IT payment consultancy Icon Solutions is tackling the difficult task of helping banks offer instant payments. With PSD2 regulations looming in the U.K. and the industry’s shift to a more open banking structure, simply saying the phrase instant payments may be enough to make a banker break out in hives.

That’s where Icon Solutions comes in. At FinovateEurope 2017 the company unveiled its Instant Payments Framework (IPF). “We believe that unless banks and PSPs are using the same kind of technology as the market disruptors and internet scale providers out there, how are they able to compete?” Icon’s business development director Richard Dear asked during the demo. He added, “What we’ve done is codify Icon’s many years of experience with instant payments, within a new software product, the Instant Payments Framework, or IPF.”

Company Facts

- Founded in 2009

- Headquartered in Wimbledon, United Kingdom

- Processes 20 million payments an hour via IPF

Tom Hay (Head of Payments) and Richard Dear (Business Development Director) debut Icon Solutions’ Instant Payments Framework

We interviewed Icon Solutions’ Business Development Director, Richard Dear (pictured), in the weeks following FinovateEurope earlier this year.

We interviewed Icon Solutions’ Business Development Director, Richard Dear (pictured), in the weeks following FinovateEurope earlier this year.

Finovate: What problem does Icon Solutions solve?

Dear: Icon believes that real-time or instant payments will underpin the API economy and drive innovation. Yet, current market solutions cannot easily transition to instant payments, are heavy-weight, inflexible and don’t address the significant organizational, technical and business risks.

Icon’s Instant Payments Framework (IPF) is a light-weight software product that enables organizations to process instant payments. IPF comes with a reference implementation for each scheme, for example Faster Payments, SCT inst and TCH. We then enable our clients to graphically fine-tune these predefined message flows to quickly meet their needs. IPF has a small footprint and uses open source technology to ensure speed of deployment, high performance, low latency, and 24×7 availability whilst reducing the cost of ownership.

Finovate: Who are your primary customers?

Dear: Our primary customers are members of instant payments schemes, ranging from tier 1 banks to fintechs.

Finovate: How does Icon Solutions solve the problem better?

Dear: We’ll highlight three key areas:

- IPF complements the existing IT infrastructure. IPF is specifically focussed on instant payments and enables banks to rapidly get to market without a “rip and replace” of their existing systems

- IPF comes with a reference implementation for each scheme. Effectively we have codified our many years of expertise in instant payments within the product to smooth implementation. We then empower clients to graphically fine-tune predefined message flows to quickly meet the needs of the bank, putting the power to make changes back in the hands of the bank rather than the vendor.

- IPF has a small footprint and uses open source technology to ensure speed of deployment, high performance, low latency and 24×7 availability whilst reducing the cost of ownership. It uses similar technology to the GAFA’s and internet-scale providers, allowing banks to compete in the new world.

Finovate: Tell us about your favorite implementation of your solution.

Dear: One of the key challenges facing banks when connecting to an instant payments network is how to detect payment fraud during transaction processing. With the increased volume in transaction processing accompanying a move to instant payments, fraud control and automation of manual tasks are key factors in the success of instant payments systems.

Icon has therefore been partnering with Featurespace, the world’s leading supplier of adaptive behavioral analytics technology. Their advanced machine learning platform detects anomalies in individual behaviour to spot new fraudulent activity in real time. Featurespace’s platform will allow Icon’s Instant Payment Framework (IPF) customers to monitor their data in real time and can reduce genuine transactions declined by over 70% and manual processing by over 50%. Featurespace’s ARIC platform complements IPF’s software as both are specifically designed for real-time processing.

Finovate: What in your background gave you the confidence to tackle this challenge?

Dear: Firstly, IPF is brought to you by a team of accomplished professionals with hands-on delivery experience of local and international instant payments solutions. Icon has one of the best resource pools of instant payments knowledge globally.

Secondly, with recent advances in technology and the increasing competition from fintechs, Icon’s clients have become increasingly frustrated with traditional vendor solutions based on technologies that are now ten to twenty years old. As a result Icon performed a comprehensive review of leading edge open-source products and methodologies and their suitability to the types of projects we could see happening over the next few years.

The result has meant we are able to work with our clients to help them take advantage of these changes in several practical ways, for example moving to a DevOps approach, as well as building IPF.

Finovate: What are some upcoming initiatives from Icon Solutions that we can look forward to over the next few months?

Dear: Our focus over the next few months is on expanding the client base in Europe and the U.S., across a number of use cases, including instant payments and PSD2.

Finovate: Where do you see Icon Solutions a year or two from now?

Dear: In a year or two we would expect to see Icon acknowledged as the only organisation providing banks with similar technology to the GAFA’s and internet-scale providers, allowing them to compete in the new world of instant payments and API banking. We also look forward to being back at Finovate and showing how we have delivered other use cases based on the same transactional framework as IPF!

Tom Hay (Head of Payments) and Richard Dear (Business Development Director) debut Icon Solutions’ Instant Payments Framework:

A look at the companies demoing live at FinovateSpring on April 26 & 27 in San Jose. Pick up your tickets today and save your spot.

Assaf Frenkel, VP Product & Marketing

Assaf Frenkel, VP Product & Marketing

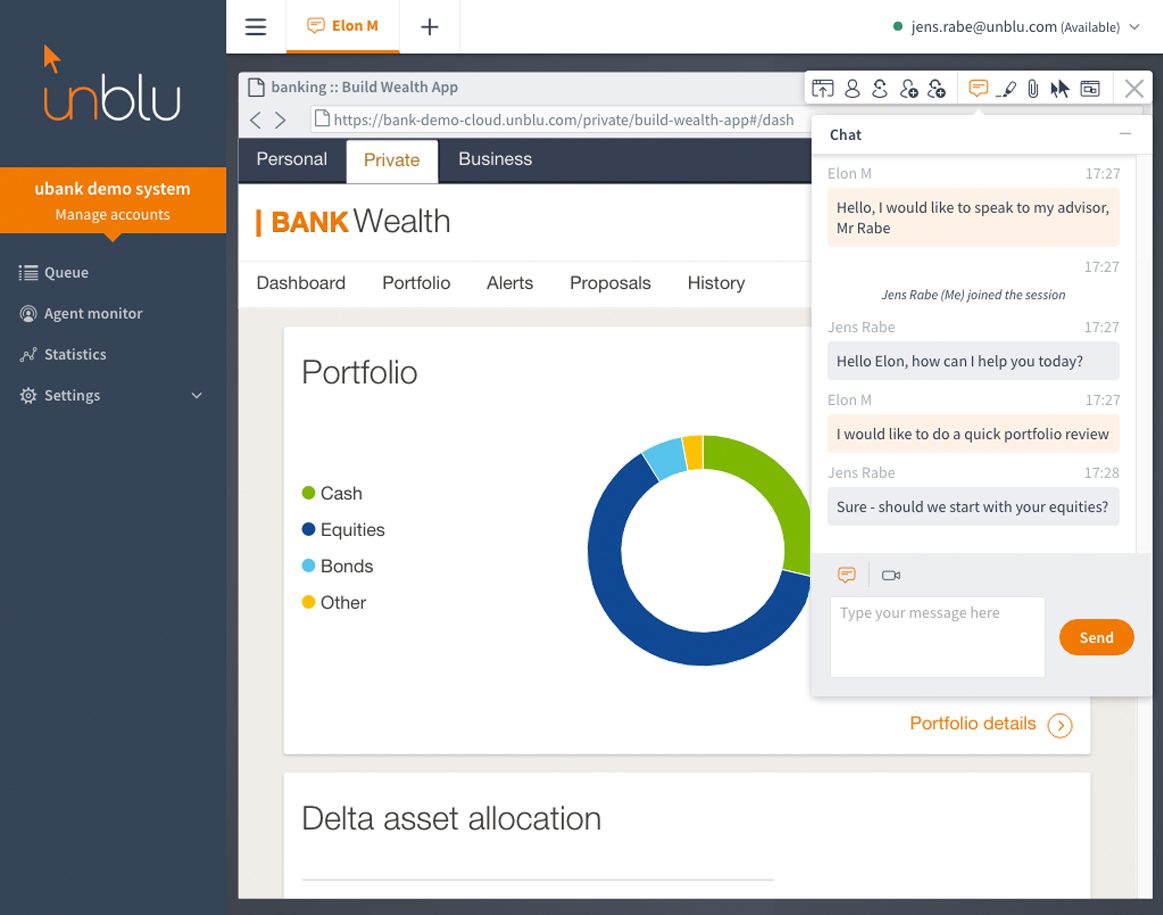

We spoke with Luc Haldimann (pictured), unblu CEO after the show and followed up with an interview.

We spoke with Luc Haldimann (pictured), unblu CEO after the show and followed up with an interview.

Presenter

Presenter