This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

When development and compliance are handled separately financial services organizations often run into challenges. These challenges can be remediated with solid IT Automation practices.

Without IT Automation a lot of time and money must be used to remain up-to-date, compliant, and secure. A robust automation strategy is an answer, and 89% of FIs agree: it is one of their top priorities. But only around 18% of the industry is doing this effectively.

Join the latest #FinovateWebinar, where we explore the focus areas that can be streamlined while deploying IT automation resulting inteams that are more productive, reduced errors, improved collaboration, and more time spent on more meaningful, thoughtful work.

The session will look at:

Identifying, preempting, and overcoming internal resistance challenges like a lack of dedicated resources and a lack of executive buy-in

Assessing where you are on the automation journey and how to get started

Overcoming complex use cases and lack of visibility to benefits

Featuring Jamil Mina, Chief Architect for Financial Services, Red Hat and David Penn, Finovate Research Analyst.

Ahead of FinovateFall Digital next week, we hear from Chad Hamblin, Global Industry Director of Financial Services at Microsoft, one of Finovate’s Gold Sponsors. Hamblin exploreswhy success will come down to understanding and empathizing with your client. Dig a little deeper into this topic with Microsoft’s eBook on the topic: Reimagine the client experience in wealth management.

COVID-19 has put a strain on everyone. We’ve all navigated social isolation, uncertain investment projections, and remote work environments. Regardless of the experience, this time away has left a haze over individuals and organizations alike. We’re not just unsure what comes next, we’re questioning the very processes we’ve accepted to this point.

Investors are feeling a new tension that makes small pain points all the more obvious. Voice automation, fixed fees, commissions — what clients once accepted as the cost of doing business are suddenly under intense scrutiny. Clients aren’t obligated to trust a major firm with their financial future, and now they’re acting on the opportunity to move their money elsewhere.

So how can wealth management firms adapt their strategies (and identities) to regain that trust? It all starts with understanding the client.

A holistic experience

Over the years, many wealth firms operated under a one-size-fits-most model — if the client fell into a specific demographic, then the firm provided a specific portfolio. Empowered by the Digital Age and amplified by this pandemic, a growing number of modern clients are looking for a wealth management partner—someone willing to listen to their ambitions, dreams, and goals and recommend actions catered to their unique circumstances. These clients want to feel identified, seen, and valued; they want to feel like more than an account number. Organizations can deliver on that expectation by creating a holistic client experience — a strategic client approach that uses technology and relationship-building to create a more inclusive perspective on the client’s needs, interests, and ambitions.

Delivering a holistic client experience comes to life in three ways: portfolios, services, and communications.

Holistic portfolios understand the client’s dreams, goals, and life events and work to build the right mix of investments to meet that individual’s financial plan, risk preference, and goals. By moving away from cookie-cutter portfolios and embracing a consultative approach, advisors create a partnership built on trust.

Holistic services encourage firms to expand their capabilities to adapt to a changing world. In the last decade, clients have become jaded by fixed-fee models. At the same time, online resources have made wealth management more accessible. By shifting to a holistic client model, organizations expand their services beyond portfolio management and provide added-value services like financial advice and planning, risk mitigation, goal tracking, wealth building strategies, and even bring in experts for specialized areas like real estate, education planning, tax mitigation, and estate planning. By expanding into capabilities that they may not have focused on before, wealth management firms further align with the individual goals of their clients and can offer one-stop solutions.

Likewise, holistic communication leverages the client’s communication preference. Every company has multiple engagement channels—voice, text, email, chat, video, social media, etc.—but most organizations assume that every client wants to be contacted via every channel. Yet, modern tools can equip firms to democratize their client data to share information and insights. By consolidating data and communication streams into a single hub of truth and by providing that information via client-friendly channels, wealth management firms can ensure that clients are engaged in the mediums they prefer.

Adapting in real time

It won’t be enough to lag behind your clients, real time adaptations and analysis will count.

While holistic client experiences serve as the star of wealth management’s future, next-generation technologies will be the foundation of these efforts. Trending tools like AI, life event and goal tracking, market risk analysis, smart portfolio allocation, and project automation equip organizations with the tools they need to build more responsive, reliable offerings for clients.

Imagine how predictive analytic tools will help determine the stability of future investments or the time employees could save on data entry through automation. Today’s technologies grant employees the tools they need to deliver a holistic customer experience by making their day-to-day tasks more efficient and effective.

Investing in trust

By creating a holistic client experience, wealth management firms become a reliable asset during hardship and a celebrated ally in victories. Right now, clients around the world are reassessing their investments for fear of a future crisis. In many cases, COVID-19 has fundamentally upset the way many clients view wealth management and building. It’s up to firms to empathize with those concerns and shape their efforts to bring peace of mind.

With a multitude of wealth firms fighting for their dollars, today’s clients are increasingly taking their funds to firms that demonstrate a conscious effort to understand their ambitions beyond executing trades. Wealth management firms that position themselves as true advisors and champion the hopes and dreams of their clients can foster trusting and long-lasting relationships.

The alternative is a slow descent into transactional business, commoditization, and ultimately irrelevance. The holistic wealth management firm is prepared to advocate for the best interests of their clients.

For more insights into how today’s firms can steel themselves for tomorrow’s challenges, read Microsoft’s latest eBook.

The following is a sponsored post from Michael Hom, Head of Financial Solutions at InterSystems, Gold Sponsors of FinovateFall Digital 2020, September 14 through 18, 2020.

Currently, external factors like the COVID-19 pandemic mean that the global economy has become increasingly volatile and capital markets firms are having to work harder than ever to make sure users, both retail and institutional, can continue to trade without interruption.

As these financial organizations look to mitigate risk in this period of uncertainty, gaining operational resilience, implementing risk mitigation strategies, and having the right technology in place will be crucial to continue to deliver value to customers, comply with regulations, get ahead of the competition – and, most importantly, maintain trust.

Given this, the pressure for incumbents to upgrade infrastructure is only increasing, but challenges remain in doing so. While the pandemic may have been the linchpin for organizations to start embracing new technologies there are still barriers to overcome and best practices to be put into play to not only mitigate risk, but also prepare capital markets for what’s to come in the future:

Replacing legacy technology

Critical to mitigating risk is ensuring data is available quickly and easily accessible. For many capital markets firms this is an area where they struggle due to a significant amount of legacy technology in their infrastructure and, consequently, data siloes.

Connecting these disparate systems will be vital to not only help them with performance issues they have today, adapting to situations such as mass remote working, for example, but also so they are capable of growing with them into the future.

This requires them to adopt solutions that can seamlessly run, scale, and expand into the cloud. By replacing legacy infrastructure, they will have the benefit of providing new technologies and innovations access to their wealth of valuable data.

These solutions should also be location agnostic to allow capital markets firms to be agile and take advantage of new technology and services and bring that into their existing infrastructure.

Investment in the future

As these institutions look to replace their legacy technology, they should focus their investments on two key areas.

First, they should invest in platform scalability as being able to scale up as the market spikes is crucial and can be a major differentiator. This scalability can even give firms a competitive edge with some firms having recently gained market share solely due their ability to scale up.

The second area of investment should be in analytics and automation that can support and, in some cases, reduce the manual-intensive workload. We’ve already seen increases in algorithmic trading and customer chatbot technologies, while many organizations within the financial services industry use AI to automate processes, such as fraud checks and compliance.

With less time spent on time-intensive manual tasks, capital markets firms will be able to direct their attention to more value-adding services for their clients. The use of AI will help to spot patterns and anomalies in those patterns much faster for fraud prevention, while also reducing the risk of human error.

Gaining access to real-time data

Is your data strategy keeping up in real-time?

Within capital markets firms, there is a growing requirement to be able to access real-time data so these organizations can simplify their stack and get access to transactions that are happening in the moment. This will allow them to produce more time-sensitive reporting so they can make appropriate business decisions and better comply with regulatory requirements.

Data fabric

Data fabrics are fast becoming a key trend within data management across the board, helping to reduce friction. Improving the accuracy, availability and accessibility of data and should also be a consideration as capital markets weather this period of uncertainty and beyond.

A data fabric that uses the latest technology will help organizations to better grasp data governance, ensure that their data is clean and accurate, to harmonize that data where appropriate, and make it more accessible. All of these will help them derive more value and better insights from their data to help drive their enterprises and those of their customers forward.

How can capital markets firms not only survive, but also thrive?

As capital markets firms look beyond this period of volatility to thriving long term, it’s vital they embrace agility by implementing modern technology with a focus on analytics and automation. This will allow them to quickly adapt to changing and new business needs by helping them to make use of their data, analyze it, monetize it, and turn it into actionable intelligence.

In an increasingly competitive landscape, where new market entrants aren’t weighed down by legacy technology and architectures, this will be a key differentiator and enable capital markets firms to take advantage of new opportunities within the market faster.

If you want to hear more about this subject, listen to this webinar in which InterSystems takes a deep dive into the challenges facing capital markets firms and how they can mitigate risk, alongside a panel of other industry experts from Northern Trust, Westwood Group, and SIX Securities & Exchanges. Or read InterSystems‘ latest blog posts on Data Excellence.

The following is a sponsored blog post by Chris Papathanassi, Global Solution Lead, Lending with Finastra. Papathanassidiscussesthe two challenges facing lenders: data quality and ensuring a true “golden source” and leveraging real value through data connections. Find out more in the full report >>

Today, digital is the only way to do business. But even though everything they do can be expressed in ones and zeros, most financial service organizations simply aren’t set up to be truly digital. In the context of the current disrupted, volatile and remote-working global economy, doing digital brilliantly is now a matter of survival and urgency for many financial firms – no longer simply a ‘nice to have’.

Digital transformation is difficult for even the simplest business models, and in lending in particular, there is a real challenge. When it can take up to three months to get cash out of the door, it’s hard to see how any bank can keep up with the digital shift. There is a continued dependency in lending on paper documentation and face-to-face contact.

Despite this, the challenges of digitalization are more than balanced out by the potential benefits. You’re likely aware of a few of these already:

Increased efficiency – removing repetitive, non-value-added work and moving towards real-time processing

Personalization – delivering relevant customer service even in a socially-distanced context

Improved credit management – providing integrated, rules-based systems for greater decision speed and transparency

Proactive risk management – using APIs and platforms to “join up” the risk and sales processes

Self-service for corporates – providing a digital channel that empowers corporate customers

Unlocking the value of data – bringing data together from disparate sources so its true value as a commodity can be leveraged

So, what needs to happen for lending to get there?

One of the key issues is data quality and the “golden source”. The bespoke nature of lending makes it hard to maintain data quality and consistency. Lenders have their own individual nuances and conventions. And corporate borrowers that have lending relationships with many different organizations will download and manipulate data so it’s in a format they can work with.

Can you trust the data?

As one major bank asked us: “How can we ensure what the source of truth is across different applications?”

What’s more, as data moves through different systems in a digitalized and connected world, it changes too.

This points to the second challenge, which is that digitalized lending data is only valuable when it can be connected to the other pieces of the puzzle, to provide the big picture lenders and borrowers need. Right now, firms are still downloading data into Excel, manipulating it, and re-sending it.

Digitalization plus API capabilities, however, makes it possible for stakeholders to see the same pieces of data in the same state. It’s this connectivity that is key to realizing the full benefits of digitalization and addressing the “source of truth” issue.

Digitalization also opens data to new technologies such as AI, machine learning, and robotic process automation, which can create new efficiencies and value for banks and customers. And for processes such as syndicated lending that have multiple players, it can be combined with cloud technology to enable more collaboration and better access to a single source of truth.

APIs in the cloud can make innovation more accessible to banks, overcoming the challenges of integrating in-house and external products. In essence, on platforms, banks have access to pre-integrated, interoperable solutions and better access to the broader financial services ecosystem, where they can explore innovations and consume them at speed.

This potentially changes the shape of the lending industry, opening up interesting questions. What do banks want to be? Leaders in the lending business or providers of specialist products? With digitalization both options are possible, creating an opportunity for lenders to add value and build their lending businesses – or to disintermediate healthily.

Mario Aquino, Founder and Managing Partner of FutureLabs Ventures, looks back at FinovateAsia Digital, and the panel on Financial Wellness: How the Digital Shift In Asia Has Created Opportunities to Better Serve The Underserved, to share his key takeaways and thoughts for the future of financial wellness.

Last month I joined a distinguished panel of speakers, including Ryan Jonghoon Kim (Group Chief Digital Officer, FWD Insurance), Lotte Schou Zibell (Regional Director, Asian Development Bank (ADB), Ankit Shrivastava (Director Digital Product, Aegon Asia), Yinglan Tan (Founding Managing Partner, Insignia Ventures Partners), and Amran Hassan (Chief Executive Officer, Etiqa Insurance and Takaful). We explored 4 questions:

What does financial wellness and serving the underserved mean to each organisation?

What are the latest exciting innovations across the payments/remittance, lending and insurance landscapes?

What are the key challenges to increase adoption of new solutions (including having a financial identity, financial literacy) and what is the impact of Covid on this?

Where are the next big opportunities and areas of impact? — as the focus moves from remittances to lending & insurance solutions and, even more broadly, goes beyond financial services to include HealthTech, EduTech & ESG solutions that benefit the underserved.

It is not my intent of this article to reiterate the full content of our session, instead I would like to focus on sharing my 3 key takeaways about Asia, the diversity and nuances it presents.

1. A quarter of a trillion in new GDP value can be created through the scale of the unbanked opportunity available in Asia

The scale of opportunity to better serve the underserved is enormous. There are 1.7B (30%) unbanked adults globally, out of which 2/3 of them own a mobile phone that could access financial services. 658M of the unbanked population live in Asia. 200M of them are expected to join an exponentially growing middle class by 2030. To provide a sense of scale of the opportunity that lies ahead, it can be estimated that if a portion of this population is converted to a banked population, a quarter of a trillion in new GDP value can be created. At FutureLabs Ventures, serving the underserved is one of our three megatrends we focus on — we call this “serving the next 1 Billion” – which is a tremendous opportunity to do well by doing good.

“Serving the next 1 Billion” – can be a great way to do well by doing good.

While the opportunity is incredibly big, there are no doubt various challenges to unlock it. These range from reaching the unbanked (especially where there is no electricity), financial identity and literacy, to fraudulent activities. One of the areas that is being widely studied by Aegon Asia, a financial services company, as shared by Ankit, is the right ecosystem to reach the unbanked, and a question being asked is ‘would digital or physical solutions be more effective for this group?’. That being said, the increase in smartphones is making access easier — and it is a trend that is only going to improve.

2. Covid-19 is a great catalyst to change consumer behaviours and leverage on the help of a broader ecosystem to create effective solution for the underserved

A significant shift in consumer behavior has been seen as a result of Covid-19, primarily in the adoption of digital non-cash payments. During the initial outbreak period, the World Health Organisation (WHO) came up with guidelines encouraging contactless payments as a measure to curb the spread of the virus. The psychological fear set in created more willingness in merchants to accept non-cash payments and use channels such as Instagram, QR Pay, E-wallets while absorbing any transaction cost for the transfer.

In our panel discussion, Amran confirmed that in markets like Malaysia, he believes this consumer behavior will stick as merchants realize the benefits from digital payments. But, in order for these consumer behaviors to continue to be adopted by the unbanked/underserved, a concerted collaboration among all ecosystem players is needed — central banks, governments, fintechs and large corporates — in order to bring to market targeted solutions that address real pain points and are interoperable. As Lotte well emphasised during our conversation, there are two critical aspects to be addressed in the process. Firstly, the basic rails for financial access – from digital identity to financial literacy; and secondly, interoperability and data protection need to be integrated right from the outset to encourage broader adoption and impact vs. the proliferation of an sub-scale set of individual solutions that don’t work with each other. If we are able to achieve this broader ecosystem collaboration, we would have put the setting for real impact at scale — where individual creativity and entrepreneurship is encouraged, but within an ecosystem that allows scale, competition as well as collaboration.

3. Financial Inclusion is not a means to an end, but rather a means to create access to Healthcare, Education and other Services

Financial access has a key role to play in day-to-day living and facilitating individuals in everything from long-term goals to unexpected emergencies. Overtime, individuals with financial access are more likely to use the access to invest in education, health, weather financial shocks and improve their overall quality of life.

As Ying Lan also shared, I truly believe there is an ever greater realization and awareness of the consequent positive effects that financial inclusion in Asia can create. These are new and sizeable customer segments that can generate new business opportunities for corporates and start-ups.

It would be wonderful to continue to see a high and close collaboration among all ecosystem participants — entrepreneurs, investors, banks, corporates and large tech firms — to unlock these opportunities and to do well while doing good!

As part of our #WomeninFintech series, Finovate speaks to inspiring women about their career in financial services and technology, their unique insights into the challenges and solutions for the industry today, and their advice for the next generation of women leaders just starting out. Today, we join Lena McDearmid, COO at Artis Technologies, a provider of embedded financial services platforms for digital, point-of-need lending and payments. Lena helped launch the startup earlier this year with a mission to refine the consumer lending experience by merging the art of technology with the science of finance to create the best consumer experience possible.

What led you to fintech and specifically down a path toward acquiring the expertise you have now?

Lena McDearmid: It started with my mother responding to an ad in the paper looking for someone to manage short-term loans from retail locations. Here I, unfortunately, learned about the negative side of lending, but also how to build programs to help get people out of destructive cycles. This inspired me to move to Atlanta where I joined an online mortgage startup company.

However, in 2008, I could see a coming shift away from the trending jumbo hybrid real-estate loans into more stable and traditional loan types. With that foresight, I moved into conventional lending where I would diversify my underwriting experience with mortgage refinances, auto loans, personal credit cards as well as debt consolidation. I learned the importance of empathizing with customers’ needs and offering more customized products based on their unique loan usage.

From there, I went to a company that focused exclusively on underwriting auto loans, where I had my first realization of a “culture-first” experience proving that employees who are happy and positively impacted by their work culture are better able to focus on the customer’s experience. I believe completely that a customer’s experience is the most important part of business.

After my time there, I was then recruited to build out the credit department at GreenSky where, for the first time, I had direct contact with technology and could see what tech could do for my operations. I spent eight years going from credit operations, to project management, and finally to technical product ownership, before leaving to start Artis.

The journey of my career is one of constant learning and growth. I am a builder of companies, products, teams, and experience. Had I not had the good fortune to walk down so many different paths, there is no way that I would be here today having the confidence knowing that at Artis, we are building a company and products that are ultimately helping the consumer with more accessible financing, the most important part of business.

Where do you see the future of the fintech heading in the next 12 months?

McDearmid: Continually increasing reliance on big data and the ability to incorporate alternative data for better decision making, especially when it comes to credit. Stronger reliance on user experience and customizations per user.

How can the financial services industry humanize AI and gain the trust of its customers? How is Artis Technologies helping?

McDearmid: It starts with the data scientists and the data. We have to know, throughout the design process, that there are humans analyzing this data. We also have to know what data elements are sensitive and understand how biases can get into the models so that we can design bias-free models and analytics. Finally, we must study the outputs and analyze their impacts on humans to ensure there are no adverse effects.

What does being one of the company’s women co-founders mean to you? And how does this set the example for other women looking to break into the field?

McDearmid: It means a great deal; most of the women in my family were entrepreneurs and as a co-founder, I now feel as if I am in their company. I imagine that the more women see other women as co-founders and leaders, this will encourage them to strive for these roles, as the women in my family inspired me. Each light on a path makes the path a little brighter and easier to follow.

How are you tackling the challenges and redefining the role of women at Artis?

McDearmid: One of the reasons I co-founded Artis was because I saw an opportunity to overcome the typical challenges women face in being heard and seen as leaders. Because Artis is a startup, it’s given me the opportunity to help define, not redefine, the importance of women and diversity at our company from the beginning. All of which are supported by my other like-minded male co-founders.

Why is it important to have multiple voices in the room, and hold each other accountable throughout the journey?

McDearmid: Diversity leads to quality. The ability to draw on multiple perspectives and experiences enriches discussions and solutions. And, without accountability, there can be no real growth, honesty, or radical transparency. Through accountability, we hold ourselves to our standards and continue our growth — regardless of gender.

What advice would you give to women starting out in fintech now?

McDearmid: Find a mentor and advocate. Believe in yourself and be assertive while learning as much as you can about all aspects of the business and industry.

There aren’t many industries where organisations have so much data about customers for such a long period of time. For example, I have had the same bank for the last 25 years which, by the way, is the same as my father’s.

My bank has been my partner when I wanted to go to university or buy my first apartment. It knows how much I make and where I spend it, but I never truly felt they used that knowledge to either enrich my experience or deliver tailored offers. Why is that?

There is a wealth of value to explore in untapped customers’ financial behaviour and banks are in prime position to reap the benefits, but they need to adapt.

The transformation has already begun with banks introducing more channels, learning best practices from digital native banks and fintechs, and even creating new digital business models to test what works, aiming to later integrate those learnings into the core business.

Still, banks are drowning in data and have very little insight on how to transform it into actionable knowledge to better serve customers, personalise offers, and deliver a consistent customer experience.

Furthermore, through segmentation, banks can use their knowledge about current customers to define campaigns and other initiatives to fulfill one of their main objectives, attract new customers. Their continuous appetite for growth steams from delivering unique and innovative value propositions to current but also future customers which today can be, in many situations, hallenging.

From risk takers, tech-savvy, and hungry for innovation customers to techavoiders that value human touch, banks must accommodate different engagement approaches and insights to differentiate customer profiles. This happens not because they don’t have the data, but because they can’t mine it.

It’s clear that very soon ‘Customer intelligence’ will be the most important predictor of revenue growth and profitability. The use of behavioural analytics will be key to identify customer friction points and there will be a surge in building technological capabilities to get more insight on customers’ needs.

A New Engagement Model for the Digital Age

By nature, financial products are complex and both companies and individuals are deeply affected by their financial choices, so there’s a foreseeable need for contact, ensuring a correct understanding of what is at stake.

Bank tellers, financial advisers, and other resources are key in accommodating customers’ requests and providing value-added and timely information. They benefit first-hand from customer insights, which enable them to provide not only a better service, but also to increase the customer value by offering the best solutions.

In addition to assisted channels, there is the emergence of self-service applications aiming to allow customers to engage on their terms, when they want, going as far as allowing customers to configure product features, including pricing. If, in this case, the human factor is eliminated, the need for accuracy is even greater, otherwise, the sale may fail or the inquiry can go unanswered.

Customer expectations have changed mainly due to the experience from other digital native organisations, coming or not, from the financial sector. The easy interactions, the tailored offers, integration between physical and digital channels or the unmatched service, creates a gap between what many financial institutions can deliver and what customers are getting elsewhere.

Responding to the pressure to change, banks must find a balance between opening but guaranteeing trust continues to be paramount, at all levels. Up to this point, the perspectives presented argued for the need for banks to not only gain insights and knowledge from the data they already have, but also the challenge in adjusting to new customers’ demands and how they choose to engage.

However, the biggest challenge is how to orchestrate these two dimensions and provide customers with experiences that leverage the knowledge banks have delivered in a seamless way, using whatever channel customers choose from.

The holy grail of an enhanced experience in the banking sector is to have an holistic and end-to-end perspective of the customer experience.

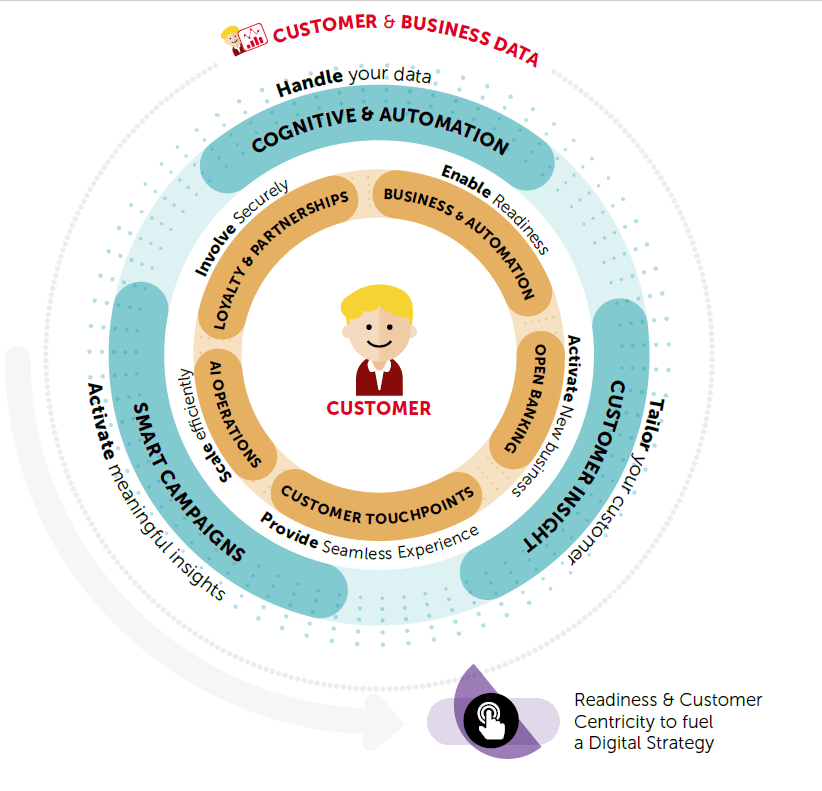

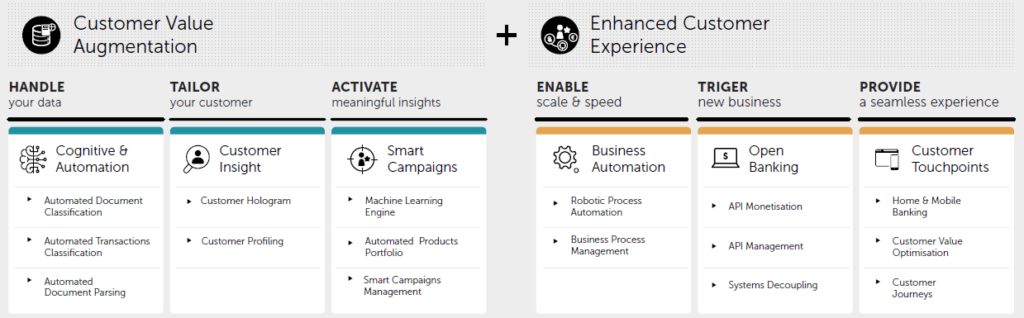

Introducing Celfocus Customer Knowledge Augmentation and Activation

Celfocus Customer Knowledge Augmentation and Activation is a modular and integrated framework tailored to leverage banks’ customer knowledge and deliver tailored services.

This framework is anchored in 2 main modules. The first comprises the tools and technologies to augment customer knowledge by activating every single customer through automated AI and Cognitive data insights, and the second aims at delivering tailored experiences that trigger new targets, portfolios, and customer lock.

By encompassing the Customer Value Augmentation and Enhance Customer Experience modules, the solution provides banks’ full control of the customer journey from planning to execution, focusing on building the technology capabilities to get more intelligence about customers’ needs, and how to best serve them.

What a week it was for the first Finovate Fintech Halftime Review; we heard from experts across the fintech spectrum, covering LendingTech, PayTech, FraudTech, BankingTech and WealthTech.

Missed some of the live sessions? Want to dig a little deeper and get the Finovate Analyst view of the first half of 2020? Well look no further, as the Finovate Fintech Halftime Review eMagazine brings all the content from the week together in one place.

Download it now and have all the latest insights at your fingertips.

Financial organizations are managing mass amounts of information on a daily basis.

Whether it’s a loan application, credit approval, or new customer records, sharing documents securely is key for effective task completion and departmental collaboration.

With a variety of document formats needed for each of these tasks, professionals must often switch from application to application to complete processes. Standard processes are often outdated and inefficient.

Discover how financial organizations can streamline their workflows and collaborate more effectively within their current applications.

It’s the FraudTech day of the Finovate Fintech Halftime Review, and we welcome Jeff Tinsley, CEO of MyLife to talk fraud management and prevention and how MyLife can be used by financial institutions to educate and add value for their consumers.

David Penn, our own Finovate Analyst, asks what sort of things go into creating a Reputation Score, and how MyLife protects people from fraud?

Watch the full interview.

Find out more about MyLife and get in touch with Tim ([email protected]) for any questions or partnership inquiries.

As part of our Finovate FinTech Halftime Review, Finovate Analyst David Penn sat down with João Lima Pinto, Chairman of ITSCREDIT. With nearly 20 years of solid experience in the financial sector, actively participating in the design and implementation of innovative omnichannel and credit solutions, Pinto has garnered much success by leading a variety of business development, product and project management, business analysis, and product operations functions.

Among the topics discussed include ITSCREDIT’S Genie Advisor app, how the company has seen the COVID-19 crisis impact its customer base, and its plan to address the challenges and move forward in 2020.

In the midst of the myriad challenges COVID-19 has thrown up for financial institutions and the people and businesses they serve, the crisis is also propeling innovation forward, proving the worth of past technological investments, and shifting the view of digital initiatives from a ‘nice-to-have’ to a ‘need-to-have’, particularly in a time of social distancing.

Against this backdrop of crisis-galvanized change, senior content producer Laura Maxwell-Bernier caught up with Sunayna Tuteja, Head of Digital Assets and Blockchain at TD Ameritrade, to talk about how she is seeing this play out, and how financial institutions should approach digital transformation to ensure relevance in the ‘new normal’.

We are also delighted to announce that Sunayna will be expanding on the themes covered in our conversation at FinovateFall in September, where she will look at the next phase of this trajectory, how changed consumer behaviors will drive further change, and what role technology will have as the dust settles.

Laura Maxwell-Bernier: Crises like COVID-19 have historically shown us how quickly technology can go from a nice-to-have to a real necessity for consumers. How are you seeing this play out in the context of COVID-19?

Sunayna Tuteja: Innovation often gains traction in times of turbulence. We are certainly witnessing that play out at massive and magnified levels in the context of COVID-19. Technologies and trends that were already in motion reached escape velocity – in scale and speed of both investment and adoption accelerating in the span of weeks vs. years. Examples include tele-medicine, online learning, and omni-channel commerce. The necessity of solving a pain point combined with a sense of urgency is activating laser-focused action that otherwise might be slowed down by inertia. In short, digital transformation is now a matter of business resiliency, representing an ultimate shift from “nice-to-have” to “need-to-have”.

Perhaps my favorite example is the Supreme Court of the United Sates (SCOTUS), an institution steeped in tradition which until recently conducted all oral arguments in person, behind closed doors and without cameras present. They too have had to adapt and transform. Last week the SCOTUS moved to hearing arguments via tele-conference, and also opened it to the public to listen in real time. While the new format may lack the usual pomp & circumstance, it ushers in an era of transparency & inclusivity. It’s a joy to witness this epic transition. Necessity is the mother of invention, or in this case adoption!

LMB: What similarities are you seeing in the way financial services organizations are responding to COVID to how they responded after the 2008 financial crisis? What lessons should we be drawing from this in our planning for the longer-term repercussions of COVID?

Tuteja: An imperative for institutions (private and public) to innovate is the rapidly closing delta between novelty and necessity. It wasn’t that long ago that the notion of banking and trading on your mobile device was unfathomable – mobile phones were for playing Candy Crush and Angry Birds! But within a matter of years, driven by a shift in consumer behaviors and expectations plus the rise of Fintech, incumbents have had to evolve and for many, the nice-to-have digital venues are now need-to-have primary on-ramps to attract, engage and retain consumers. Ergo, shocks like the global financial crisis and COVID-19 further reinforce and validate that tapping into the power of nascent yet powerful technologies to break down barriers and create next generation products/client experiences must be an evergreen endeavor. You need to maintain a persistent and pervasive focus on client-centric innovation to keep up with and surpass the evolving expectations and norms.

At TD Ameritrade, we saw this thesis come to fruition as we embarked on transitioning our employees to work from home in a matter of 10 days whilst serving millions of clients during tumultuous market conditions. The firm’s steady investments over the years in capabilities like cloud, Artificial Intelligence, messaging, mobile etc. enabled a speedy and smart transition.

LMB: What implications do you see this crisis having for the rate of adoption of digital assets – stablecoins, CBDCs and the like?

Tuteja: Digital assets are uniquely qualified for these present times. Be it as an investment vehicle akin to bitcoin’s value proposition of ‘digital gold’ or the prospect of modernizing payments, remittances, money movement or banking the unbanked/underbanked driven via stablecoins, digital wallets and CBDCs, the opportunities abound. It’s fertile ground for projects in the digital assets space, including DeFi efforts currently focused on solving these important problems. Again, this momentum is driven by heightened need as we reimagine and reconfigure our day-to-day norms in the time of/after COVID. For example: In my role leading emerging tech and partnerships, I had the opportunity to work with several Asia Tech firms in China. As someone who needs her daily dose of Starbucks, it was always amusing when I tried to pay for my drink with cash or credit card. In a society that has adopted end-to-end digital payments driven by digital wallets embedded within messaging apps like WeChat, the notion of a cash or physical credit card interaction could not be more antiquated. While the proliferation of digital wallets and QR codes have been slow to gain momentum in the U.S., current circumstances may mark a significant shift as consumers are more conscious and concerned about what they touch and who touches their card.

In this new world order, businesses will have to strike a balance between efficiency and resiliency, and as business leaders we must deliver a compounding and comparative advantage to our constituents – customers, employees, and the communities we serve. All of which will enable a good deal of change management and digital transformation to ensure long-lasting relevance. Yet in these times of hyper-change, innovation guided by the voice of the customer is always in vogue.

The confluence of these developments combined with the current macro environment garner an important inflection point in the proliferation of this nascent technology & asset class. It is therefore incumbent on the institutions that consumers know and trust, to lead with prudence and pragmatism in addressing this growing demand from consumers for education and access to digital assets, and continue the journey of bringing Wall Street to Main Street.

LMB: What does the path forward for digital transformation look like as a whole, and what do you anticipate the long-term effects on technology adoption being?

Tuteja: I’ve long maintained that anything that can be digitized will be digitized, it’s a matter of timing and led by the consumer, with technology as the enabler vs. the driver of change. An evergreen approach is key because the timing and pace of adoption is often influenced by external factors as we are witnessing at the moment. I’m reminded of examples like Webvan and Pets.com, which are often cited as failures of the dot.com bubble. Yet their contemporaries, Instacart and Chewy.com, are gaining tremendous adoption today. As an organization, you don’t want be caught off guard and unprepared, hence a persistent evaluation of the evolving consumer needs combined with a “perpetual beta” mindset in deploying new technologies is critical.

While starting with the technology can be alluring, it can lead to “shiny object syndrome” and innovation theater without much value for the end constituents. The not-so-secret secret sauce is an obsession with customer-focused innovation. A myopic focus on solving gnarly problems to deliver meaningful value by breaking down barriers that enable consumers to take charge of their financial future with confidence. If that’s powered by blockchain and AI, great, but the tech ought be secondary to the problem statement. The litmus test we apply is: What is the problem we are solving? Why is this problem worth solving? And why are we or is this tech uniquely qualified to solve this problem? It’s always better to be solving the hard problems and shipping pain-killers vs. vitamins. A strong anchor to the problem statement is also useful in maintaining focus on investing in, experimenting with and operationalizing new capabilities while averting the trappings of fads or fear of missing out.

In this new world order, businesses will have to strike a balance between efficiency and resiliency, which will enable a good deal of change management and digital transformation to ensure long-lasting relevance. Yet in these times of hyper-change, innovation guided by the voice of the customer is always in vogue.