This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

We’re halfway through 2025, and with two Finovate events in the books, there are clear themes emerging around the future of financial services and fintech.

In this edition of the Finovate eMagazine, we bring you insights from both sides of the Atlantic, featuring key learnings from FinovateEurope and FinovateSpring.

Fill in the form and discover the trends shaping the future of financial services and fintech. Explore:

The latest approaches to innovation

Hear from David Barton-Grimley and Bhoomika Ghosh on how to make innovation meaningful and impactful. Plus, David Penn brings us insight into how credit unions want to digitise and partner.

How to navigate global growth in today’s economy

Julie Muhn brings us the key regulatory shifts on both sides of the Atlantic and David Grace from SHAZAM explores the importance of partnerships to face the upcoming challenges

The Finovate Library on Streamly

This eMagazine brings you insights to inspire your business strategy and your future endeavours.

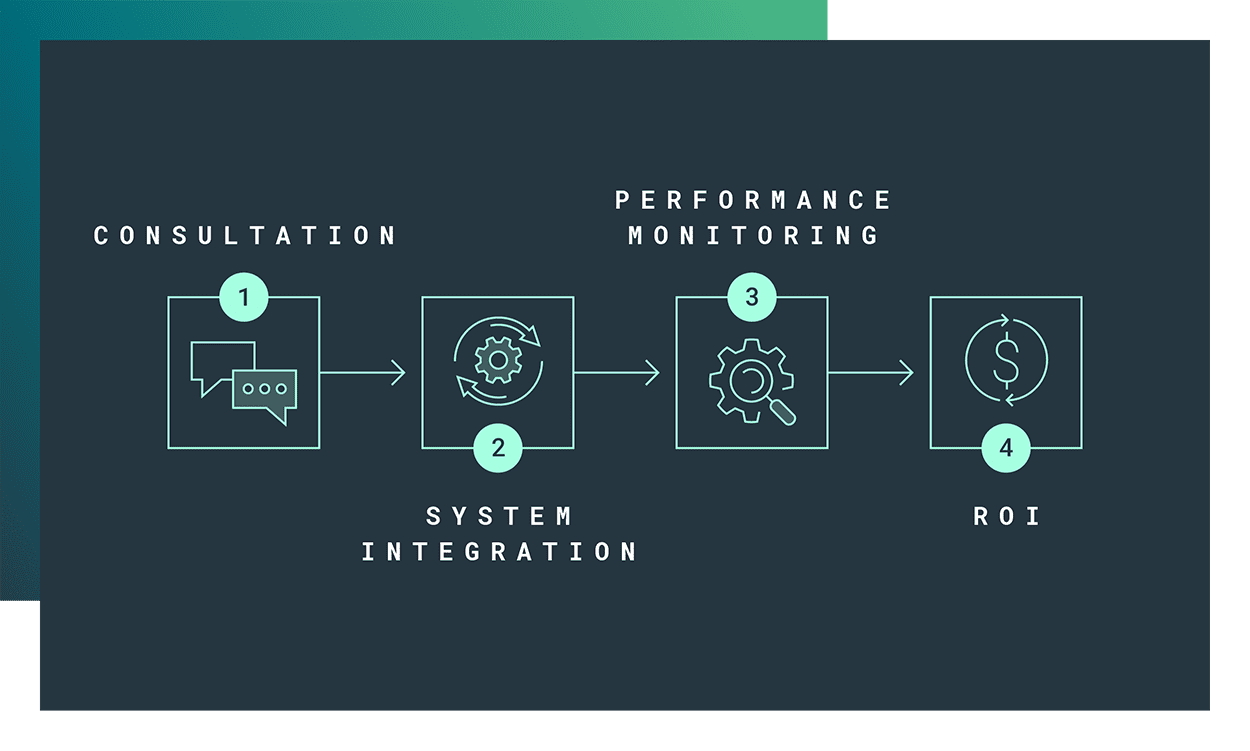

Successfully integrating AI into core business services isn’t a straightforward approach—this requires strategic foresight into AI and how it best aligns with business, regulatory compliance, and operational efficiency.

Putting this into action and delivering AI solutions can drive real impact, especially for those in the financial industry. At VASS Intelygenz, we personalize services for our customers, automate their manual operations, and improve efficiencies. We work through the whole AI project lifecycle, conceptualizing, developing, deploying, and maintaining custom AI solutions that solve real business problems. All of which are reshaping how financial institutions operate by enhancing their client interactions and uncovering new market opportunities.

However, AI is not as simple as flipping a switch. According to a Gartner research, only 15% of AI solutions deployed by 2022 will be successful, let alone create ROI positive value. The path from implementation to achieving measurable ROI can feel complex and daunting. Identifying the right solutions, navigating the complexities of AI, and ensuring AI initiatives deliver measurable ROI have often led financial institutions to a standstill when it comes to their AI implementation.

With over two decades of expertise in machine learning and AI, we’ve helped financial institutions unlock the potential of AI to deliver real business value. Here, we outline three key lessons to keep in mind as you start your AI implementation process.

1. Align AI With Your Business and Change Management Strategy

The most successful AI initiatives start with a clear alignment to your business goals. Instead of jumping into technology innovations, identify the core challenges your organization is facing and determine how AI can address them. Are you looking to reduce operational costs? Improve customer retention? Prevent fraud? Only then should you consider which AI solutions will address these challenges.

Actively involve key stakeholders, including leadership and operational teams, during the implementation phase. This collaborative approach ensures that everyone understands the strategy, leading to smoother implementation and better ROI.

It’s integral that you invest in training and communication to help employees adopt AI tools with confidence, so they become champions of the technology rather than resistors.

2. Make Sure to Implement AI Safely

While the potential of AI-powered solutions in finance are vast, the risks are equally significant. Financial organizations deal with highly sensitive information and operate in tightly regulated environments. Implementing AI safely is non-negotiable.

The finance industry is a signifier of importance when it comes to balancing innovation and compliance. AI systems within finance that automate credit scoring or detect fraudulent activities must adhere to strict regulations and industry-specific requirements. Before adoption, ensure that your AI solutions meet ethical guidelines, operational standards, and legal compliance.

Another critical consideration is explainability. Stakeholders, from board members to customers, need clarity on how AI systems get to their conclusions. Choose solutions that incorporate transparency tools, such as explainable AI models, so you can maintain trust while also fulfilling regulatory requirements.

3. Have Confidence in Proof of Concepts (PoCs)

AI is advancing rapidly, and businesses that hesitate to move beyond pilot projects risk missing out on its full potential. To maximize ROI, you must scale your first steps into AI with a fully integrated, organization-wide solution.

While pilot projects allow you to test AI solutions on a small scale, their impact remains limited without transitioning to full-scale deployment. Leading organizations are fast-tracking this process, transforming successful PoCs into actionable, large-scale AI systems. This shift enables businesses to get ahead of their competition, enhance profitability, and reduce costs.

Implementing AI successfully into your financial organization involves more than just an interest in emerging technologies. It requires alignment with your unique business strategy, identifying your challenges as well as having ROI in the forefront of your mind.

At VASS Intelygenz, we bring over 20 years of experience to the table, with a proven process that streamlines AI adoption, from scoping opportunities to rapid experimentation, so you can unlock value quickly and deliver ROI faster. We’re committed to helping financial institutions unlock the true potential of AI.

Want to learn more about this topic? Join us at our presentation at FinovateSpring on May 7th at 2:45pm to explore real-life examples and strategies for implementing transformative AI. Find out more here.

Across the world, growing numbers of young people, new-to-country immigrants, and other groups are poised to enter the financial system as customers of credit, loans, remittances, and more. By 2030, 75% of consumers in emerging markets will be between the ages of 15 and 34.

Companies that can safely onboard and serve this population of emerging identities can unlock significant growth potential and improve financial inclusion. But for the banking and payments systems of the world, emerging identities often complicate traditional approaches to recognizing trusted customers.

Younger demographics haven’t had as much time to build up a record of working, borrowing and purchasing.

New-to-country immigrants might not have acquired financial products or proof of residence outside of their birth countries.

Older consumers that live communally and don’t have a driver’s license may seem risky.

Identity verification needs to keep pace with all of these changes, and more.

Emerging Identities Provide Superb Camouflage For Synthetic IDs

From the business world’s perspective, emerging identities can seem to appear out of nowhere, often with robust digital profiles but fewer physical identifiers. Unfortunately, these profiles also strongly resemble third-party synthetic identities, cobbled together by fraudsters from real, modified, and fake bits of identity information.

Since first materializing in the US more than 10 years ago, synthetic identities have spread to other major financial economies. Recent analysis found three million high-risk synthetic identities in circulation in the UK alone, with the volume increasing at a rate of over 500% between 2020 and 2023.

With global losses from synthetic identities estimated at up to $40 billion, businesses must be cautious of this rising threat as they attempt to find ways to onboard emerging identities.

It’s bad business to reject low-risk emerging identities. Even flagging them for manual review increases operational costs and degrades the applicant’s onboarding experience, starting the new relationship with an unproductive atmosphere of mistrust.

How Synthetic Identities Cloud The Search For Emerging Identities

There are two types of synthetic identities, broadly speaking. First-party synthetics are alternate identities that consumers create for themselves, for a specific purpose—and not always with malicious intent. However, these identities often collide with the real identity they are augmenting, and do not pass validity checks.

Third-party synthetics are more malicious in nature. These are sometimes referred to as “Frankenstein” identities because a third party cobbles together pieces of identities from legitimate and fictitious sources into one imaginary digital identity they can leverage for cybercrime. These are managed via disposable email addresses and phone numbers, to help maintain anonymity.

Credit bureaus have become an unexpected, but reliable ‘source’ of synthetic identities. It’s hard for criminals to fabricate an identity through credentialed sources like voter registration, a property deed, or a professional certification. On the other hand, it’s relatively easy to submit multiple credit applications to stimulate the creation of a credit profile.

How To Tell Synthetic Identities From Emerging Identities

Though synthetic identities can appear very similar to emerging identities, smart analysis backed by robust intelligence can reveal telltale patterns of synthetic fraud. For example, synthetic identities are 7x more likely than emerging identities to have no first-degree relatives, 20x more likely to appear in multiple credit applications in a short time period and 7x more likely to first show up at a credit bureau at an unusually late age.

Businesses Are Finding New Ways To Safely Onboard Emerging Identities

Competing more effectively in the emerging consumer market starts with an accelerated customer acquisition process that speeds approvals for legitimate customers while mitigating fraud threats. Balancing faster approvals with increased confidence demands identity verification that accurately assesses applicant identity and behavior patterns in real time.

Because emerging identities appear without historic data, businesses need more diverse sources of context around risk.

Seek out alternative data sources. For example, education sources can help to verify younger demographics.

Clarify a bigger picture.Robust collaborative intelligence networks help to set an identity’s desired action in the broader context of their past and real-time interactions with other organizations, in different industries and even across borders.

Authenticate documents with liveness checks. More advanced solutions can verify and authenticate valid documentation without much disruption to the user experience.

Layer insights for a more comprehensive view of identity. How is the user behaving? Are they mobile? Are they submitting many applications in a short period of time? Does the email, device or location carry risk signals? The sum of these insights clarifies risk more than any one contributing factor.

Both customers and businesses win when emerging identities can be verified reliably and distinguished from synthetic identities. More legitimate consumers access the financial services they want. Businesses acquire more customers safely while reducing costs and better focusing manual fraud risk assessments.

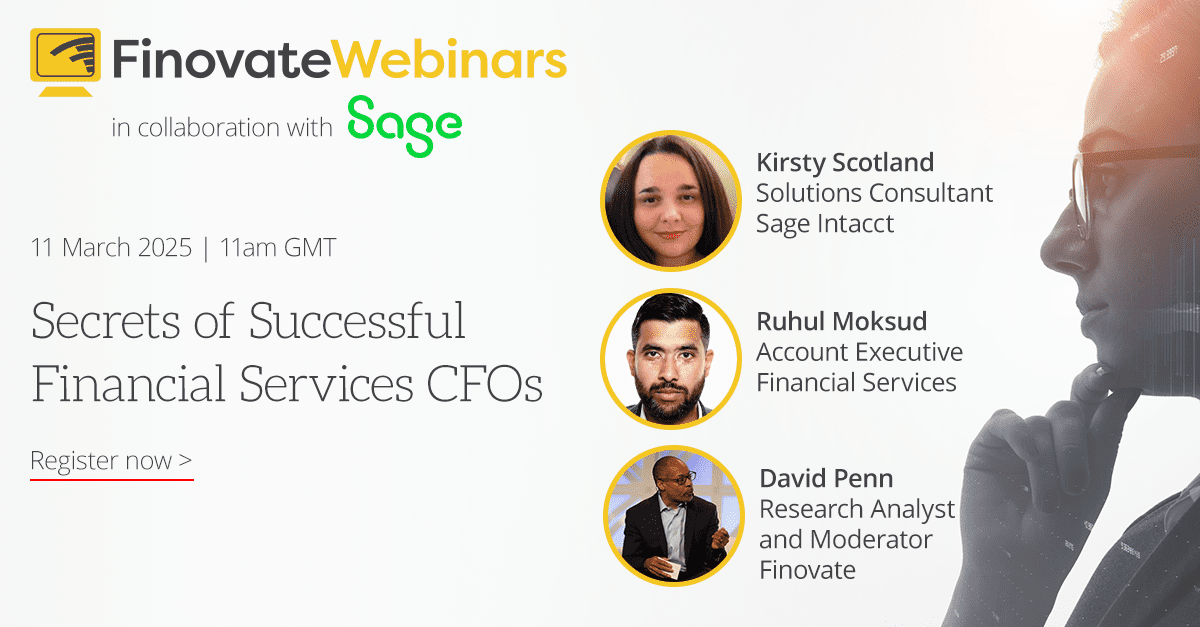

Discover the best practices top financial leaders use to become more impactful in their firms.

Financial services Chief Financial Officers (CFOs) are navigating a complex landscape of rapid technological advancements, increasing regulatory demands, and the necessity for agile financial strategies.

As their roles evolve into Chief Financial Growth Officers (CFGOs), leveraging cutting-edge technology to drive innovation and efficiency has never been more important.

Watch this webinar with Kirsty Scotland and Ruhul Moksud to learn about:

The impact of AI and machine learning on financial leadership specifically in financial services firms

Driving efficiency through automation and process improvements

This edition of the Finovate eMagazine brings you insights from FinovateFall 2024. We spoke to dozens of experts, innovators, and strategists from banks, credit unions, wealth management firms, and insurance companies about the hottest topics in fintech. Learn how they:

Elevate customer experiences From approaching Gen Z and addressing the painpoints of change to empowering employees and enhancing customers’ digital journeys.

Build partnerships As financial institutions share their approaches and how they bring cultures together.

In the financial services sector, artificial intelligence (AI) is often heralded as a transformative force capable of revolutionizing everything from customer engagement to fraud detection. However, as the excitement around AI continues to grow, so do the challenges associated with its implementation. According to the latest McKinsey Global Survey on AI, AI adoption is accelerating, with 72% of organizations using AI in at least one business function in 2024, up from 50% in previous years. However, the challenges of achieving tangible business value remain substantial. The survey highlights that organizations need to focus on aligning AI projects with strategic business goals to achieve success (McKinsey, “The State of AI in Early 2024”).

The journey to successful AI implementation in financial services is not about jumping on the latest technology bandwagon; it is about identifying core business challenges, choosing the right AI strategy, and following a robust engagement methodology. Here’s how financial institutions can move beyond the AI hype and achieve real, measurable business value.

1. Start with the business challenge, not the technology

The key to successful AI deployment begins with a comprehensive understanding of the specific business problems that need to be addressed. Too often, organizations are drawn to AI’s potential without a clear roadmap for its application, leading to projects that flounder in development or fail to deliver a return on investment (ROI). McKinsey notes that “the business goal must be paramount,” emphasizing the importance of identifying the most promising business opportunities and working backward to potential AI applications rather than pursuing tech for tech’s sake (McKinsey, “The State of AI in Early 2024”).

For financial institutions, this means asking critical questions: What are the pain points that, if resolved, would yield the most significant benefits? Whether it’s enhancing customer engagement, improving fraud detection, or optimizing operational efficiency, defining the challenge upfront ensures that AI initiatives are grounded in strategic business needs rather than technological fascination.

2. Evaluate: build, buy, or partner

Once the business challenge is identified, the next step is to determine the most effective strategy for deploying AI. This involves a critical decision: whether to build a custom solution, buy an existing one, or partner with an AI expert.

Build: Custom solutions offer the highest degree of specificity and alignment with unique business processes, but they require significant time, resources, and in-house expertise. For institutions with complex, industry-specific needs, building an AI solution may be the most effective approach, but it also carries the highest risk.

Buy: Off-the-shelf solutions provide a faster route to deployment and can be cost-effective for common challenges. However, they may not offer the flexibility needed to adapt to specific business environments. McKinsey’s latest research shows that while 50% of organizations are using off-the-shelf generative AI models, the high performers are increasingly moving toward significant customization or developing proprietary models to meet specific needs (McKinsey, “The State of AI in Early 2024″).

Partner: Partnering with a specialized AI consultancy, like Intelygenz, allows organizations to leverage deep technical expertise and experience while focusing on rapid implementation. A trusted partner can guide institutions through the complexities of AI deployment, ensuring that the solution is tailored to deliver the maximum business impact. This approach combines the benefits of both build and buy strategies, mitigating risks and accelerating time to value.

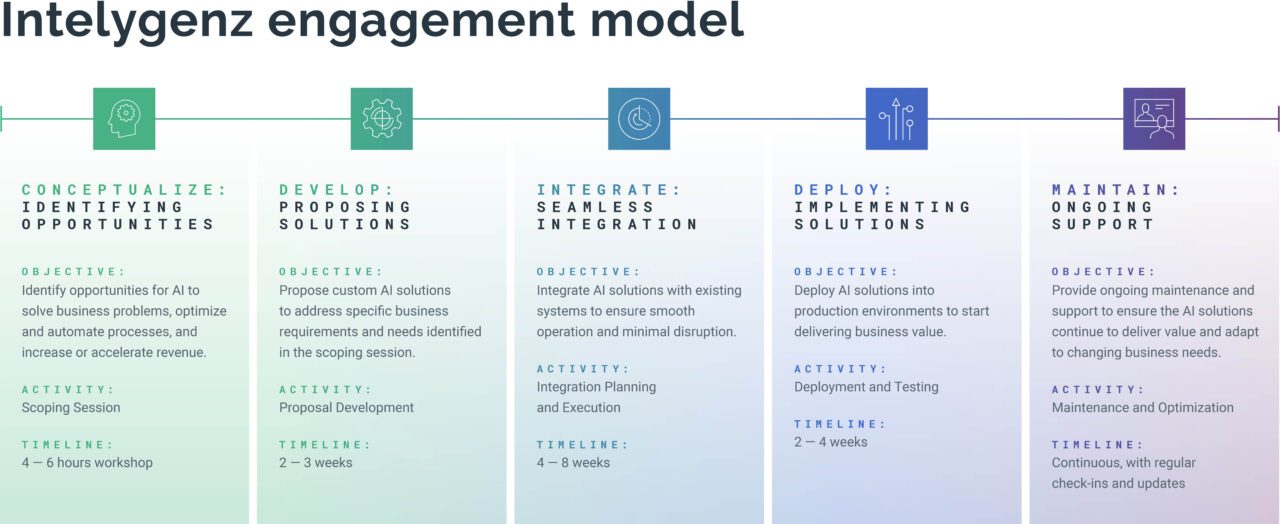

3. Implement with a proven engagement methodology

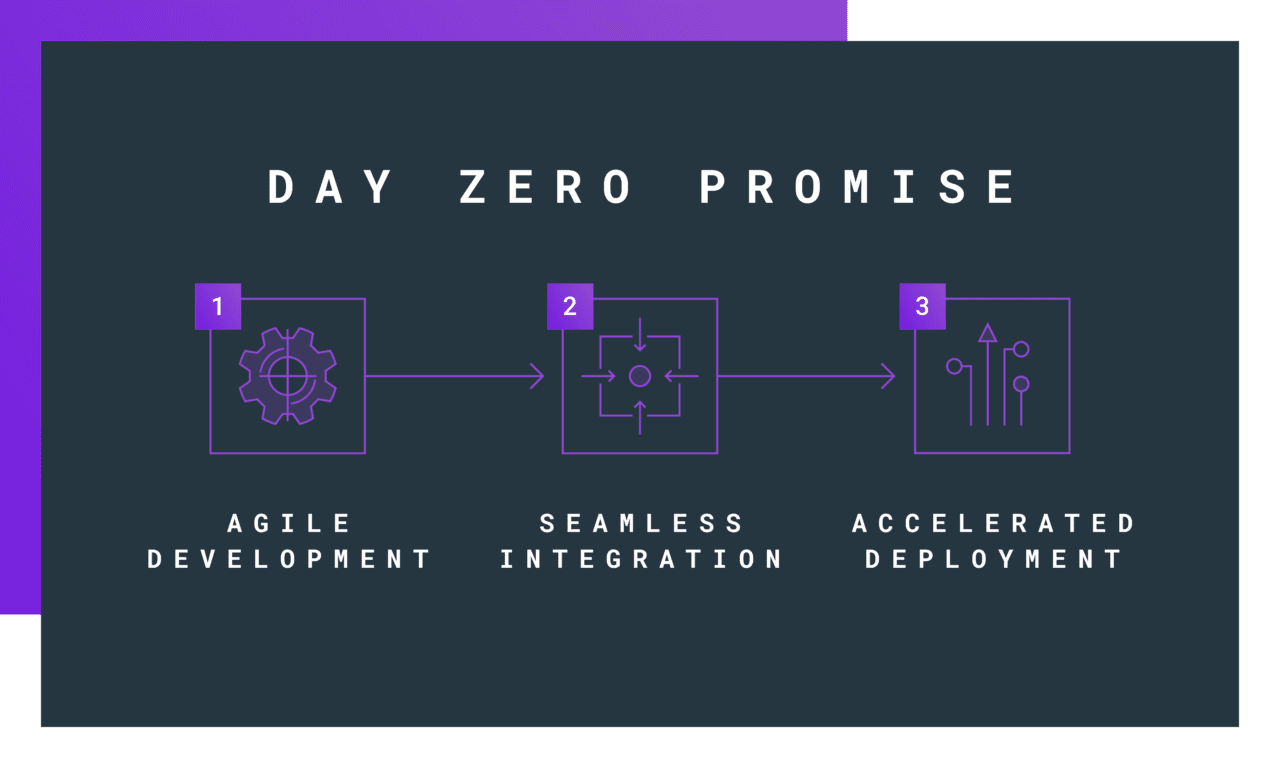

The pathway from AI concept to value realization is rarely linear. To navigate this complexity, financial institutions need a structured, end-to-end engagement methodology that enables rapid development and deployment while ensuring alignment with strategic objectives. Accenture’s “Tech Vision 2024” report emphasizes that adopting an agile, iterative approach to AI deployment enables organizations to see faster returns on investment and adjust quickly to evolving business needs (Accenture, “Tech Vision 2024″).

Intelygenz’s “Day Zero Promise” embodies this approach. Our methodology begins with a rigorous scoping session to align AI projects with strategic business outcomes from the very beginning. This is followed by:

Agile Development: An iterative approach that allows for continuous refinement and adaptation of AI solutions to evolving business needs.

Seamless Integration: Close collaboration with internal IT and business teams ensures that AI solutions integrate smoothly with existing systems and workflows.

Accelerated Deployment: Fast-tracking the time to value by deploying AI solutions in a matter of weeks, not months or years.

By maintaining a relentless focus on delivering measurable ROI, Intelygenz helps financial institutions avoid the common pitfalls of AI implementation and ensures that AI initiatives contribute directly to business growth.

4. Focus on flexibility and cost-efficiency

For many financial institutions, one of the barriers to AI adoption is the perceived cost and complexity. However, AI does not have to be prohibitively expensive or rigid. Intelygenz positions itself as a more flexible and cost-efficient alternative to top-tier AI companies. We deliver high-quality AI solutions without the overhead and rigidity often associated with larger providers, making us an ideal partner for organizations looking to innovate while managing costs.

5. A collaborative approach to AI success

AI projects are not just technical endeavors; they are fundamentally business transformations. A collaborative approach between the AI partner and the organization is crucial for success. At Intelygenz, we engage closely with our clients throughout the entire process, ensuring that every AI solution is not only technically robust but also aligned with the organization’s strategic goals. This partnership approach has led to real-world success stories where financial institutions have transformed AI from a buzzword into a business-critical capability.

Learn More at FinovateFall

For financial services leaders looking to leverage AI effectively, the path to success involves a thoughtful strategy that prioritizes business value over technology for technology’s sake. AtFinovateFall, Chris Brown, President of Intelygenz USA, will delve deeper into these themes during his keynote session, ‘Beyond the Hype: Delivering Real Business Value with AI in Financial Services’. Attendees will learn how to identify the right business challenges, evaluate strategic options for AI deployment, and implement solutions that drive tangible ROI.

Join us on day two of FinovateFall to gain actionable insights and see how Intelygenz’s expert consultancy and implementation services can help your institution harness the true potential of AI.

In today’s instant digital economy, providing your customers with a unique experience can translate to a crucial advantage for your firm. Your payments strategy plays a critical role in this.

Join this webinar and discover how to design a customer-centric payments strategy driven by choice, convenience, and speed.

Key takeaways:

Understanding Customer Needs: Learn how to identify and analyze the specific needs and preferences of your customers when it comes to payment options.

Seamless Payment Processes: Explore strategies for creating smooth and frictionless payment experiences that enhance customer satisfaction.

Discover: Find out how to personalize payment experiences to build stronger customer relationships and loyalty.

Fintech leaders, C-suite executives, and investors are facing an epic challenge: How do we adapt our customer acquisition strategies as the landscape becomes more competitive? In this article, we’ll highlight the challenges fintech companies face in customer acquisitions and the benefits of digital experience intelligence (DXI) in understanding your customer behaviors and challenges. Armed with those insights, you’ll be better able to navigate the ever-evolving fintech environment to grow your customer base and nurture your existing customers.

Want to know which of your marketing assets was most viewed by new conversions? Done!

Wondering where the common dropoff points are in your mobile app? No sweat.

Here are ten ways DXI can inform and refine customer acquisition strategies for fintech companies to acquire more of their ideal customers.

1. Identifying Acquisition Opportunities

Digital experience intelligence enables your organization to measure and analyze how users interact with your website or mobile app. Analyzing these journeys provides insight into pain points and areas of high engagement for potential customers. This initial informational process can help you tailor your product offerings and marketing outreach to engage your ideal customers.

Note: Be sure you’re targeting your ideal customers – the ones who truly need and will benefit from your products or services. Understanding who they are, and making that extra effort, will pay off with a client base that is bought in and wants your solutions to work for them.

2. Data-Driven Optimization

Leveraging insights from digital experience intelligence can help identify which marketing channels attract your target audience. In addition, user behavior analysis can measure the effectiveness of ad campaigns to optimize them across different channels.

Personalizing customer experiences is one of the most effective ways to increase engagement and conversion rates, especially during the consideration and decision-making stages. A digital experience intelligence platform like Glassbox is the easiest and most effective way to gain critical insights into how users interact with your platform.

You can then use that data to segment customers by a variety of metrics to provide more relevant, personalized digital experiences. The data gained can also be used to inform product recommendations, web content, and marketing messages, as well as cater to specific preferences, all of which can boost engagement and conversions.

4. Mobile Optimization

Nearly 40% of app uninstallations occur because people are simply not using the app. The best way to understand why customers are abandoning your app is by measuring and monitoring your customer journeys. Armed with that information, you can refine your app to ensure it’s relevant, intuitive, and user-friendly so your users are never tempted to select “Remove app.”

5. A/B Testing for Optimization

Data-driven insights are the holy grail of refining customer acquisition strategies. A/B testing enables companies to understand which versions of websites, apps, and offers perform best in attracting and converting potential customers. The insights you gain can inform continuous improvement of user experience and refine your customer acquisition strategies.

6. Proactively Addressing Customer Pain Points

Technology like Real User Monitoring (RUM) and newer iterations like Real User Experience (RUX) enable fintech companies to quickly detect and resolve technical issues.

The ability to swiftly address user experience pain points and intercept technical snags before they escalate can transform your customer’s journey from one of frustration into a smooth and responsive experience that makes them feel valued. With 80% of consumers reporting that customer experiences need to be improved, proactive engagement is your golden ticket to differentiation.

7. Unlocking More Substantial Customer Feedback with AI

Voice of the Customer (VoC) data captures customer feedback so you can gain a deeper understanding of their digital experiences. However, VoC data only represents the vocal minority—our internal analysis found that only about 4% of users provide feedback.

Fintech companies can now leverage AI to automatically compare these rated interactions to similar interactions across the entire user base. We do this at Glassbox with our Voice of the Silent (VoS) tool, which makes it easier to understand what the majority is experiencing, even when they blow off satisfaction surveys.

8. Building Customer Trust Through Transparency

Building customer trust is the most direct path to loyalty. Digital experience intelligence reveals where users hesitate to provide information or engage, which can reveal areas for improving transparency about data privacy and security measures. Addressing those concerns demonstrates your commitment to user safety, which puts you further along the path to customer trust and loyalty.

9. Clear The Biggest Hurdle: Knowing What Your Customers Want

With fintech products and services flooding the market, customers have an exhausting supply of options if you fall short of their expectations for seamless digital experiences. Understanding how they experience interactions with your website or mobile app is critical to effectively measuring, analyzing, improving, and ultimately ensuring customers feel understood and appreciated.

10. Make Customer Acquisition Everyone’s Business

Customer acquisition should be an all-encompassing, organization-wide effort – not just the job of marketing or product development. Lasting relationships are supported at multiple levels and in diverse ways, and playing that message on repeat is essential to making it stick.

Want to see what DXI actually looks like in action? Click around in Glassbox’s self-guided platform tour.

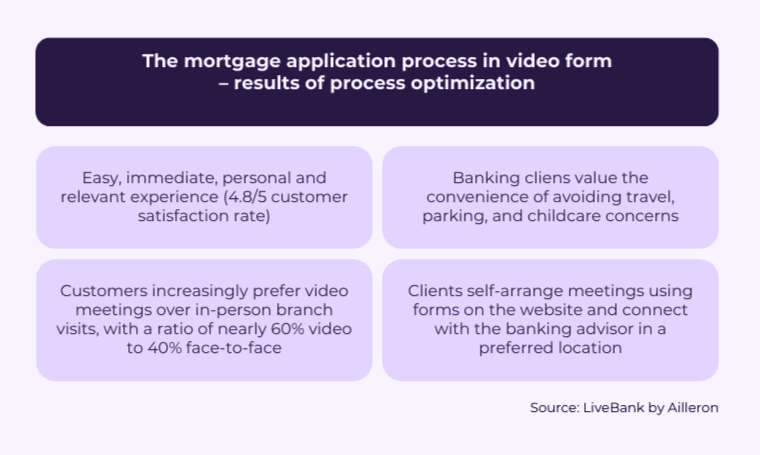

This is a sponsored article by LiveBank by Ailleron

In this digital age, the banking sector is not just undergoing change; it is at the cusp of a revolutionary transformation that is poised to redefine the very fabric of financial services. This transformative wave is powered by the synergistic relationship between human intelligence and artificial intelligence (AI). Far from merely mechanizing existing processes, this collaboration aims to completely reimagine how banking services are delivered, making them more intuitive, efficient, and customer-centric.

Transforming Human-to-Human Interaction through Technology

At the heart of this transformation is the role of Generative AI. This advanced form of AI is transforming modern banking by enhancing the human element rather than replacing it, particularly in complex sales processes. For example, while simpler banking products have become largely automated and can be easily accessed online by customers independently, more intricate products – like those involving mortgages or business financing – still benefit significantly from human insight. However, AI tools in banking is not replacing the need for human interaction; instead, it enhances the advisory services provided by banking professionals, making these interactions more productive and customer-friendly.

Entirely Digital Mortgage Application Process

A vivid demonstration of this innovative approach was showcased by LiveBank in collaboration with ING Bank on the London stage. They illustrated how digitization could reinvent the mortgage process, which has traditionally relied heavily on face-to-face interactions and extensive paperwork. By integrating AI with digital technologies, LiveBank has transformed this process to better align with contemporary customer expectations, which include a seamless digital experience, personalized service, and simplified procedures that significantly cut down on processing times.

As a leader of Retail Banking in ING emphasized during a joint speech, “Customers seek the convenience of applying for a mortgage online, uploading required documents electronically, and monitoring their application’s progress in real-time. They also prioritize transparency, clear communication, competitive interest rates, and personalized guidance throughout the mortgage journey. Ultimately, they desire a smoother and more efficient experience compared to traditional paper-based methods.”

With 45% of consumers favoring digital channels for banking product purchases, LiveBank aligns perfectly with the modern client’s preferences. It streamlines banking operations and enhances customer service by offering real-time human-to-human assistance through the customer’s first-choice communication channel.

The entire presentation and more insights are available here.

How to Redefine an Online Mortgage Experience?

ING Bank has been expanding its remote customer service capabilities, particularly for clients interested in mortgage offerings. The journey began with the option to submit applications via phone through the Contract Center, which was later extended to include customers using the services of specialists in ING’s branches.

Recognizing the evolving landscape of customer expectations, ING took the initiative to introduce video call options, marking a significant advancement in providing clients with a seamless remote banking experience. This decision entailed evaluating both customer needs and advisor perspectives.

Success Story of ING Bank & LiveBank by Ailleron

To ensure alignment with customer expectations, ING conducted comprehensive research, actively seeking feedback and insights. Valuable suggestions emerged from this process, including the need for video meetings with specialists in local branches, especially in emergency situations.

In response to these insights, ING embarked on a journey to integrate customer expectations with the capabilities offered by video support tools. This strategic alignment not only enhances the remote banking experience but also underscores ING’s commitment to innovation and customer-centricity.

This transformation is crucial in today’s banking landscape, where customer expectations are increasingly geared towards digital solutions. The transition involves not only adopting new technologies but also rethinking the customer journey to make it as frictionless as possible. By reducing the need for in-person meetings and streamlining documentation, banks can address significant pain points, making the process quicker and more pleasant for customers while also optimizing operational efficiency.

The successful digital transformation of complex banking products like mortgages requires thorough organizational preparation. It entails understanding and integrating the needs and expectations of all stakeholders involved – both customers and bank employees. This preparation is critical to ensure that the new digital channels are not just new tools but are part of a holistic strategy to improve both customer and employee experiences.

Bank Branches and Their Role in Building Customer Relations

The recent pandemic has accelerated the shift away from traditional branch-based banking towards more dynamic, digital models. This shift has prompted banks to rethink the role of physical branches. Despite their reduced footfall, branches continue to play a critical role, particularly in fostering stronger customer relationships. Recognizing this, LiveBank has innovated a new approach where loan specialists are made available to clients through convenient video calls, allowing for digital collaboration throughout the loan application process. This approach not only maintains the personal touch that is often crucial in banking but also enhances convenience and efficiency.

Furthermore, LiveBank’s method allows clients to choose how they wish to engage with the bank, emphasizing the flexibility and client autonomy that modern customers desire. This model has proved successful, leading to a majority of remote interactions with over 400 branch mortgage specialists (60% of new meetings were on video) while maintaining high levels of customer satisfaction 4.9/5 – a testament to the effectiveness of integrating personalization with digital efficiency.

How to Increase Sales in Banking Using AI & GenAI Capabilities?

The expansive capabilities of Generative AI were further highlighted at FinovateEurope in London, where banking experts showcased how AI could elevate the credit process. AI assists bank advisors by managing vast amounts of data and providing insights, thereby enhancing their ability to offer tailored advice. Additionally, the use of advanced AI-driven avatars can pre-qualify customer needs, ensuring that when a client is handed over to a human advisor, the groundwork is already laid for productive interaction.

This blend of human empathy and machine precision is crucial. It leverages the strengths of both to optimize banking operations and tailor services to individual needs, thereby not only elevating the efficiency and effectiveness of banking services but also enriching the customer experience with a personal touch that technology alone cannot provide.

Human Empathy Meets Machine Precision to Optimize Banking Operations

LiveBank exemplifies this future, standing at the forefront of the transformative journey in banking. Its platform is meticulously designed to integrate the capabilities of humans and machines seamlessly, ensuring that every customer interaction is a blend of efficiency, personalization, and security. The key to their success lies in finding the optimal balance between human and artificial intelligence, using the unique attributes of both to deliver high-quality service in real time.

In conclusion, as the banking sector moves forward, the integration of human and machine intelligence holds incredible potential. Innovations like those pioneered by LiveBank are not just enhancing operational efficiencies; they are fundamentally enriching how customers experience banking. This is a visionary journey, one that promises to transform the landscape of financial services and set new standards for the banking industry worldwide.

Mateusz Grys, LiveBank by Ailleron speaker said, “Generative AI is a major trend reshaping our industry, but the human aspect remains critical, especially in sales and advisory roles. It’s crucial for dealing with complex banking products that customers may encounter only once in their lifetime. By integrating AI, we enhance these interactions, but the empathy and understanding of human advisors are irreplaceable when navigating such significant financial decisions.”

Today’s customers want personalized experiences, but how can companies drive meaningful one-on-one connections at scale?

Data wins!

Handled correctly, well-orchestrated data reaches customers the way they want to be reached: fast and seamless while facilitating loyalty and trust.

The next generation customer experience is made easier with LeanData, the leading Revenue Orchestration platform. LeanData connects the dots for over 1,000 companies, increasing speed-to-response and aligning go-to-market motions with efficiency.

90% reduction in data duplication

78% decrease in time needed to research records

5 hours per week saved by eliminating manual processes

Time-to-response decreased from 1 to 2 days to less than 1 hour

As the banking sector stands at the precipice of a new era powered by fintech innovation, mastering the rapid deployment of AI technologies is not just beneficial—it’s imperative. At FinovateSpring 2024, Chris Brown, President of Intelygenz USA, will share pivotal insights during his keynote on “Accelerating Bank-Fintech Fusion: Deep Tech & AI Solutions in Action.” However, the core themes of his talk resonate beyond the conference, offering valuable lessons for all financial institutions navigating the complex terrain of digital transformation.

Chris Brown’s address will confront a stark reality in the fintech space: while many AI projects begin with promise, few successfully bridge the gap from development to production. An overwhelming 85% of these initiatives falter, yet Intelygenz has carved a niche in ensuring projects land within the successful 15%. This capability is not just a differentiator but a strategic imperative that positions banks to lead rather than follow in the digital age.

The keynote will explore three strategic areas where AI can significantly impact banking operations, tailored to both conference attendees and the broader industry audience:

Building Data-Driven Architecture with AI

Leveraging AI to enhance data architectures transforms the foundational operations of banking. By integrating predictive analytics for credit scoring, automated compliance monitoring, and real-time fraud detection systems, banks can enhance decision-making, ensure compliance, and secure transactions, streamlining operations while significantly improving risk management and customer trust.

Streaming AI to Automate Day-to-Day Operations

The deployment of streaming AI moves the technology from a conceptual stage to an operational necessity, automating critical operations such as transaction monitoring and customer interactions. This shift not only boosts operational efficiency but also enhances the quality of customer service, providing real-time, actionable insights that empower banks to make informed decisions swiftly.

Implementing Human Experience-Centric AI Solutions

At the heart of technological advancements lies the need to enhance human interactions. By focusing on AI-driven enhancements in customer service operations and user interfaces, banks can forge deeper connections with their customers, resulting in increased loyalty and satisfaction. From AI-enhanced financial wellness programs to advanced biometric authentication and accessibility improvements, these technologies are reshaping how banks interact with their customers.

These areas underscore Intelygenz’s expertise in rapidly transitioning AI projects from development to deployment, ensuring they not only meet but exceed their intended goals swiftly.

For those attending FinovateSpring, Chris Brown’s session will not only illuminate pathways to leveraging AI but also provide practical insights into overcoming the implementation challenges often encountered by financial institutions. For the broader audience, these themes serve as a blueprint for understanding and deploying AI technologies effectively within their organizations.

For a deeper dive into these transformative strategies, attend Chris Brown’s session at FinovateSpring, or reach out directly via his contact details for more personalized insights and solutions from Intelygenz.

By embracing these insights, banks and Fintechs can ensure they not only participate in the digital revolution but lead it, transforming potential technological disruptions into opportunities for significant growth and customer satisfaction.

About Intelygenz:

Intelygenz is a leading deep tech and AI services consultative company, specializing in delivering tailored solutions that leverage advanced technologies to drive business transformation in the banking and fintech sectors. With over two decades of expertise, Intelygenz specializes in enhancing operational efficiency and elevating customer engagement, thereby delivering measurable returns on investment. As a full-service end-to-end consultancy, Intelygenz collaborates closely with its clients’ internal teams from concept through to deployment, helping to develop, integrate, and maintain customized solutions.

Intelygenz’s key strength is its ability to facilitate rapid deployment, enabling its clients to realize tangible ROI within weeks, not months or years. Banks and fintech companies trust Intelygenz to tackle their most complex challenges, confident in the company’s capacity to support their teams in delivering critical AI-enabled projects on time and within budget.

Chris Brown, President at Intelygenz USA, is a seasoned leader in the AI and tech industry, specializing in transformative solutions for banking and fintech. Leading a team dedicated to innovation, Chris drives the development of tailored Deep Tech solutions to meet evolving client needs. LinkedIn

Moneyhub recently commissioned research into building societies and consumers, which involved interviews with building society leaders from the likes of Nationwide, Skipton, Yorkshire, Coventry, and The Building Societies Association. Additionally, 2,000 British adults were surveyed to find out about the sector’s digital readiness and the opportunities a more data-led proposition might offer.

Here’s what Moneyhub found:

Nearly 1 in 2 building society members report difficulties in engaging with their services.

80% of consumers believe that a good online platform is important when choosing a new financial provider.

66% of 18-34 year olds would like more convenient access to products and services without the need to visit physical bank branches.

Building societies are at a pivotal juncture. Traditionally known for their community focus and customer-centricity, they now face the urgent need to digitize to meet evolving consumer demands.

“Digitize or die”, a senior sector stakeholder said.

Moneyhub’s research highlights a stark reality: there is a gap between consumer expectations and the digital offerings of building societies. The company’s report – Digitize or Die: A Call to Arms for Building Societies – serves as a roadmap for building societies ready to embrace this essential transformation, ensuring they meet the needs of today’s and tomorrow’s consumers.