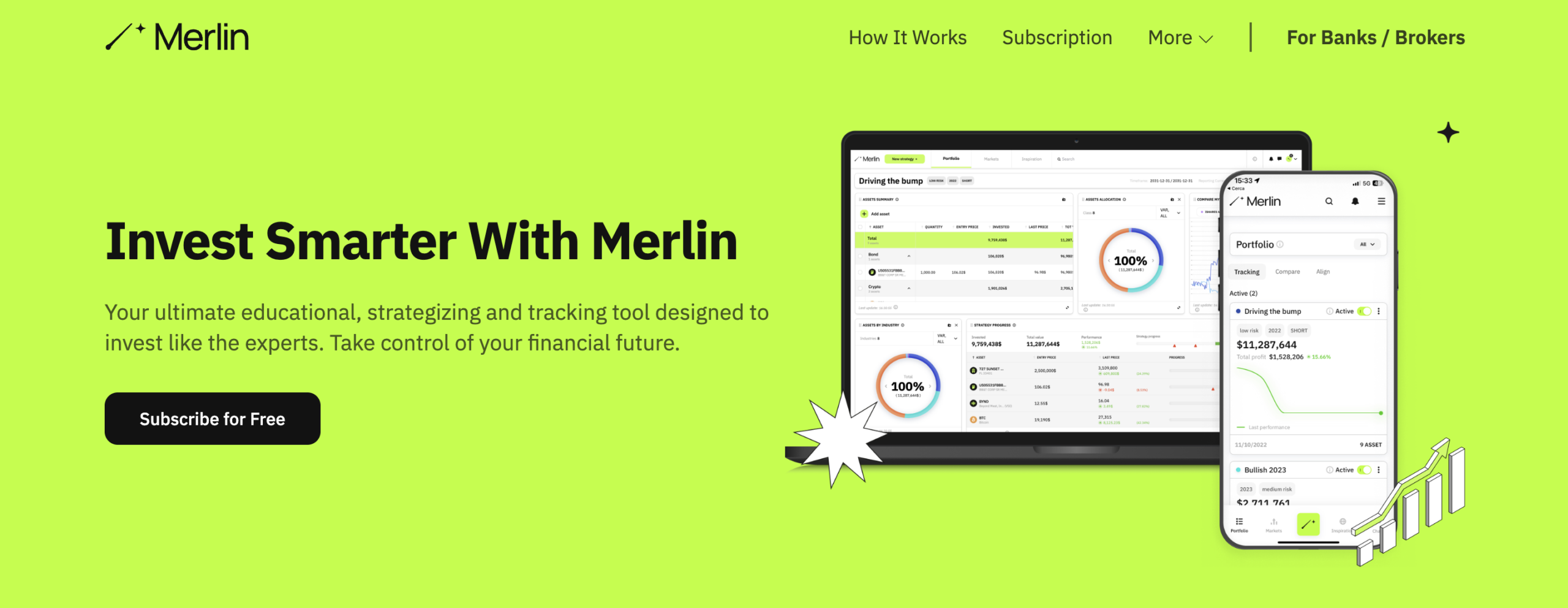

Launched in the fall of 2021, Merlin Investor is on a mission democratize access to investment strategies. The fintech offers a while label, multi-asset, educational, strategizing and tracking tool that helps investors accomplish two critical goals: building long-term positive results and limiting potentially catastrophic losses.

Merlin Investor’s technology is compatible with all trading platforms. The technology is suitable for both retail and professional traders, and is available for both the desktop and mobile. Merlin Investor enables users to retrieve market data and sentiment from multiple sources and apply that data to a massive range of tailor-made investment strategies.

With offices in both West Palm Beach, Florida, and Lugano, Switzerland, Merlin Investor made its Finovate debut at FinovateEurope earlier this year. The company returned to the Finovate stage in May for FinovateSpring. We caught up with Merlin Investor founder and CEO Guido Petrelli (pictured) this summer to learn more about the company, its mission to democratize access to investment strategies, and what to expect from the company in 2023 and beyond.

What problem does Merlin Investor solve and who does it solve it for?

Guido Petrelli: Merlin Investor was born as an intelligent protection and conscious guide for a more farsighted management of investments aimed limiting potential catastrophic losses while building long term positive results. Thanks to the Merlin platform, retail investors can educate themselves, study the markets, and create and track their own investment strategies to easily understand, balance and diversify investment risks.

In other words, we help and empower a new generation to invest with strategy in mind. This is the key to becoming successful and is the only factor distinguishing between gambling and investing. As we are on a mission to democratize financial inclusion and investment planning, our technology was built to allow anyone, regardless the level of knowledge or experience, to become independent and the one and only master of their own financial future.

How does Merlin Investor solve this problem better than other companies?

Petrelli: In the retail investor space, we see many companies focusing on execution, meaning focusing on the act of buying and selling assets. But executing without evaluating multiple sources of information first, combined with the lack of a diversified and balanced investment strategy, can lead to uncontrolled and unlimited potential losses because of the market’s ups and downs. While it may imply the chance for quick gains, it’s actually not the norm as wealth is usually built over time by managing a positive-sum game.

That’s why from the very beginning Merlin was designed as a complementary product to a trading platform and not as a substitute solution. Merlin Investor addresses the strategic essence of investing while the majority of the competition just focuses on enhancing the trading experience – which is already well supported by several financial institutions in a pretty similar way.

Who are Merlin Investor’s primary customers. How do you reach them?

Petrelli: Our primary customers are financial institutions focusing on educating a new generation of retail investors and offering the possibility to trade different asset classes through their digital banking platforms. We attend multiple fintech events in several countries that are attended by financial institution decision-makers responsible for delivering an innovative and digitalized experience to their clients. We also analyze the markets to identify those prospect clients we believe to be a fit in terms of services and client base. Then we look for the people focusing on retail digital products and platforms and reach out to them to introduce our company and technology. Last, we work to be featured in fintech-specialized magazines having financial institutions as target audience.

Can you tell us about a favorite implementation or deployment of your technology?

Petrelli: We offer our technology as a white-label solution that financial institutions can easily embed into their own digital platforms through API keys, while having the possibility to customize product’s appearance and features. As result, our product is delivered to the final users in the bank’s name and as a sub-section of the same app/e-banking they are already familiar with. Through our B2B partner’s portal, we grant to financial institutions the flexibility to choose from the full Merlin product those asset classes, sections, features, and contents they intend to integrate based on their own specific needs. In this way, they can design a tailored solution and experience for their own clients, while sticking to the overall structure and design of the banking platform they already offer.

What in your background gave you the confidence to respond to this challenge?

Petrelli: In a nutshell, it was the combination of my knowledge around investing and the problem I personally experienced as a retail investor that led to Merlin Investor. In fact, I was just a teenager when I first started to trade. Then I quickly realized that executing trades “per-se” – meaning the simple action of buying and selling assets – is the less strategic and relevant part to achieve long term positive results. Instead, studying different market sources, and then designing a diversified and balanced investment strategy, are what make the difference in the end. Still, (available) banking and trading platforms were not enough to educate me about investing, or to (help me) design and analyze my own investment strategies.

As a result, for years I was forced to create time-consuming and unfriendly spreadsheets to the point where I couldn’t accept it anymore – not in a world like today’s where we have an app for everything we do! At the same time with trading platforms booming basically everywhere, it became more and more clear that a new generation wants to invest autonomously and in the right way. As I couldn’t find any product in the market like the one I envisioned, I decided to create it. And that’s how Merlin Investor was born.

Merlin Investor founder and CEO Guido Petrelli demoing the company’s technology at FinovateEurope this year.

You recently demoed at FinovateSpring and will be demoing your technology at FinovateFall in September. What brings you back?

Petrelli: This year I’ve demoed the Merlin platform at FinovateEurope and FinovateSpring, so FinovateFall will be my third appearance. So far the experience has been great. We have been able to show our cutting-edge technology to major financial institutions in Europe and North America, while receiving much interest and establishing meaningful connections with decision-makers within the banking industry. The high visibility and key connections with prospect clients are the two main factors which bring us back to FinovateFall. The well-organized events and the team at Finovate are also a plus.

What are your goals for Merlin Investor?

Petrelli: Our goal is to be recognized by the major global banks as the innovative partner to work with when it comes to educating and empowering a new generation of retail investors. We focus on establishing solid and strategic partnerships with a limited numbers of players in the banking industry to achieve our mission of democratizing financial inclusion and strategic planning globally, while helping young investors to reach financial independence and to become the masters of their own financial futures.

What can we expect from Merlin Investor over the balance of 2023 and into next year?

Petrelli: We’ll continue to prioritize continuous and never-ending improvement of our technology by looking to upgrade the experience we offer either to financial institutions and to the final users to whom our product is deployed. We will also continue to work to boost our market presence to make the Merlin platform known to more financial institutions serving retail clients in several countries. We will eventually concentrate on scaling the team and operations to be able to manage expectations. We will accomplish all of this without forgetting our mission to make conscious and strategic investing accessible to anyone through strategic partnerships with financial institutions.

Formerly known as TeamApt, Moniepoint is the largest business payments platform in Nigeria. The company processes $170 billion in annualized total payments volume (TPV), and became QED Investors’ first investment in Africa last year.

Headquartered in London, with offices in Nairobi and Lagos, as well as the U.S., Moniepoint was founded in 2015. The company counts more than 600,000 businesses large and small among its customers. Moniepoint has been recognized by the Central Bank of Nigeria as the most inclusive payment platform in the country, and was named the second-fastest growing company in Africa by the Financial Times.

We caught up with Tosin Eniolorunda (pictured), founder and CEO of Moniepoint, to discuss the state of fintech in Nigeria and what Moniepoint is doing to help provide better financial services to businesses and communities in Africa.

In our extended conversation, we discuss challenges to digital transformation in the region, the evolution of Nigeria’s cashless economy, and what to expect in the wake of Moniepoint’s recent rebranding.

What problem does Moniepoint solve and who does it solve it for?

Tosin Eniolorunda: Moniepoint solves the problem of fragmented, inaccessible, and low-quality financial services for businesses in emerging markets. It is a full-service business banking platform seeking to provide all the digital financial services a typical business needs.

Moniepoint specifically provides businesses in emerging markets with banking, payments, credit, and business management tools to help them grow. Our motivation is to power business dreams and create financial happiness for our customers. We recognize the importance of businesses in driving economic growth. By powering the profitability and operations of these businesses, we hope to enable them to make significant contributions to the economy at large.

To date, we have powered the dreams of over one million businesses who support local communities up and down Africa.

Your company began the year with a rebrand, transitioning from Team Apt to Moniepoint. What was the significance of this decision?

Eniolorunda: The company, TeamApt, started as a service provider, and our name was aptly selected. The team providing these services was the heart of our solution. As the company grew, our flagship product – Moniepoint – became ubiquitous in the market, and it became necessary to bring everything together to push the whole brand forward. We had become the point for people’s money, and it was only right we took up that name.

We know top talent is highly sought after in the global fintech industry, which is why we wanted to show our commitment to embracing the best and brightest by going out into the world in our choice of headquarters. By being more globally oriented, we want to be recognizable as an employer of choice for talents around the world.

What is the financial services industry like in Nigeria? And what is its relationship with the fintech ecosystem?

Eniolorunda: The financial services industry in Nigeria is generally a collaborative one. The Central Bank of Nigeria drives policy change in collaboration with all players in the industry – traditional banks and fintech players – all geared towards a more financially inclusive ecosystem. An example of how this plays out is fintechs working with traditional banks as their settlement partners, and traditional banks providing virtual account solutions to fintechs so they can, in turn, provide digital wallets to their customers.

It’s also recognized that fintechs take a generally technology-first approach to financial solutions, and regulations exist to make this as seamless as possible.

You have said that “low-trust” is an impediment to digital transformation in Africa. Can you elaborate on this challenge and what is necessary to overcome it?

Eniolorunda: Financial education is particularly important to gain trust and support for digital transformation, as people generally are wary of what they do not understand. In societies with a large percentage of uneducated people, it is expected that they will push back on innovation that promises to make their lives better.

For example, if a digital bank wants to provide nimble convenient services, it might decide not to have physical branches or a call centre to manage costs. However, low-trust means that these communities of people want to see a person or hear from them in order to leave their monies in the bank.

We overcame this barrier by approaching these markets using a hybrid distribution method – via collaboration with local people they could identify. When they got introduced to these digital solutions by people they knew and saw in their neighborhoods, it became easier for them to trust these products and try them out.

This spring there were a number of headlines about the “cash crisis” in Nigeria. Can you tell us about this and how the crisis impacted Moniepoint?

Eniolorunda: In March 2023, as part of its effort to aid in adopting cashless means of payments, combat inflation and prevent fraud, the Central Bank of Nigeria started a redesign of the Naira, Nigeria’s currency. People had to turn in their old notes as they were no longer legal tender, and the consequence of this process was a reduced availability of cash and, by extension, increased reliance on digital payments.

Moniepoint began to focus on supporting businesses in April 2022, extending our banking and payment tools to them. Consequently, during this cash crunch, we were well-placed to provide these businesses with the tools they needed to accept digital payments and stay afloat.

As a result, we saw a surge in transactions during this period. We adjusted our platform to make it more reliable, helping us to keep supporting these businesses.

What role will Moniepoint play in an increasingly cashless economy in Nigeria and other parts of Africa?

Eniolorunda: By being a banking partner for businesses, we enable them to receive payments digitally, which is very important in Africa’s journey towards becoming a cashless economy. In 2022, we helped businesses process over $170 billion, and are continuing this positive trend in 2023.

We are determined to stay at the forefront of the digital revolution. Initial efforts across the continent have been focused on providing individuals with access to digital financial services, giving them cards and other means to pay digitally. It’s not enough for customers to be empowered to pay digitally; the businesses have to be equipped with the education and resources to receive these payments.

When businesses are able to receive these digital payments directly, cash becomes less central to every transaction, and we’re collectively closer to a cashless ecosystem.

There has been talk in the fintech press about Moniepoint and potential acquisition opportunities. Is the company actively looking to make significant acquisitions?

Eniolorunda: Yes, the plan is to make significant and strategic acquisitions that align with our overall goal of providing an all-in-one financial platform for businesses in emerging markets. These acquisitions allow us to expand our product suite or enter new markets.

Also recently Moniepoint announced a partnership with Google Cloud. Why did Moniepoint pursue this partnership, and what will the partnership help Moniepoint accomplish?

Eniolorunda: As we grew bigger and faster, it was important that financial transactions on our platform could be performed at light speeds, so adopting a hybrid cloud strategy was key for us.

Some of the tools include Cloud Spanner and Kubernetes, which help us to manage and process high volumes of transactional requests per minute, with no lag time. A partnership with Google Cloud ensures we can use their services with personalized support that the scale of our business needs.

What can we expect from Moniepoint in the second half of 2023 and into next year?

Eniolorunda: We are proud to have already been be recognized this year as not just Africa’s largest fintech, but also its fastest-growing. But this is only the beginning.

We have so much in store for the second half of 2023, including plans for a new product and to enter new markets. Watch this space.

“NayaOne is a digital transformation platform that helps you leverage the fintech ecosystem. We work with product, innovation, and tech teams in banks and insurance companies to help them get their products to market much, much quicker. We have synthetic data sets and building tools on the platform. Typically, it takes companies nine to twelve months to begin working with a fintech. Our customers can get to that outcome in about six to eight weeks.”

“We provide the industry with a digital banking market research platform that’s analyzing the digital offerings of banks, fintechs, credit unions, across the U.S. and worldwide. We analyze – from A to Z – what the banks, fintechs, and credit unions are offering, how they offer it, (and) how well they offer it, all while providing them with the ability to benchmark against the market and organize their product roadmap to implement their digital banking strategies.”

Greg Palmer chats with Nicole Sanders and George Broom of 10x Banking on streamlining product development and getting to market faster. Episode 171. Demo video.

“10x is a cloud-native banking platform that acts like a real-time operating system for banks. It allows you to build and run your bank at record speed at a fraction of the cost. We demonstrated that at Finovate through the use of our Bank Manager UI application. This allows product managers at banks to build products in minutes rather than months. In that seven minutes, we built a current account with a card and also a loan ready for launch to production.”

“We are a scale-up, San Francisco-based, that provides a software-as-a-service, machine learning platform which enables business experts to stay in control of their AI models. We also empower the data science and engineering teams through our technology that consists of the ability to continuously learn from the data as the business world changes. We provide continuous explanations to business users and give them the ability to give feedback to the models so that the models are aligned with the business all the time.”

Stay tuned for more insightful conversations from Greg Palmer and the Finovate Podcast!

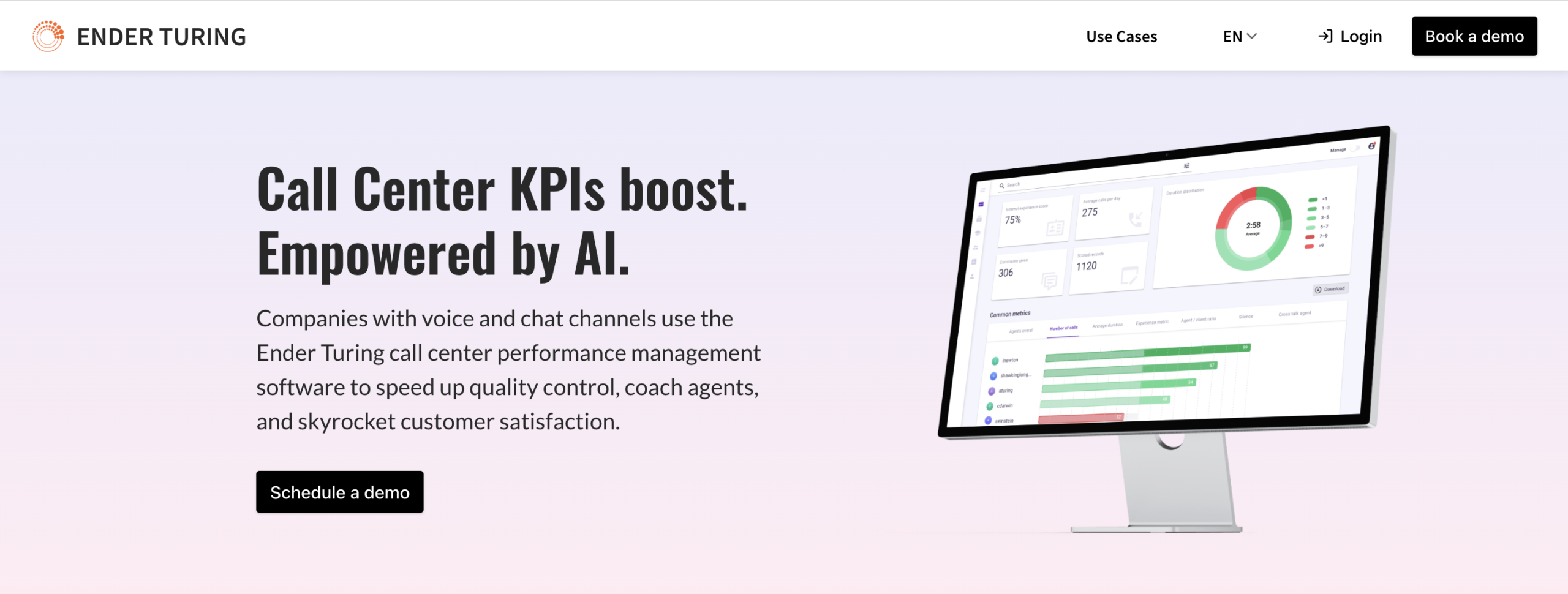

This week’s edition of Finovate Global takes a look at one of the innovative fintech companies headquartered in Estonia: Ender Turing. The firm, which specializes in voice conversation intelligence and automation, made its Finovate debut earlier this year at FinovateEurope in London.

Headquartered in Tallinn, Ender Turing was founded in 2020. The founding team consisted of two AI researchers with experience in automatic speech recognition and natural language processing (NLP), as well as a third member with experience in enterprise-level call center software. Together, the team formed Ender Turing and have since launched Ender Turing AI Speech Analytics. The new solution automatically analyzes and assesses the communication content between financial institutions and their customers. This helps FIs enhance the customer experience, as well as meet quality guidelines and compliance requirements in areas such as customer service, sales, and debt collection.

We corresponded with Ender Turing CEO Olena Iosifova via email. Below are her responses to our questions.

Read more about fintech in Estonia in this Finovate Global column from earlier this year.

What problem does Ender Turing solveand who does it solve it for?

Olena Iosifova: Eight hundred million voice conversations are recorded daily in Europe and many more worldwide. A tiny 1% of these conversations are checked for quality control, employee training, and business results improvement. Ender Turing is a conversations intelligence and automation platform to close 99% of the conversation gap for business growth.

Our daily business users are customer service, sales, and collection departments. But marketing and product teams also get value from making client’s research right on our platform.

How does Ender Turing solve this problem better than other companies?

Iosifova: Ender Turing created the fastest-to-value platform that performs in 24 languages. We use a proprietary speech-to-text engine to fine-tune models for every client to achieve the highest accuracy. Our machine learning pipelines are very efficient, and we can fine-tune speech recognition for free.

Also, the user interface does all the system setup for reaching business KPIs. There is no need to wait for the time slot at the IT department to help a business unit make it.

Who are Ender Turing’s primary customers?How do you reach them?

Iosifova: Our primary customers come from financial industry. These are banks, debt collection firms, and other financial services companies. But we also have clients in the public sector and in healthcare.

Direct outreach is our main channel of getting noticed by potential customers – as well as our partnership network. We cooperate with system integrators and call center software vendors and offer added value to their customer base.

Participation in conferences serves as a great supporting touch.

Ender Turing CEO Olena Iosifova demoing Ender Turing AI Speech Analytics at FinovateEurope 2023.

Can you tell us about a favorite implementation or deployment of your technology?

Iosifova: We have two great examples of our technology implementation. One is OTP Bank, and another is Creamfinance Group.

In OTP Bank it started with the call center customer service department. One month after we started, the debt collection department joined, seeing great results. OTP Bank saw hundreds of hours of saved time every month for quality management, employee training, and improved conversion rates – results we mutually enjoy.

With Creamfinance Group, the best indicator of great business results is that after implementation in their headquarters in Poland, we now serve also their offices in Spain, Mexico, and the Czech Republic.

What in your background gave you the confidence to respond to this challenge?

Iosifova: Three founders in Ender Turing have positive experience and skills in artificial Iitelligence R&D, business management, and a passion for building highly performing teams. We enjoy analyzing our potential customers’ strategies and market trends to foresee the challenges they might face in the next three to five years. With constant innovations inside our R&D, we build our product to deliver value for today and the future.

What is the fintech industry like in Estonia? How do traditional financial institutions treat Estonian fintechs?

Iosifova: Apart from the big name in fintech, Wise, coming from Estonia, other exciting fintechs are growing here. To name a few – Grunfin, Scrambleup, Tuum, Salv, Montonio.

They partner with traditional financial institutions actively. For example, LHV Bank is the best client of Tuum. And Salv is the AML solution that works exactly in a traditional financial services market.

You recently demoed your technology at FinovateEurope in London. What was that experience like?

Iosifova: This is truly an international event where we met companies from all over the world. This was a pleasant surprise. We will participate again.

What are your goals for Ender Turing?

Iosifova: Our goal is to become a number-one choice platform for banks and financial services companies regarding conversation intelligence and automation, providing the best quality of service, sales conversation rate, and recovery rate.

What can we expect from Ender Turing over the balance of 2023?

Iosifova: Our growth in 2023 gets us to expand to the U.S. and Latin America. But what’s more interesting is that we bring real-time agent assistance to fill the gap between the top-performing agents and the rest of the team and ensure real-time compliance monitoring in every conversation.

As Financial Literacy Month draws to a close, we reached out to Parker Graham, founder and CEO of Finotta. We wanted to hear his thoughts on what it means to be financially literate at a time of major digital transformation and technological change – both in financial services and in the world writ large.

Finotta enables banks and credit unions to personalize their mobile banking experiences for their customers. Headquartered in Overland Park, Kansas, and founded in 2018, Finotta helps smaller financial organizations generate new revenue streams, boost user engagement, and compete with larger financial institutions.

Finotta made its Finovate debut last year at FinovateFall.

What does it mean to be financially literate in 2023?

Parker Graham: For many people, managing their finances and staying financially literate is not just a challenge – it feels harder than ever.

With decades-high inflation and historic interest rate hikes, consumers are feeling the heat. Most workers reported that any salary gains they’ve received in the last year have been outpaced by inflation. We’re really seeing this hit young people hard. Half of Gen Z and Millennials are living paycheck to paycheck.

Many consumers don’t know what steps to take to get ahead. And with traditional digital banking channels lacking that personalized experience, they aren’t getting the advice they need. Banks and credit unions must prioritize financial education for their customers because they can’t afford to be left behind.

In today’s world, is digital literacy required in order to be financially literate?

Graham: Digital literacy is a huge challenge we’re facing in the banking industry. More than 15 million people are not digitally literate. Consumers should not have to know how to bank online to make good financial choices.

To tackle this, banks should ensure that customer experience is at the forefront of all of their technology decisions. Banking apps need to be easy to read, quick to navigate, and intuitive – even for individuals who are not digital natives. This is exactly why we work directly with users when building our technology at Finotta to make sure it is easily accessible, navigable, and understandable.

Banking tech also must go the extra mile and make it personal by providing Personalized Financial Guidance (PFG) to customers. This guides consumers through their financial journey, no matter where they are, by offering tailored advice on how to meet their financial goals.

How can we make sure technology is an enabler of financial literacy rather than an obstacle to it?

Graham: Banks have to remember that acquiring a new digital banking solution isn’t just about technology for the sake of seeming flashy or modern. A banking app can actually help with financial literacy by taking the guesswork out of what customers should do with their money.

Your banking app needs to deliver the right experience, service, or product to the customer based on their individual data. Then, it should offer users concrete suggestions, like opening a new savings account for college tuition, that help them achieve financially healthy lives. The cherry on top is offering in-app rewards, like badges and milestones, that recognize customers for their positive choices and make financial literacy fun.

How does personalization in digital banking help foster financial literacy? How can fintechs help digital banking customers turn insights into action?

Graham: Consumers are looking for financial guidance beyond typical personal financial management tools, which do nothing more than provide fancy pie charts that show a customer’s spending.

From a consumer’s perspective, getting alerts in their banking app that tell them how much money they spent at Starbucks over the last month (when that money could have gone towards a 401K instead) does nothing more than shame them. It’s essentially saying, “Hey, you’re in a hole.”

Instead, banks can take consumer data one step further by helping them take actionable steps to reach their goals – like setting up monthly direct deposits to save towards retirement. A bank using a personalized approach can say, “Hey, we see you’re in a hole, and here’s how you can get out.”

Finotta made its Finovate debut last year at FinovateFall. What was that experience like?

Graham: Debuting our technology last year at FinovateFall was incredible. It gave us an opportunity to tell the story of how powerful and impactful our platform is in a room of our customers and peers.

What can we look forward to hearing about from Finotta in the coming months?

Graham: The next few months for us are going to be about scaling with more and more customers. It’s been a journey building our software and now we are focused on replicating our successes with as many financial institutions as possible.

In this week’s edition of Finovate Global, we feature Uri Rivner, co-founder and CEO of Refine Intelligence. The Tel Aviv, Israel-based company, founded in 2022, made its Finovate debut earlier this year at FinovateEurope. At the conference, Refine Intelligence demoed its technology, Life Story Analytics, that leverages AI to help banks better defend themselves against money laundering.

We discussed the challenge of fighting financial crime, the innovations that Refine Intelligence brings to the market, and the relationship between upstarts and incumbents in Israel’s dynamic, fintech and financial services ecosystem.

What problem does Refine Intelligence solve and who does it solve it for?

Uri Rivner: If you’re a bank, your AML Operations team is massive, and needs to grow every year to cope with growing alert volume. But the team can have a pretty frustrating daily routine, as almost all the alerts they’re investigating end up being totally legit activities done by the customer.

Take an account that did a large wire transfer to Mexico for the first time. The AML Transaction Monitoring is screaming like a banshee – maybe there’s money laundering here? But after investigating, the team finds out the customer just has a daughter studying in Mexico, and this was to pay her tuition.

Years ago banks knew these life stories, because everything was done at the branch. But now with digital transformation, banks have lost that superpower.

At Refine intelligence, our mission is to help banks regain that superpower of really knowing their customers’ life stories, so their financial crime teams can quickly clear AML or scam alerts triggered by legitimate customer activity. We work with Risk, Financial Crime, BSA and AML teams. Fraud teams look at our technology to help with scam operations.

How does Refine Intelligence solve this problem better than other companies?

Rivner: Refine Intelligence takes a unique approach for fighting Financial Crime – we call it ‘Catching the Good Guys.’

Think of someone who got married and now deposits a large amount of cash from wedding gifts. Or a couple withdrawing cash in order to pay for a big renovation project. Think of people starting a new cash-intensive job, or depositing money from a fundraiser. These are all legitimate activities that look abnormal, triggering transaction monitoring alerts.

Refine discovers these sort of “life stories,” i.e. legit customer activities behind a flagged anomaly. There are two ways to do that:

The first is to ask the customer and Refine provides that capability through our Digital User Outreach which allows a bank to reach out to customers automatically and collect their explanation within minutes.

The second way is to train AI to recognize the life story behind an anomaly, without reaching out to the customer. Our Life Story Analytics does that, and the training uses our unique, proprietary data set of genuine explanations.

The outcome: clear, fast evidence that helps AML teams clear away falsely flagged anomalies by identifying the legitimate customer activity behind them.

Who are Refine Intelligence’s primary customers? How do you reach them?

Rivner: We work with large to mid-sized banks who operate a big team of investigators to look into AML alerts. Refine helps those banks reduce their operational effort significantly without making any change in the Transaction Monitoring system.

Our founders and senior management team have been working with financial crime units for decades, and we expand our reach via participating in events such as Finovate, as well as our own virtual events.

Can you tell us about a favorite implementation or deployment of your technology?

Rivner: A Top 50 bank in the U.S. deployed Refine Intelligence to handle customer outreach for AML. Before using Refine, the AML team approached the branch when they couldn’t find a good explanation to a flagged anomaly. The branch tried calling customers, leaving messages and chasing them for answers. A district manager described the situation as “we are the punching bag of the AML team.”

After the bank started working with Refine, it became clear why the existing RFI (Request for Information) process was driving everyone crazy. The average time to complete a customer outreach was 16 days with 3.6 back-and-forth emails between the AML team and the branch, as initial responses were often insufficient. The process consumed resources that were better used elsewhere.

Refine Digital User Outreach automated the process by messaging customers through digital channels. Response time was cut from two weeks to two minutes, completely changing the game for the Operations team who could work on alerts without interruption, receiving quality responses. With an 85% answer rate, the digital process outperformed manual outreach. Data collected was structured and allowed analysis and benchmarking, and soon most RFIs (Requests for Information) turned digital using the Refine system. The AML team loves the new approach.

What in your background gave you the confidence to respond to this challenge?

Rivner: I’ve been fighting online fraud for 20 years in Cyota, RSA and BioCatch – which I co-founded. This helped me take an outside look at the way AML was operating and realize that the current paradigm isn’t sustainable.

Online fraud detection benefits from context-rich signals that go well beyond transaction monitoring, device analysis, geo-location or behavioral biometrics. These signals feed into AI that is trained using a huge pool of fraud cases, as victims report fraud in their bank account. But no one reports money laundering in their own account, and when a bank files a Suspicious Activity Report, they never get feedback from authorities. You can’t train AI to recognize bad guys without feedback, so the industry had to revert to anomaly detection.

You can get more and more efficient in anomaly detection, but at the end of the day most of what you find is irregular activity in good people’s accounts. Any improvement in detecting bad guys is doomed to be marginal. And that’s not good – the industry needs a game changer…

This brought the insight of reversing the focus, to “Catching the good guys,” that is, detecting the legit activities that were falsely flagged as anomalies.

What is the fintech industry like in Israel? What is the relationship between fintech startups and the country’s established financial services sector?

Rivner: Israel, widely known as the ‘start up nation,’ is a powerhouse of cyber, fintech and financial crime fighting. Many market-shaping startups grew up in Israel: Cyota, now RSA Outseer, was first to introduce risk-based authentication using device and geo-location analysis. IBM Trusteer was first to launch an anti-Trojan tech. BioCatch was first to leverage behavioral biometrics for online fraud and scam detection. Forter and Riskified pioneered the chargeback guarantee market in eCommerce, Simplex did the same in crypto, and DoubleVerify prevents fraud in the digital advertising market. The largest global player in AML is Nice Actimize, and companies like EverC and ThetaRay help acquiring banks and payment providers manage financial crime risks. This might explain why there’s a vibrant community of fraud fighters in Tel Aviv.

Interestingly enough, the local Israeli market has never been a big target for those innovators. Most Israeli Fintech startups work directly with global design partners, who recognize the disruptive, out-of-the-box thinking behind their technology.

You recently demoed your technology at FinovateEurope. What was that experience like?

Rivner: Demoing at FinovateEurope was fantastic! We were thrilled to have the opportunity to demo together with so many other innovative fintech companies, and to meet with banks that are looking to incorporate innovative technologies into their operations. The experience was very TED-like, professional, and the vibe was exciting.

What are your goals for Refine Intelligence? What can we expect from the company over the balance of 2023?

Rivner: Everyone we talk to is very excited about what Refine is doing. When showing our Digital Outreach capabilities, AML teams come up with so many ways to use it effectively – from automating requests of information for resolving transaction monitoring alerts to helping the line of business with Enhanced Due Diligence and Cash Structuring education. Fraud teams are particularly interested in digital outreach to potential scam victims, and it is a great way to conduct rapid investigations of incoming wire and check deposits.

But the biggest amount of interest is in our other bit of magic – Life Story Analytics. That’s where we train AI to recognize the legit customer activity behind a flagged anomaly, without reaching out to the user. Financial Crime teams are excited about the notion of keeping their AML transaction monitoring or scam detection models as is, despite the high degree of false positives, and letting AI sweep aside the legit customer activities so what’s left are the real unexplained anomalies that might be money laundering or scam victims. That’s going to be a major area of expansion for Refine.

How has the challenge of digital transformation impacted banks and credit unions in recent years? Has the momentum for change slowed since the peak of the pandemic? How can banks win the “expectations game” with increasingly digital-first customers?

These are some of the questions we posed to Savana CEO Mike Wolfel. Headquartered in Malvern, Pennsylvania, Savana offers banks and other financial institutions a digital delivery platform that provides single location, real-time orchestration for all processes and transaction requests across the enterprise.

In recent months, Savana has announced partnerships with Primis Bank, Capco, and Battle Financial. Founded in 2009, the company has raised more than $53 million in funding from investors including Georgian and LiveOak Venture Partners.

What is the primary challenge for banks and credit unions that are trying to undergo digital transformation today in 2023?

Mike Wolfel: Most of the challenges banks and credit unions face center on technical innovation constraints based on their existing technical and operating architectures. Banks and credit unions are often limited either by their complex and rigid solutions already in place to support multiple channels or products, or by the inflexible multi-system architecture that allows them to be more agile. In addition, the lack of complete API exposure of underlying core systems leaves little opportunity to drive digital self-service or product innovation.

The inconsistency of processes implemented in different channels or across products is both a technical constraint and an operational efficiency challenge. These inconsistencies of processes and dependencies on manual work can also create regulatory issues or, at a minimum, lead to customer dissatisfaction.

There was a great deal of momentum behind digital transformation during COVID. Has that momentum waned? If so, why?

Wolfel: The momentum has not changed, but the focus seems to have shifted to different areas and more broadly expanded across various layers of the banking technology. The drive for transformation during COVID, especially during the first year, was a general improvement in digital consumer experiences due to the branch banking challenges. However, the banks we are working with seem to be taking a broader and more systemic internal view to recognize that they need more agility in terms of next-gen cores and more operationally efficient operations systems.

How can banks win the expectations game? How can the customer experience at banks keep up with the kind of CX/UX people experience in other digital interactions?

Wolfel: Bank experiences need to deliver more active intelligence, using AI, to consumer experiences. An adaptive information approach to tailor content and action needs to be more dynamic based on customer intelligence and behavior analytics. Just as Amazon or social media applications recommend the content of interest, consumers can be enlightened with relevant information on their banking behavior that will enable them to see opportunities better.

In addition, the capabilities of the experience, not just a pretty design, need to provide an effective and comprehensive set of services to the consumer to take action without requiring the need to engage the bank in the direct channels (branch, call center). Clearly, consumers prefer self-service and being able to act at a time and place of their choosing. Additionally, having the same processes and awareness of customer engagement actions need to be available to the banker if the consumer reaches out for direct support. Often, in today’s environment, the bank is unaware of why the customer might be calling when making a transition for support between digital to direct engagement.

What are the first key steps a financial institution needs to take in order to be ready for digital transformation – to say nothing of executing the transformation itself?

Wolfel: That depends on the goals and the transformation journey desired by the bank. But, in general, several things are consistent for the banks we work with on their journeys. First, they are taking a much broader view than trying to solve for a specific channel improvement. For those that are considering new next-gen core technology, they need to decide on a big bang or progressive renovation approach. The progressive renovation (gradual cutover to a new core) takes significant planning because it will create significant operational issues with customer and account data spread across multiple cores.

Comparatively, a big bang cutover to a next-gen core will require significant ecosystem rework and presents a potentially higher risk. Fortunately, Savana’s approach and architecture support our bank partners regardless of their desired approach. In the end, having a clear vision of the full end-state vs. a siloed or segmented view is the critical consideration.

What role does Savana play in helping facilitate digital transformations for financial institutions?