This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Businesses today are confronted with a dizzying array of options when it comes to digital modernization and embracing technological innovation. Decision-making when it comes to technology investment is often slow, and the costs incurred when those investments do not work out as planned can be painfully high. Poor solution choices have resulted in failure rates of up to 75%, according to some estimates, and even those investments that do succeed often come with hefty price tags that can put a drag on revenues.

To learn what companies in the financial services space can do to make better technology choices, I caught up with Charlie Day, SVP, Sales and Advisory, at UPSTACK, at FinovateFall 2025 earlier this year. UPSTACK is a technology advisory platform that helps businesses reduce costs, accelerate deployment, and simplify IT decision-making. The company offers vendor-agnostic expertise, with recommendations powered by both AI and UPSTACK’s vendor experience, all informed by the firm’s proprietary dataset.

In this conversation, Day explains how UPSTACK combines a focus on long-term relationships, human expertise, and AI-powered insights to drive business success and help companies achieve their goals in an ever-evolving technology landscape.

Technological advisory has really shifted into more of a strategic relationship. It’s not just about a transaction, an event, or a sale, but a true, long-term relationship beyond the technology choice. We mix the technology expertise we have with marketing insights—everything from pricing to integration capabilities to how certain selections will mix into their overall IT landscape—to ensure that our customers are making not only the right decision in a short snapshot in time, but also what’s going to keep them achieving their goals over the long term.

Charlie Day brings more than 20 years of experience in enterprise sales and strategic partnerships. He has held leadership roles at 8×8, RingCentral, Oracle, and AT&T. Day has business degrees from the University of New Hampshire and Southern New Hampshire University.

UPSTACK is a vendor-neutral, full-service technology brokerage. Founded in 2017 and headquartered in New York City, the company provides expert advisory and execution services to help businesses make smarter technology decisions. UPSTACK works with companies across the entire technology landscape, including colocation, cloud, connectivity, networking, cybersecurity, AI, and more. With more than 60 customers in the Fortune 1000, UPSTACK recently acquired Breakwater Cloud Advisors, a CX consultancy specializing in contact center modernization, automation, and AI transformation. Christopher Trapp is UPSTACK’s Founder and CEO.

Today’s financial landscape is steered by rising consumer expectations, requiring banks to search for ways to deliver more personalized, actionable guidance to their customers. While fintech has always discussed financial wellness, it is not always easy to deliver it in a way that is embedded, intuitive, and with low friction. The banks that will take the lead in the customer journey in 2026 are the ones that will turn complex financial decisions into simple, interactive experiences that help users understand their options in real time.

Today, we’re highlighting a conversation with Chase Neinken, CRO and co-founder of Chimney, which offers banks personalized tools to help them improve the customer experience and ultimately improve their financial wellness. Recorded at FinovateFall 2025, this interview features Neinken’s thoughts on how banks can use interactive tools to deepen engagement, increase transparency, and empower consumers to make smarter financial decisions within their trusted banking channels.

But I think over the next few years, what you’re going to see, especially with AI and automation and some of the intelligence tools that are coming out, is that the winners are going to separate themselves by moving from the application layer to the infrastructure layer. So owning that data and being able and prepared to take advantage and act on it. So [consider] how you take advantage of all of the accountholder data that you have within your existing systems, not relying on third parties to do that, and then analyze that data, act on that data, and give that to the accountholders in a very convenient experience that helps your teams be more efficient and helps you grow the balance sheet in a meaningful way.

As a co-founder of Chimney, Chase Neinken brings a commercial mindset shaped by years of working with banks and fintechs to solve real consumer pain points. Neinken’s focus is on transforming static, outdated digital banking experiences into dynamic tools that guide users toward financial wellness.

Founded in 2021, Chimney is helping banks change the role they play in consumers’ financial lives by providing interactive financial tools that power more personalized, data-driven experiences within the banks’ existing channels. Chimney’s tools help users explore scenarios such as mortgage affordability and home-equity planning. For financial institutions, the New York-based company offers a plug-and-play way to increase engagement, build trust, and drive conversions without overhauling their core.

First-party fraud is a growing problem for financial institutions and retail businesses. But relative to other fraud threats—from deepfakes to account takeover—first-party fraud is often overlooked when it comes to major fraud challenges faced by businesses. Nevertheless, this type of fraud, which takes place when an individual claims to have not made a purchase they have actually made, is a problem that has only increased as ecommerce has expanded.

In this interview, conducted at FinovateFall earlier this year, I spoke with Shanti Shanmugam, Co-Founder and CEO of Casap, about the challenge of first-party fraud and dispute resolution. Shanmugam explains how AI enables Casap to instantly distinguish legitimate disputes from fraudulent claims, reducing dispute resolution costs by 90% and reducing fraud losses for clients by 51%. Shanmugam discusses why trust is at the center of both banking relationships and the dispute resolution, and how a poor dispute resolution experience can impact how much business a customer decides to do with their primary financial institution in the future.

The true cost of disputes is in trust. You are saying ‘Hey, I really did not buy this TV at Best Buy, and I really need you to have my back.’ Right now, most financial institutions, especially if they’re not working with us, take on average 90 days to resolve your case. And you’re kind of waiting in the dark the whole time. Maybe they give you a credit up front, but at the end, if they don’t get that money back from the merchant, they’re going to be clawing that money back from you 90 days later. And that’s a very trust-breaking experience. It’s the number-one reason why people are leaving their institution as a primary financial relationship: because of a negative dispute experience. So that’s the hidden cost of a dispute.

Founded in 2022 and headquartered in New York City, Casap won Best of Show in its Finovate debut at FinovateFall 2025. The company’s dispute automation and first-party fraud prevention platform automatically resolves disputes, enabling financial institutions to intelligently manage first-party fraud. The technology also transforms the dispute resolution process into an opportunity to build lasting loyalty and trust. Casap’s solution increases recovery rates, identifies and prevents fraud patterns, and delivers fast, frictionless, low-cost dispute and chargeback resolution.

For financial institutions deciding on their modernization strategy, what are the options? Does legacy technology need to be abandoned immediately or entirely? Or are there ways that financial institutions can leverage the infrastructure they have while embracing areas where digital and other modern solutions can bring real efficiency gains?

In this interview, I talk with Casey Ferguson, VP of Marketing at Zoot Enterprises, about the company’s phased approach to modernizing financial systems, integrating legacy technology, and enhancing fraud prevention strategies. Ferguson explains why incremental progress, cross-functional collaboration, and layered fraud defenses are key to effective digital transformation.

“At Zoot we look at modernization this way: It’s not about tearing everything down. When you look at this kind of rip and replace mentality you’ve got to remember that it can be pretty risky, it can be very expensive, and it can be kind of slow, as well. When you think about the pace of change, architecting the perfect environment, the world may have changed by the time you have a perfect picture of all this. So working on things incrementally and in phases can really make a difference.”

Headquartered in Bozeman, Montana, and founded in 1990, Zoot Enterprises provides acquisition, origination, and decision management solutions that help financial institutions streamline processes, increase flexibility, and accelerate growth. Zoot offers comprehensive and flexible platforms for numerous specific business operations—from loan origination and data acquisition to fraud detection and prevention.

Digital businesses in the modern era span geography, product types, and regulatory regimes, making the process of verifying identities and assessing risk difficult. Today, we’re highlighting a conversation that digs into how platforms can assess risk at scale by embedding identity and risk intelligence into a single workflow.

At FinovateFall earlier this year, I spoke with Kate Young, Marketing Manager at Middesk, a company specializing in identity verification and onboarding automation. During our conversation, Kate discussed identity and onboarding challenges, how platforms distinguish legitimate enterprises from fraudulent ones, and the importance of embedding risk intelligence and KYB tools into the onboarding and lending processes. The interview touches on real-world use cases, ROI metrics, and what it takes to move from spreadsheets to APIs.

“There’s still this… trust gap between all of the businesses and the changes that they make both legitimately and illegitimately and the understanding of those financial institutions of those businesses. So there’s a wide gap between that business identity data and financial institutions being able to trust it…. We can actually bring that [gap] much closer and financial institutions can get much closer to trusting those businesses and saying yes to them more confidently and honestly growing their portfolio with those businesses once they truly trust who they are.”

Founded in 2018, Middesk’s identity and business verification platform provides APIs for verifying B2B customers, reducing fraud risk, and automating underwriting. With features such as entity resolution, beneficial-owner monitoring, and embedded data flows, Middesk enables platforms to streamline onboarding, reduce fraud, and scale reliably by offering up-to-date, verified data about their business users and clients.

What is supplier enablement and why does it offer businesses a way to optimize vendor payments to maximize cash flow or another business outcome? How does the revolution in data management help businesses deal with the challenge of important data that is sequestered in accounting systems? And, finally, what role do automation and AI have in opening up access to that data?

Last month at FinovateFall, I interviewed Peter Zhou, Co-Founder and CEO of Rutter. Founded in 2021 and headquartered in New York City, the company offers a unified API to help companies add accounting, commerce, and payment integrations into their B2B product workflows. A trusted integration partner for companies such as Airwallex, Mercury, and Ramp, Rutter empowers businesses to build and launch products in lending, expense management, AP/AR automation, and more.

“In the same way that companies like Plaid offer a unified API for banking data, Rutter aims to be the unified API for small business financial data. Our core systems of record that we are unifying for companies are commerce, payments, accounting, and ads data … We basically help them provide customer-facing integrations into those systems of record that their customers use.”

Rutter introduced its Supplier Enablement solution earlier this year. The new offering leverages unified ERP and payment intelligence to help businesses unlock card revenue. Supplier Enablement allows Rutter to provide support for fetching vendor data from 30+ additional mid-market and enterprise ERPs, a new intelligent file import workflow, advanced OCR enrichment that uses bill attachments to improve vendor match, and integration of Visa card acceptance data to enhance vendor scoring.

Peter Zhou is a graduate of Yale University, with both Bachelor’s and Master of Science degrees in Computer Science. Before co-founding Rutter, Zhou was a software engineer with San Francisco, California-based professional services company Atrium.

Many businesses approach fintech in a fragmented way. They are forced to stitch together multiple payment systems, APIs, banking partners, and integrations just to achieve basic functionality.

Patricia Montesi, Founder and CEO of Qolo, explains in a FinovateFall video interview how her platform is solving that complexity for banks, fintechs, and enterprises. Qolo offers a unified payments stack through a single API that enables institutions to modernize their payments infrastructure without expensive and risky rip-and-replace of legacy systems.

In the video, Montesi delves into embedded ledgers, real-time rails, and how Qolo can overlay existing cores in under nine months while positioning clients for the next generation of payments, such as stablecoins and novel rails.

“We set out to build an entire, comprehensive payments stack that includes ledger, card, payments, virtual account management—everything all available through a single API served up to you so that you can then focus on your customers.”

Patricia Montesi is a seasoned payments veteran with over 20 years of experience across banking and fintech. Prior to Qolo, she held leadership roles driving innovation in payments and scaling complex platforms. Her deep domain expertise across card processing, FX, bank partnerships, and regulatory environments gives her insight into the pain points that banking partners face when retrofitting modern payments capabilities.

Qolo was founded in 2018 with the aim to simplify payments by offering a comprehensive payment stack, including an embedded ledger, card issuing, money movement, real-time reconciliation, and cross-rail connectivity on a single API. Rather than forcing banks to rip out their core, Qolo overlays its platform directly atop existing systems, enabling deployment in under nine months. This sidecar-oriented architecture lets institutions adopt new payment rails without disrupting core banking operations.

With more banking options available than ever before, winning customers and their deposits has become increasingly difficult. Differentiation is not only harder to achieve, it’s also more essential for banks and credit unions seeking growth. Yet for many institutions, finding a truly distinct value proposition can feel elusive.

This is where Wysh’s embedded life insurance product comes in. I spoke with Wysh CEO and Founder Alex Matjanec at FinovateFall last month about how his company helps banks differentiate their offerings by adding life insurance protection. The unique benefits help firms build loyalty, retention, and deeper customer relationships while also helping grow deposits.

“The main problem that we’re solving is that in America, there’s a massive underinsured gap where many Americans don’t have enough insurance. And the way they get it is actually going away, so they’re looking for new avenues to do so. On the other side, banks are looking to differentiate themselves by capturing new deposits to beat digital institutions… and we think layering in protection is the way to do so and we make it very easy to do that.”

Alex Matjanec is a serial entrepreneur with deep roots in fintech and digital product leadership. Before founding Wysh, he co-founded MyBankTracker.com, which has been called “the Expedia of banks,” and was involved in other startup ventures focused on financial tools and mobile apps. Under his leadership, Wysh has scaled from a small team to over 50 employees, expanding into dozens of US states, and forging partnerships with banks and fintechs to embed protection into deposit accounts.

Wysh was founded in 2021 to help banks increase deposits while adding value and improving customer retention. The company’s flagship solution, Life Benefit, allows banks, credit unions, and fintechs to embed micro life insurance directly into deposit accounts without requiring underwriting, opt-in steps, or extra bureaucracy.

Two weeks ago, 63 companies took the stage at FinovateFall 2025 to demonstrate their newest offerings live in front of our audience. Whether or not you were in attendance, you can now watch all of the seven-minute demo videos for free online. That’s more than seven and a half hours of fintech content, available for free.

Don’t know where to start? We’ve highlighted the six Best of Show-winning demos below to get you started.

If you don’t want to miss out on the live action next time around, be sure to register for FinovateEurope, taking place February 10 through 11 at the O2 Intercontinental in London.

The challenge of modernization remains a daunting one for many community banks and credit unions. Faced with the expense and risk of a “rip and replace” strategy on the one hand and a seemingly endless series of quick fixes, workarounds, and complex third-party relationships on the other, some financial institutions remain in a limbo of inaction.

To this end, the latest innovations from banking technology platform company Nymbus are a welcome development. In our interview with Nymbus CEO Jeffery Kendall, shared here, we talk about the current state of core banking systems, the innovative “sidecar” approach to core modernization that Nymbus offers, and the transition toward vertical banking which helps community financial institutions deliver differentiated solutions to a wider range of customers and members.

“We are a United States-focused banking technology platform. We work with community banks and credit unions (that) tend to be in the one to ten billion asset size; those are the customers we are able to help the most. We provide a full banking stack that allows them to run their core processing, their digital banking experiences, onboarding experiences … from one unified platform.”

Chairman and CEO of Nymbus since 2020, Jeffery Kendall has more than 20 years of experience in technology and financial services. He succeeded Scott Killoh, who founded the company in 2015. With Kendall as CEO, Nymbus has secured more than $123 million in funding courtesy of Series C and D rounds in 2021 and 2023, respectively. The company launched a Credit Union Service Organization (CUSO) in 2021, and has forged partnerships with financial institutions like PeoplesBank, VyStar Credit Union, and MSU Federal Credit Union.

A leading provider of banking technology solutions for financial institutions, Nymbus offers a full-stack banking platform for US banks and credit unions that helps them accelerate their growth and enhance their market positioning. The company modernizes legacy core systems for both brick-and-mortar and digital-first institutions. Nymbus also supports vertical banking strategies and the launch of subsidiary brands with a sidecar core alternative. The company is headquartered in Jacksonville, Florida.

Each year at FinovateFall, we look for new and exciting ways to showcase the breadth of fintech innovation that lies just below the radar of the mainstream fintech conversation. This year, we introduced The Impact Zone: a special program for fintech startups that gives them access to highly curated content and demos; unlimited high-level meetings with financial institutions, banks, credit unions, and venture capital firms; and a strategically located table outside the plenary hall to facilitate networking and maximum visibility.

“The Impact Zone debuted at FinovateFall this year, spotlighting eight startups with AI-driven solutions in bill management, wealth management, digital lending, and more,” Finovate VP and Director of Fintech Demos Heather Stowell explained. “Focused on growth and scaling, these innovators are ones to watch—expect to see them on the Finovate stage soon!”

Let’s meet the companies from FinovateFall 2025’s Impact Zone.

AiVantage

Headquartered in Vienna, Virginia, AiVantage provides credit unions, banks, and financial institutions with AI-powered solutions that help them improve efficiency, enable personalized customer engagement, and drive growth.

The company’s flagship solution, InteractiveAI, helps construct each customer interaction uniquely at scale to help financial institutions innovate and stay competitive. Karan Bhalla (LinkedIn) is CEO.

In June, AiVantage announced that it had secured a large strategic investment from Our Community Credit Union (OURCU). The amount of the funding was not disclosed. As part of the investment, OURCU will take a seat on the AiVantage CUSO board of directors.

Blue Street Data

Founded in 2022 and headquartered in Pittsburgh, Pennsylvania, Blue Street Data facilitates the process of finding, evaluating, and purchasing third-party data.

The company’s PQC Engine is an intelligent search platform that enables businesses to discover, compare, and buy high-quality datasets at the optimal price. Including use cases such as personalization, risk modeling, and market analysis, Blue Street Data’s technology helps financial institutions derive greater value from external data. Andy Hannah (LinkedIn) is CEO.

Earlier this year, Blue Street Data announced that it had joined the Sourcing Industry Group, also known as SIG|ORG, an international network for sourcing, procurement, and risk professionals. The company hopes its engagement with the group will elevate the standard for how organizations and businesses evaluate and transact with external data.

CloudBankin

CloudBankin offers an end-to-end cloud-based loan software solution to enhance digital lending. CloudBankin’s Loan Origination System enables a variety of financial institutions—including banks, NBFCs, and MFIs—to disburse loans in less than 10 minutes.

The company’s AI-powered lending agents monitor risk, improve decisioning, and enhance customer engagement across credit underwriting, fraud detection, document intelligence, repayment prediction, and collections. Mani Parthasarathy (LinkedIn) is CEO.

CloudBankin’s Loan Management System has delivered 97% operational efficiency, 50% reduction in time-to-market for product launch, 90% decrease in the data entry error, and 100% compliance with industry regulations. Founded in India, the company’s US headquarters is in Delaware.

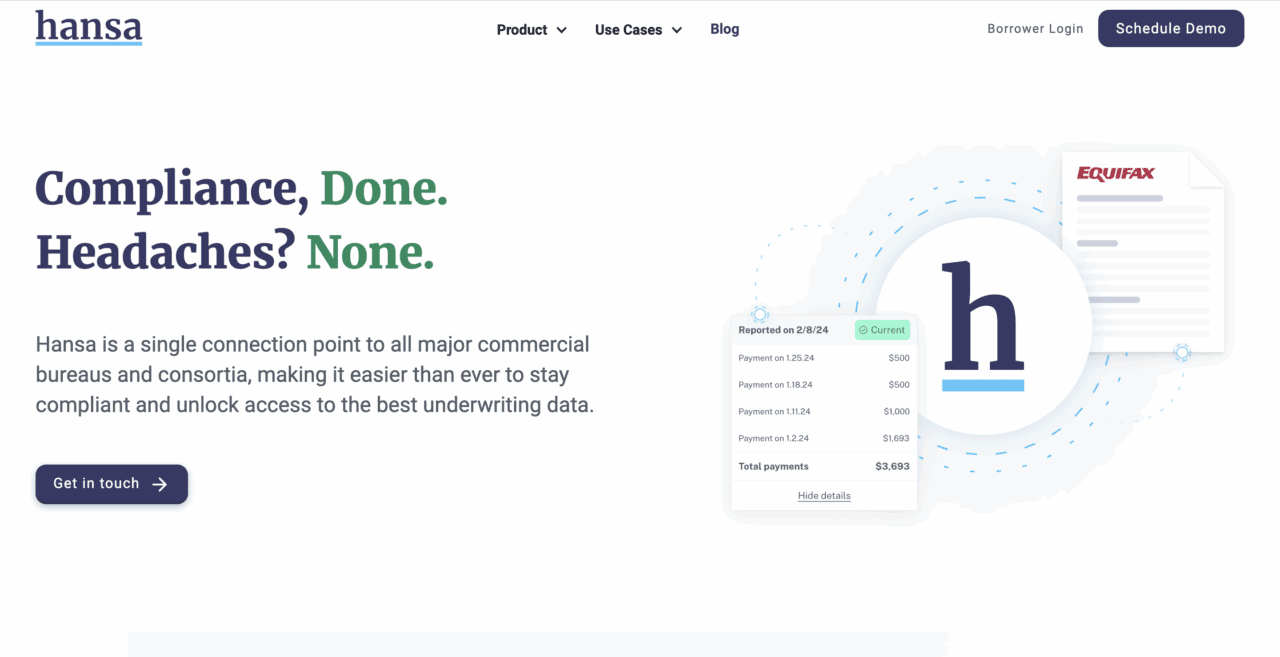

Hansa

Hansa helps lenders report commercial payment data to business credit bureaus. The company serves as a single connection point to all major commercial bureaus and consortia to make it easier for businesses to access the best underwriting data and remain compliant.

Hansa’s technology automates many of the pain points of credit reporting to help reduce delinquencies and support credit-building for small business borrowers. Henry Magun (LinkedIn) is Founder and CEO.

Founded in 2023 and headquartered in New York, Hansa began this year with the launch of its enterprise solution for commercial loan payment reporting. The new offering consists of two key components: a data reporting system that simplifies reporting by transforming and transmitting CSV file and API request data to credit bureaus, and a borrower dashboard that gives borrowers greater transparency on how their payments affect their credit.

Moneylab

Moneylab offers an AI-powered platform that enables banks and credit unions to optimize the way they manage their assets and liabilities.

Headquartered in Vancouver, British Columbia, Canada, Moneylab gives Chief Financial Officers a solution that consists of a collection of AI agents and expert systems that specialize on specific processes such as compiling and writing variance reports, monitoring loan portfolios, and pricing securities assets in real time. Vincent Wong (LinkedIn) is Moneylab Co-Founder and Chairman.

Founded in 2019, Moneylab announced this spring that it had acquired strategic intellectual property from Carfang Group. The all-share transaction will complement Moneylab’s platform offering by providing historical and current data points and analytical processes.

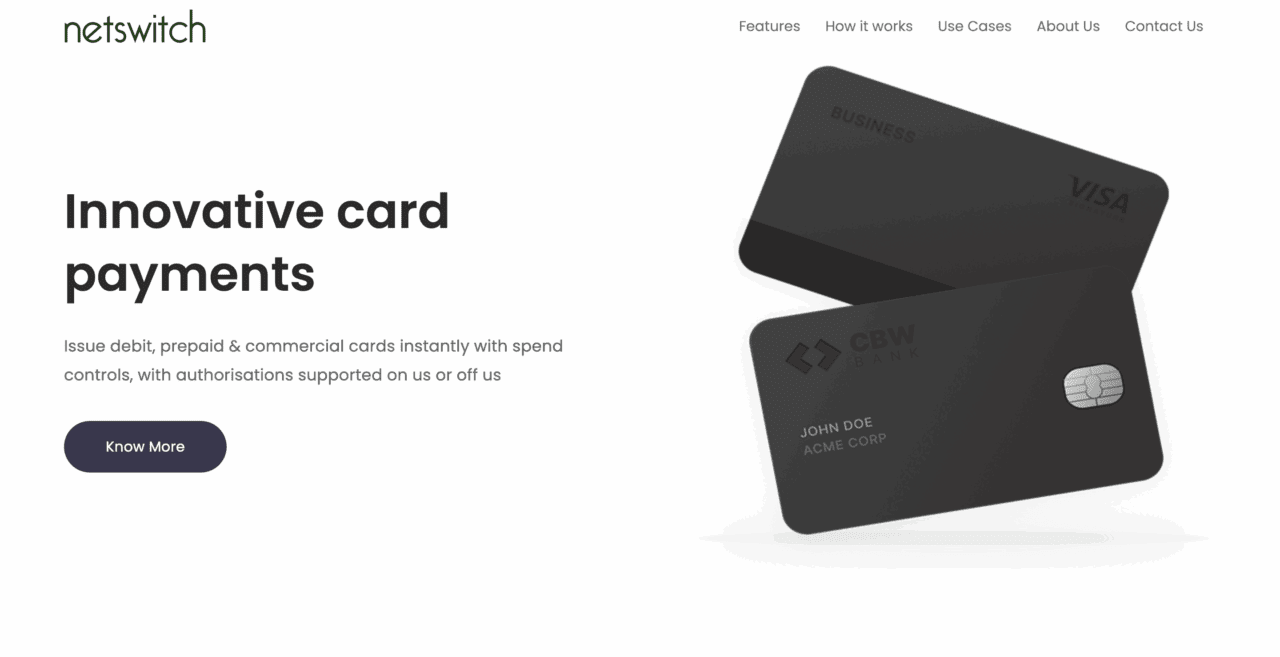

Netswitch Technologies

Netswitch offers a prepaid and debit card processing solution with a built-in ledger that is specially designed for fintechs and sponsor banks.

The company’s platform features pre-configured card controls and compliance workflows. Its custom Large Language Model (LLM) supports quick configuration and faster UI development to ensure rapid onboarding. Kris Lakshmanan (LinkedIn) is CEO.

Founded in 2020 and headquartered in Lawrence, Kansas, Netswitch supports the issuance and processing of debit, virtual, corporate, and employee cards, as well as travel and gift cards.

Nextvestment

Nextvestment offers an AI-native engagement layer for wealth management teams. The platform’s conversational co-pilots transform client questions into trusted conversations, actionable insights, and portfolio guidance.

The technology enables financial advisors to better engage with clients and provide personalized service at scale. At the same time, Nextvestment empowers clients to examine and explore their portfolio and the markets on their own, with a seamless handoff to professional advisors when they need guidance the most. Michael Davies (LinkedIn) is CEO and Founder.

Launched in 2024 and headquartered in Singapore, Nextvestment announced earlier this year that it had joined the NVIDIA Inception Program. The free, virtual accelerator enables startups innovating in AI, data science, and high-performing computing to access NVIDIA developer resources and technical training, go-to-market support and expertise, and exposure to venture capital firms via the NVIDIA Inception VC Alliance.

TrieveTech

TrieveTech offers an AI-powered, multi-tenant, white-label platform that sits at the intersection of bill aggregation, payments, analytics, insights, and customer experience enhancement to enable Energy Service Companies (ESCOs) to easily and quickly brand, customize, launch, and integrate new products and solutions. John Mulcahy is President.

Launched in 2020, TrieveTech is headquartered in Akron, Ohio. The company’s technology helps firms lower overhead costs, reduce customer care needs, and increase customer retention, leading to greater profit margins.

At a time of uncertainty in both politics and policy, an entreaty to think about “what’s possible” might sound naive—if not terrifying.

Yet, at the onset of FinovateFall 2025, which just wrapped up last week, thinking about “what’s possible” was the challenge laid down by Finovate VP and Master of Ceremonies Greg Palmer. And to the delight of our FinovateFall audience, it was a challenge that our demoing companies, keynote speakers, and insightful panelists were more than ready to accept.

What we heard from the experts

What’s possible … AI as a tool to empower and augment human action was an especially persistent theme over the three days of FinovateFall. In fact, even our pre-conference, invitation-only, Leaders+ event on Sunday evening featured a reminder that AI was increasingly the tool of choice for those under 30 when it came to a range of financial tasks from establishing a budget to making better credit decisions. Crucially, as J.D. Power’s Jennifer White pointed out, Gen Z is using AI for answers to more immediate questions, not exclusively for long-term planning. For them, AI is a co-pilot rather than a forecasting or projecting tool.

This sentiment was elaborated on by Alex Johnson of Fintech Takes in his Analyst All Stars presentation Tuesday morning. Johnson took on the notion of AI as a tool for automation, suggesting instead that AI—and Large Language Models (LLMs) more specifically—be thought of as ways to augment human activity rather than replace it outright. Johnson underscored LLMs as “probabilistic guessing machines” rather than “determinist systems,” and explained that to the extent that the latter is what’s required in financial services, LLMs alone can fall short.

That said, Johnson noted that by applying LLMs in ways that maximize what they are good at, financial institutions can leverage processes like mortgage servicing to better understand the diverse and even niche preferences of their customers. This data can be used not only to introduce new products and services, but also to scale up entire new businesses built around these edge cases.

No conversation about AI at FinovateFall would be complete without a reference to Jon Lakefish’s return to the Finovate stage for another mind-bending conversation on the latest AI tools. His Wednesday morning keynote—Creating Trust and Loyalty through AI-Enhanced CX—helped attendees understand the powerful resources available to not only build new products, but also to discover what new solutions are possible given a deeper, AI-enabled analysis of a business, its customers, and goals. In less than five minutes, Lakefish showed how a variety of readily available AI tools could enable, say, a Finovate sponsor, to uncover and pursue a new niche product line. From the latest innovations in ChatGPT—”the LLM platform for almost everything”—to Manus.AI, the first publicly available Agentic AI platform Lakefish has felt comfortable showcasing, the message was clear: the world of what’s possible is becoming larger every day and AI is a primary resource for navigating and creating within it.

One telling insight shared during our Investor All Star panel at the end of Day Three underscored the power and potential for AI when it comes to emerging fintechs, in particular. During a discussion on which trends investors were most drawn to, our panelists cited fraud prevention and compliance technology among the most attractive areas for investment, with personal finance management (PFM)-related solutions increasingly less so. Nevertheless, panelist Lindsey Fitzgerald of Vesey Ventures noted that even within this group, it was possible for truly innovative startups to stand out if they are able to deploy enabling technologies like AI in new and novel ways. “AI changes the possibility of a startup being 10x better (than its rivals) in any category,” she explained.

What we saw from the innovators

I have long contended that the roster of companies that win Best of Show at Finovate conferences in any given year is as good a heat check on the state of fintech innovation as you’re likely to find. This year’s batch of FinovateFall Best of Show winners was no exception.

By theme, FinovateFall attendees were impressed by innovations in a wide range of areas. Nevertheless companies innovating in the fraud prevention space probably experienced the greatest amount of on-stage competition—a point I’ll return to. Kudos to Casap for standing out from an impressive pack with its technology that helps combat fraud, including an especially pernicious form of e-commerce crime called “first-party fraud.” Founded in 2023 and headquartered in New York, Casap recently raised $25 million in Series A funding for its payment dispute resolution solution.

Arguably the most compelling case for financial institutions to offer services like investments came from Eko CEO Mart Vos. His company, now a two-time Finovate Best of Show winner, provides a solution that enables financial institutions to integrate digital investing functionality directly into their platforms. Vos warned banks and credit unions not to be complacent as their customers open investment accounts with innovative brokerages like Robinhood. While mere brokerages today, many of these firms are looking at ways of expanding their banking offerings, or obtaining banking licenses outright. By integrating investment services into their platforms and making them seamlessly accessible, financial institutions incentivize customers and members to keep their funds “at home.”

Enabling more qualified borrowers to secure funding is a cause championed by many innovative fintechs and it is no surprise to see two such companies among this year’s Best of Show winners. This year at FinovateFall, New York-based Krida demonstrated its AI intelligence layer for business lending. The company’s solution leverages AI to provide bankers with automated workflows for document collection, lead tracking, and data management. This enables new bankers to be more effective sooner and empowers all bankers to spend more time with their client relationships and less time with paperwork. Hailing from the other side of the country, Irvine, California-based LendAPI is a super orchestration platform that enables CTOs, CROs, and CCOs to work together to build enterprise platforms. At FinovateFall, LendAPI CEO Timothy Li demonstrated how to use the technology to launch a 1003 mortgage application in minutes. Both Krida and LendAPI are newcomers to the Finovate stage.

Another Finovate newcomer to take home Best of Show honors from FinovateFall last week was VerticeAI. The Atlanta, Georgia-based fintech provides credit unions and community banks with tools for predictive analytics, AI-powered marketing content, and targeted customer acquisition. The company began the year announcing new partnerships with Texas-based Education Credit Union and North Carolina-based Duke University Federal Credit Union.

Last but certainly not least, it was great to see the positive impression LemonadeLXP made on our FinovateFall audience last week. A Finovate alum since 2022 and, like Eko, now a two-time Best of Show winner, LemonadeLXP offers a learning experience and digital adoption platform for both the staff and customers of financial institutions. At the conference, the Ottawa, Canada-based company demoed its InsightAI solution which enables firms to develop and deploy their own employee training programs.

Where we go from here

This year I was struck by the number and quality of solutions on display that were dedicated to fighting fraud and dealing with related concerns like dispute management and chargebacks.

Fraud prevention may not be the most glamorous corner of fintech. Fraud in the digital space is a persistent, if not growing, threat to all of us; someone very close to me lost their life savings in a phishing scam earlier this year. But it’s not something that we like to talk about very much. Victims feel shame. Institutions suffer reputational damage. Providers scramble to offer their own proprietary solutions. The fraud lifecycle, so to speak, is silent and siloed. And this makes fraud harder to fight.

Perhaps this is why some of the most novel technology innovations and business strategies are found among those engaged in the fight against fraud. Consider the aggressive deployment of AI to combat deepfakes or the increasingly common collaborations between institutions—particularly credit unions and community banks—to share best practices to keep their members and customers safe. At a time when personal security concerns are paramount—in financial services and beyond—it is heartening to know that so many of fintech’s best and brightest are on the case.