I was looking at Geezeo's new Facebook app this morning (more on that later), and I noticed one of the best credit report monitoring ads I'd ever seen.

Instead of focusing on the negative aspects of your credit history, the banner ad features "testimonials" of the significant savings available with good credit (the banner above claims a $310 savings in her house payment). The stories are provided under the header, "Credit Diagnosis." And, I was initially impressed after clicking through the ad to find a good, landing page with more of the same.

However, the mostly-anonymous company behind the banner, FreeCreditReportsInstantly.com uses a $1, 7-day trial come-on for its $29.95/mo credit report monitoring service. I have no problem with the company charging what the market will bear. And to its credit, FreeCreditReportsInstantly (FCRI) does disclose the go-to fee on the first page of the application. But I think the typical young Facebook user is not going to be happy seeing $29.95 monthly fees on the credit or debit card.

Why would anyone pay $360/yr for credit monitoring?

The Internet was supposed to make it hard for companies to charge 2x to 3x the going rate when dozens of competitors were just a few clicks away. But here we have a company doing just that and evidently bringing in enough revenue to afford a Facebook ad buy, not to mention holding down the number 3 ad slot on Google searches for "free credit reports" (note 1)?

The answer is complex. It has to do with consumer confusion over the whole business of credit scores, ID theft, and the government-mandated free reports which is what most Googlers are looking for when they type "free credit report." And consumers must share part of the blame too. In a rush to get "something for nothing" they blindly fill out "free trial" forms without reading the fine print or taking time to investigate alternatives.

Taking the high road

But the dizzying array of credit monitoring options provides an opportunity for banks and credit unions to do the public a great service, and turn a nice profit, by educating their customers and offering value-priced alternatives:

- Credit scores/monitoring: Instead of pushing credit monitoring services that are too confusing and too expensive for the mass market, provide customers with their credit score each month, and if it takes a dive, alert the customer and provide the tools to access their credit report to investigate any potential problems (see our post yesterday and note 2).

- Identity fraud support: Citibank's Identity Theft Solutions advertising blitz was a nice humorous break from most bank advertising. However, I think it did a disservice by making full-blown identity fraud seem more commonplace than it really is. Consumers needn't be frightened, they need to be careful, they need to understand what to look for, and they need to know where to turn in the event of suspected fraud.

And since most banks and credit unions don't have the resources to provide full-service fraud assistance, turnkey solutions providers have stepped up to fill the need. We are lucky to feature one such company at our Finovate conference next Tuesday in NYC.

And since most banks and credit unions don't have the resources to provide full-service fraud assistance, turnkey solutions providers have stepped up to fill the need. We are lucky to feature one such company at our Finovate conference next Tuesday in NYC.

Full-service education and victim response from Identity Theft 911

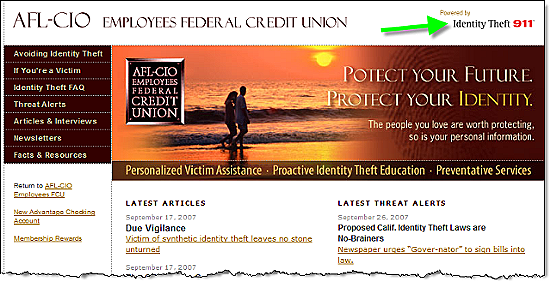

Five years ago, I met the entire Identity Theft 911 team when they were in Seattle making sales calls. It was refreshing to see someone in the identity fraud space taking a genuine interest in helping the end-user out of a jam, rather than simply trying to get them on the hook for a $150+/yr monitoring service. And over the years, I've kept in touch with the company chairman, Adam Levin, as he's worked the trade shows to garner support for Identity Theft 911 and his other company, Credit.com. Adam will take the stage Tuesday morning in NYC to demonstrate the full range of his company's resources to help banks and credit unions make their customers feel MORE secure, rather than more afraid (see screenshot below of AFL-CIO Employees Federal Credit Union's Identity Theft 911-powered services, link here).

Five years ago, I met the entire Identity Theft 911 team when they were in Seattle making sales calls. It was refreshing to see someone in the identity fraud space taking a genuine interest in helping the end-user out of a jam, rather than simply trying to get them on the hook for a $150+/yr monitoring service. And over the years, I've kept in touch with the company chairman, Adam Levin, as he's worked the trade shows to garner support for Identity Theft 911 and his other company, Credit.com. Adam will take the stage Tuesday morning in NYC to demonstrate the full range of his company's resources to help banks and credit unions make their customers feel MORE secure, rather than more afraid (see screenshot below of AFL-CIO Employees Federal Credit Union's Identity Theft 911-powered services, link here).

Note:

1. Search performed from Seattle IP address mid-morning on 26 Sep 2007.

2. For more information on credit monitoring, see the latest Online Banking Report here.