According to the Wall Street Journal, scooter sales in the U.S. are up 25% compared to last year (article here). While still relatively rare in U.S. cities, I have a feeling that 10 years from now, after a steady diet of $5/gal gas, American cities will look more like their European counterparts, with scooters zipping about everywhere.

According to the Wall Street Journal, scooter sales in the U.S. are up 25% compared to last year (article here). While still relatively rare in U.S. cities, I have a feeling that 10 years from now, after a steady diet of $5/gal gas, American cities will look more like their European counterparts, with scooters zipping about everywhere.

For banks or credit unions, this might be the ideal time to jump on the scooter bandwagon by helping customers buy the energy-efficient vehicles. It would be a great way to grab a little PR boost during the slow summer-news cycle, and with some models selling for $4,000 or more, you could boost vehicle loan outstandings by a measurable amount.

A brief Google search located two financial institutions pushing scooter loans, both appropriately with “green” in their name: South Burlington, VT-based Green Mountain Credit Union and a Wisconsin-based credit union (who’s name we removed at their request in Aug. 2010 because the offer is no longer available and they still get inquiries from this post).

Evergreen is promoting a special one-day, 3.99% scooter loan on its homepage (see screenshot below and note 1). The Saturday morning event, conducted in partnership with a local scooter dealer, included test rides, free hot dogs, and prize drawings. The CU also gave away a scooter earlier this month as part of its 50th anniversary special.

Benefits/Opportunities

- Incremental loan originations: If you are a good relationship lender, the $4,000 scooter loan today could lead to many $25,000 car loans in the future.

- Search-engine marketing: Currently, there are no direct ads running on the keywords “scooter loans,” although you will compete with several advertisers displaying against the generic “loan” in the search term. There are also few organic results for the term, so there’s a good chance an SEO-optimized landing page would rate highly in Google results.

- Leverage branch parking: One of the problems with urban scooter use is lack of available parking. Branches with parking could turn over one or more spaces for customers with scooters, creating good will, as well as the occasional picture on the 5 PM news.

- Public relations: Anything that saves gas makes for a good story this summer and beyond. It can also be pitched as a “green banking” story, although it’s not a pure environmental win. The gas savings are easy to see, but scooter emissions can be significantly higher than those of the automobiles they replace.

- Starter loan/credit: If you can convince your underwriting staff to accept applicants with limited or no credit history, the scooter loan could be a great way for young adults to build a credit file and improve their credit score (thanks, Andrea, for the idea)

- Customer acquisition: Scooter loans could be a great way to introduce younger consumers to your financial institution.

- Trendy icon: At least for urban customers, the scooter, especially the classic Vespa look, makes for an attractive graphical image, conjuring up memories of trips to Italy, or at least movies shot there on location. Your scooter program could make for good website content, eye-catching outdoor feel (great bus ad!), and or a nice flourish for other media efforts.

- Strike a deal with Scooter Financial: The number one result at Google for “scooter loans” is Scooter Financial, which does exactly what you’d expect, make loans to buy scooters. Given their name and Google pagerank, they could be an ideal company to partner with.

Cons and potential problems

- It’s an asset easily hidden from the repossession agent, so it’s harder to use the repo-threat to enforce outstanding debt.

- The accidental death rate for scooter owners is about 65% higher than that for cars; so you might want to be careful how much you push it as an “automobile alternative.” But the news isn’t all bad: Scooter owners are much less likely to perish than motorcycle owners.

- Most gas-powered scooters release significantly more pollutants than most automobiles.

- The smaller loan sizes may lead to little, if any, profits.

- Not a big market overall.

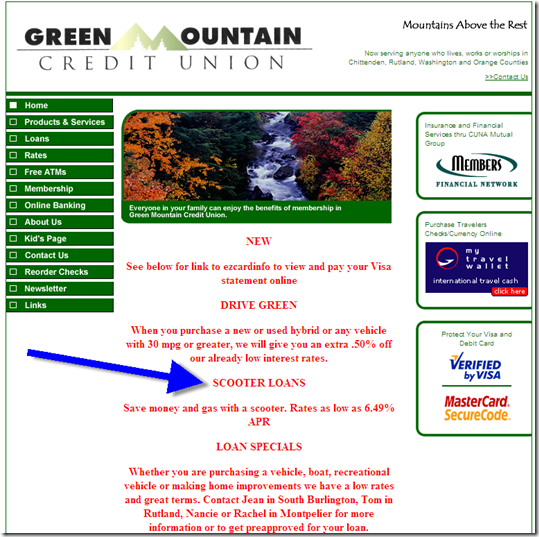

Green Mountain Credit Union homepage promotes 6.49% scooter loans

(21 May 2008)

Credit Union homepage promotes Saturday “scooter loan” special (21 May 2008)

I’ve critiqued hundreds (thousands?) of financial websites, emails, and other marketing messages. And one area that continues to be overlooked is the simple thank-you after your customer completes a transaction. I was reminded again today when testing Bank of America’s paperless statement process (see note).

I’ve critiqued hundreds (thousands?) of financial websites, emails, and other marketing messages. And one area that continues to be overlooked is the simple thank-you after your customer completes a transaction. I was reminded again today when testing Bank of America’s paperless statement process (see note).

Whatever your motivations, if you are looking to join the carbon offset trend, a company you should look at is Toronto's Zerofootprint, a non-profit information clearinghouse and source of carbon credits (see it's "carbon store"

Whatever your motivations, if you are looking to join the carbon offset trend, a company you should look at is Toronto's Zerofootprint, a non-profit information clearinghouse and source of carbon credits (see it's "carbon store"