This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Lloyds Bank has partnered with Visa to leverage the payment firm’s Visa Commercial Pay virtual card program.

Visa Commercial Pay is available to Lloyds Bank’s business customers.

The new tool aims to help businesses control spending, reconcile invoices, and report on expenditures.

In a world where digital banking reigns supreme, digital payment tools are king. That’s likely the motivation behind Lloyds Bank’s recent deal with Visa. The U.K.-based bank has tapped the U.S. payments giant to power its new virtual card solution.

Lloyds Bank’s is launching a new virtual card tool for businesses, Visa Commercial Pay, and is the first bank to launch Visa Commercial Pay in the U.K. The new tool aims to help small businesses to enterprises solve their purchasing and administrative challenges. For example, the solution can help them control spending, reconcile invoices, and report on expenditures.

“Visa Commercial Pay is a next generation payment platform that provides the technology to help businesses simplify and streamline the way they make payments, all in a secure and controlled way,” said Visa Managing Director, U.K. & Ireland Mandy Lamb. “We’re delighted to launch this in the U.K. in partnership with Lloyds Bank, delivering seamless payment experiences for U.K. businesses.”

Visa Commercial Pay works like most typical virtual cards in that it instantly issues virtual card numbers to businesses and their employees, allowing them to make card-not-present purchases right away. Employees can request a single or multi-use card number through their employer’s existing approval workflow and reference fields.

Employers have the option to issue cards individually or by batch and can manage spending via controls based on location, time, purchaser, and merchant.

“We’ve worked hard to create a solution that offers a secure, simplified process that enables businesses to pay their suppliers earlier while protecting their working capital,” said Lloyds Bank Head of Commercial Cards James Sykes.

Virtual card issuance has seen a spike amongst business users in the past few years. Not only has their utility increased with the rise of the digital economy, but the security of the cards has also proven a key benefit. That’s because many cards are issued for one-time or limited use, which reduces the risk for fraud and unauthorized transactions. Additionally, the control, visibility, and reporting capabilities the cards offer employers makes virtual cards a clear choice, especially among small businesses with limited resources.

Neo, an international corporate treasury services provider, has cleared more than $10.5 billion (€10 billion) in its corporate multi-currency accounts since 2020.

Founded in 2017, the company has grown from a FX hedging platform to a one-stop-shop to help corporates better manage cross-border transactions.

Neo made its Finovate debut at FinovateEurope in 2019.

International treasury services provider Neo announced today that it has cleared more than $10.5 billion (€10 billion) via its corporate multi-currency accounts since their launch three years ago. This includes a doubling of its cleared volume in less than a year, as its accounts for corporate treasurers reached $5.3 billion (€5 billion) already in 2023.

Neo CEO and co-founder Laurent Descout said that reaching the milestone was a testament to the scalability of the company’s core banking system technology. He called Neo’s innovation “machine-tooled to satisfy the growing complexity faced by international treasury teams.”

The new milestone also affirms Neo’s commitment to helping corporate treasurers navigate a global B2B cross-border payments market that is expected to top $250 trillion by 2027. This is based on estimates from the Bank of England. But it is not the size of the market alone that makes international corporate treasury operations a challenge. Growth into new markets also means securing different accounts for each new country or currency. For many corporate banks, opening an international bank account is a cumbersome and time-consuming process. Add to this the fact that many firms are unable to secure the international accounts they seek and those that do often deal with significant operational inefficiencies, including a lack of support from cross-border payment specialists.

“Accessing multi-currency accounts has literally become impossible for too many corporates across many different industries,” Descout said.

To this end, Neo offers a platform that enables businesses to set up an international account with their own multi-currency International Bank Account Number (IBAN). This will allow them to manage cash flows with supply chains, hedge FX exposure, and access transaction data from a single location. Companies can also leverage virtual wallets to allow them to make and receive payments in more than 25 different currencies. In addition to transparent and competitive pricing, Neo also offers professional support from a team of international payments specialists.

Founded in 2017 and headquartered in Barcelona, Spain, Neo made its Finovate debut at FinovateEurope 2019. From its origins as an FX hedging platform, Neo today provides treasury management services to more than 400 corporates across 28 countries. The company delivers payments in 100+ countries, and reaches 8,000+ banks via its Bank Identification Code (BIC) on the Swift network.

Invstr launched Invstr Jr., a digital bank and investing account for users under the age of 18.

When they are ready to invest, child users can send their investment proposals to the adult on the account, who can approve or decline the request.

The new Invstr Jr. accounts cost $6.25 to $7.99 per month.

Kids want to do everything their parents do, so why not let them invest… with a little help, of course. Digital banking and investment app InvstrlaunchedInvstr Jr. this week. Invstr Jr. is a custodial account to help users under the age of 18 learn how to earn, invest, and manage their finances.

When parents open an Invstr Jr. account for their child, they can schedule monthly deposits and set allowances for completing goals. Each account, offered by Vast Bank, features a checking and savings account, a debit card, a brokerage account with commission-free fractional investing, and a crypto account. When they are ready to invest, the child user can send investment proposals to the adult, who has the option to approve or decline the requests.

“At Invstr we believe that you’re never too young to start investing,” said Invstr CEO Kerim Derhalli. “We believe everyone can be an investor and can learn to invest in the same way that we learn to play a sport or a musical instrument. Investing is increasingly being recognized as a key life skill. We have made it fun and social for people to build experience and confidence safely and to learn good money habits.”

Invstr Jr. is also focused on bridging the financial health knowledge gap that young users face. Children can receive rewards for completing gamified learning modules in the Invstr Academy. And because many kids learn by doing, Invstr Jr. offers a Fantasy Finance game that allows users to manage a $1 million risk-free, virtual portfolio and create leagues to compete with friends. Within their league, players will see a leaderboard and statistics, and can chat or direct message other users or their adult.

Invstr Jr. accounts, which cost $6.25 to $7.99 per month, can include up to four kids and will have access to Invstr Pro. This solution offers the member tools to find the best investments and provides daily feedback on their portfolio risk and returns, their progress as an investor, and a personal Invstr Score.

The company’s new custodial investment account competes with Acorns, which offers Acorns Early at $5 per month, and with Greenlight, which offers investing tools within its account, that costs $4.99 per month.

U.K.-based Invstr was founded in 2013 to democratize finance. The company’s app has been downloaded more than one and a half million times in over 200 countries.

SME lending platform Credibly has partnered with Green Dot to add small business banking services to its offering.

The new solution, Credibly Business Banking, will help SMEs improve cash flow and secure capital easier and faster.

Green Dot made its Finovate debut in 2013. The company has managed more than 67 million accounts to date.

SME lending platform Credibly is adding small business banking services to its offering. Powered by Green Dot’s banking-as-a-service platform, Credibly Business Banking will enhance the banking experience for small and medium-sized businesses with improved cash flow management and faster access to financing.

Access to capital and better managing cash flow are two critical challenges for small businesses. The number of new small businesses continues to rebound in the wake of the pandemic, with small business applications in the U.S. up more than 40% from pre-pandemic levels. Unfortunately, many of these small businesses struggle to secure the financing they need to grow. Goldman Sachs revealed that more than 75% of small business owners surveyed in their 10,000 Small Businesses Voices Initiative cited access to capital as a main concern.

The hurdles are greater for those small businesses that do not have a business bank account. A Nav survey discovered that 70% of small business owners without a business bank account were rejected for loans within the past two years.

Credibly Business Banking is a response to these challenges, according to Credibly founder and co-CEO Ryan Rosett. “With a business checking account, customers will have faster and easier access to the cash, credit, and capital they need to run and grow their business,” Rosett said. The new account also features online mobile banking, fast account set-up, overdraft protection, no fees for eligible deposits, and access to a nationwide ATM network.

Founded in 2010, Credibly has facilitated more than $2 billion in financing to 30,000+ small and medium-sized businesses. Headquartered in Southfield, Michigan, the company has raised more than $82 million in total funding. Credibly Business Banking is one of a number of new products for small businesses the company has on its roadmap.

“The demand for seamless, accessible and intuitive financial tools for businesses remains on the rise,” Rosett said, “and we are thrilled to partner with Green Dot to add small business banking to complement our lending solutions.”

Founded in 1999, Green Dot has been a Finovate alum since 2013. The firm has managed 67 million accounts to date, providing banking services such as online bank accounts, debit cards, and credit solutions, as well as deposits and transfers. Green Dot has leveraged its embedded finance capabilities to enable partners from Apple to Walmart to embed scalable banking solutions into their offerings.

Newsweek named Green Dot one of its “Most Trustworthy Companies in America” earlier this year. Publicly traded on the New York Stock Exchange under the ticker GDOT, the Austin, Texas-based company has a market capitalization of $719 million.

MoneyGram is launching a non-custodial digital wallet.

The wallet will help users move funds from fiat to digital currency and back again.

MoneyGram is leveraging the Stellar Development Foundation’s open-source public blockchain Stellar for the launch.

When you think of the top crypto players in fintech, MoneyGram may not come to mind. However, the 83-year-old company continues to position itself at the forefront of the crypto space. As evidence of this, MoneyGram unveiled its non-custodial digital wallet today.

MoneyGram will launch the non-custodial digital wallet in the first quarter of next year. The wallet will help MoneyGram users leverage stablecoins to move funds from fiat to digital currency and back again. The new wallet will effectively serve as a bridge between international money transfers and blockchain payments.

With the non-custodial digital wallet, users will be able to cash out their digital asset holdings at physical MoneyGram locations, making their funds more liquid than before. The wallet, which will leverage MoneyGram’s compliance screening capabilities, will also offer account-to-account money transfers, allowing users to send digital assets to other users in the wallet.

The wallet leverages MoneyGram’s partnership with the Stellar Development Foundation (SDF), the organization behind open-source public blockchain Stellar that allows money to be tokenized and transferred globally. MoneyGram and SDF originally partnered in October of last year, when the two piloted the cash-to-crypto functionality.

“Through the services we provide in partnership with SDF, MoneyGram has made strides to create equitable access to the global financial system, having become the single largest fiat on and off-ramp provider offering blockchain access worldwide,” said MoneyGram CEO Alex Holmes.

The “non-custodial” element of MoneyGram’s wallet is notable because it will offer users control over their own private keys, which can offer more security. And because users don’t rely on a third party to manage their funds, they are less dependent on centralized institutions, which makes the wallet more decentralized, and ultimately offers a higher level of anonymity because they don’t need to provide personal information when creating or using the wallet.

After its launch, MoneyGram’s non-custodial digital wallet will be fee-free until June of 2024. The company also notes plans to expand the wallet’s capabilities with new features next year.

MoneyGram first launched its fiat on-and-off-ramp service for digital wallets in 2022 and has since expanded the service to eight digital wallets on the Stellar blockchain. Today, consumers can cash-out in 180+ countries and cash-in in 30+ countries around the world.

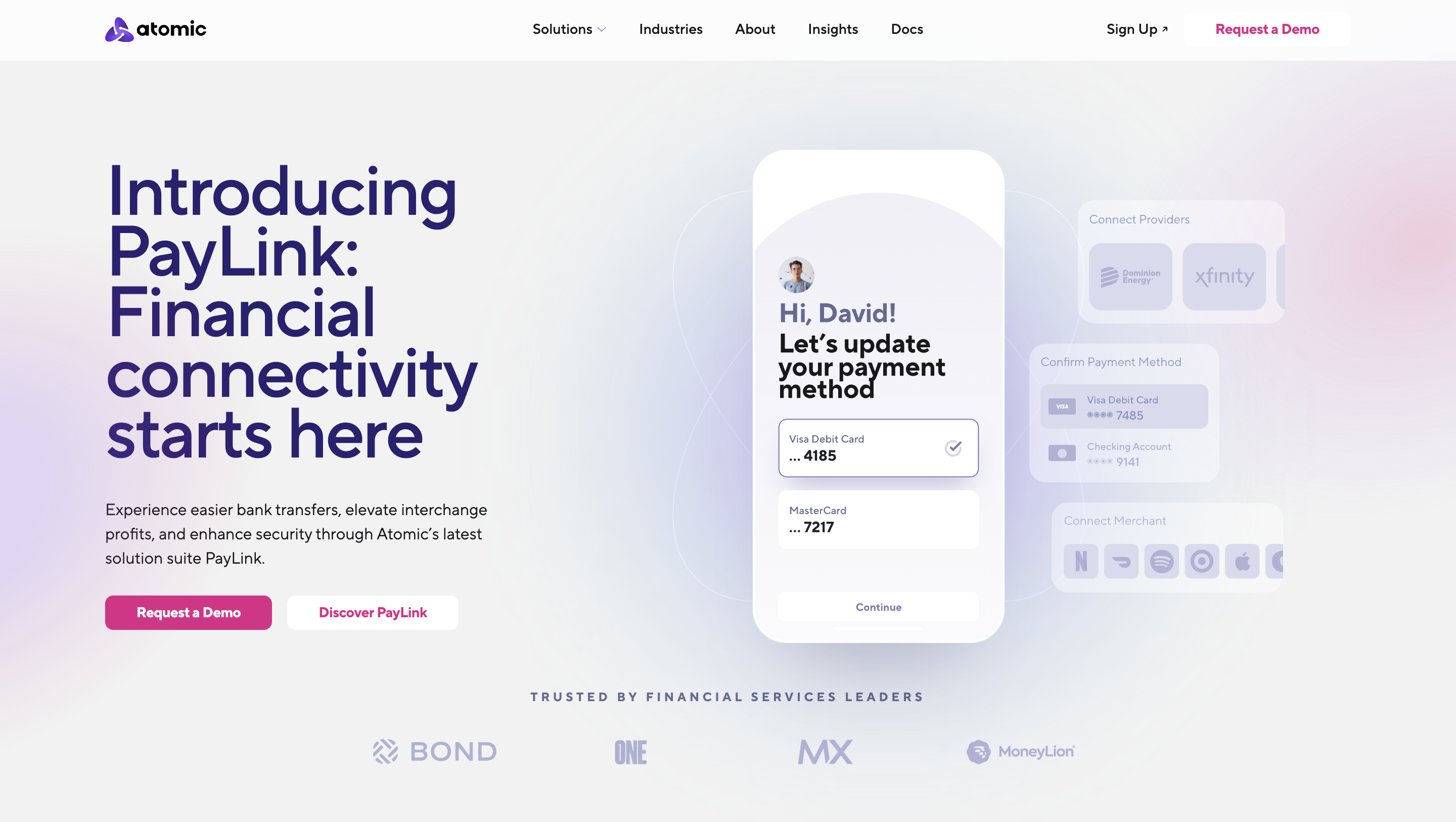

What is the future of open banking in the U.S.? Today, financial connectivity innovator AtomiclaunchedPayLink, a new suite of solutions that streamline payment switching for consumers.

The new offering provides for an improved user experience for financial services consumers. It is also a big step towards helping banks and other financial institutions align themselves with the Consumer Financial Protection Bureau’s goals with regards to open banking.

We talked with Andrea Martone, Head of Product for Atomic, to learn more about PayLink, and the drive toward a more open banking system in the U.S.

Headquartered in Salt Lake City, Utah, and founded in 2019, Atomic made its Finovate debut two years ago at FinovateFall 2021. Jordan Wright is co-founder and CEO.

Congratulations on the launch of PayLink. Tell us more about this new suite of products.

Andrea Martone: Thank you! We’re thrilled about the launch of PayLink. We’ve taken our expertise in building user-permissioned connectivity for sharing and updating data and expanded it to merchant accounts, streaming services, and recurring bill providers, enabling consumers to seamlessly update their payment methods on file and retrieve information on upcoming payments. Building PayLink was a natural next step on our journey towards helping consumers update their primary banking relationship as it helps overcome a major point of friction in the process. To build it, we leveraged our cutting-edge TrueAuth technology that allows users to authenticate directly on their devices, without ever sharing login credentials.

For our readers who are new to Atomic, can you tell us a little about the company?

Martone: At Atomic we believe that making it simple for consumers to access, share, and update their financial data is key to unlocking new financial opportunities. By embedding Atomic’s SDK into their online and mobile banking applications, financial institutions can enable consumers to easily update direct deposit instructions, verify income and employment, import W2s and, now, update payment methods on file with merchants without leaving their application. With our solutions, financial institutions help grow new account adoption, qualify borrowers, and streamline tax filing.

Open banking was a major topic of conversation at our FinovateFall conference a few weeks ago. What is your take on the state of open banking in the U.S.?

Martone: Open banking in the U.S. is at an interesting juncture. With the CFPB taking bold steps in their public commentary, there’s an exciting momentum building around the consumer-centric transformation of financial services. While Europe has been ahead in this race, the U.S. is catching up, and I believe we are headed for an ecosystem that allows for significant innovations to support both consumers and financial institutions.

One of the issues that came up in our discussion on open banking was the idea that open banking is integrally related to the issue of digital identity. Do you agree? Why is this so and why is it important to keep in mind?

Martone: Digital identity is the backbone of a secure open banking ecosystem. As we democratize access to financial data, establishing secure, verifiable digital identities becomes crucial. It’s not just about sharing data, but ensuring that the right data gets shared with the right entities for the right purposes – securely. Our TrueAuth technology, for example, is designed to enhance credential security while empowering consumers.

The CFPB is working on regulations that could impact personal data rights. What are your thoughts on these potential regulations and their impact on companies in the open banking space – as well as the impact on consumer adoption of open banking?

Martone: I view the CFPB’s focus on personal data rights as a necessary step toward fostering a fair, transparent financial ecosystem. Giving consumers greater portability over their financial data opens the door for increased innovation and competition in the financial services space. However, it also creates a wider surface area for exploitation and misuse of data, as well. As a result, regulations will need to set the standards that ensure consumer privacy and data security and, in turn, build consumer trust. For companies evolving into the open banking space, this is an opportunity to align their products with consumer-centric values, which I believe will accelerate consumer adoption and loyalty in the long run.

Atomic is headquartered in Salt Lake City, Utah. We’ve seen a surprising number of innovative fintechs headquartered in Utah. What is it like to be a tech startup in the Beehive State?

Martone: Being headquartered in Utah has been fantastic for us. The state offers a thriving tech scene, a highly skilled workforce, and a business-friendly environment. We also have a dynamic team located throughout the country, which ensures that we comprise a diverse workforce.

What can we expect to see from Atomic over the next few months and into next year?

Martone: We have a busy roadmap ahead! You can expect to see more advanced features being rolled into PayLink, further strengthening its capabilities. You will also see us double-down on our strengths in expanding connectivity where it can benefit consumers to access, share, and update data in secure, transparent, and reliable ways to expand their financial opportunities. Key to this is continuing to advance our authentication methods, including our TrueAuth technology. Additionally, we’ll be focusing on strategic partnerships to widen our reach. Our aim is to continue leading the charge in making open banking a tangible, beneficial reality for all.

Engagement banking innovator Backbase has teamed up with identity verification and fraud prevention company FrankieOne.

The strategic partnership will combine the Backbase Engagement Banking Platform with FrankieOne’s identity verification solutions.

A four-time Finovate Best of Show winner, Backbase most recently demoed its technology at FinovateFall 2021.

Engagement banking firm Backbase has forged a strategic partnership with identity verification and fraud prevention platform FrankieOne. The two companies will work together to help banks and credit unions in Australia and New Zealand onboard customers faster and more securely. The collaboration blends Backbase’s personalized banking experience platform with FrankieOne’s identity verification solutions to make it easier for customers to seamlessly and safely access digital financial services.

Courtesy of the partnership, users of Backbase’s Engagement Banking platform will be able to access a variety of KYC, AML, biometric verification, transaction monitoring, fraud detection, and compliance capabilities from a curated roster of providers. Additionally, the recent launch of Backbase’s Engagement Banking Cloud (EBC) will give its strategic partners – like FrankieOne – a single platform that supports the full customer lifecycle.

“This partnership reinforces Backbase’s global commitment to enhancing our offering and meeting the needs of financial institutions across the region,” Backbase Director of Global Head of Fintech-As-a-Service Mayank Somaiya said. “These partnerships allow us to accelerate the integration of best-in-class capabilities into the Backbase Engagement Banking Platform.”

Backbase’s announcement comes just a few days after the company reported that it was working with Judo Bank. The Australian challenger bank, launched in 2016, selected Backbase’s Engagement Banking Platform earlier this month. In August, the Amsterdam-based fintech announced partnerships with business and IT consulting company Valleysoft and fellow Finovate alum SavvyMoney. Founded in 2003, the four-time Finovate Best of Show winner most recently demoed its technology at FinovateFall 2021. At the conference, Backbase introduced its customer onboarding solution. This technology consolidates customer finances through direct deposit, billpay auto linking, and debit card account opening.

Onboarding and fraud platform FrankieOne was founded in 2017 by Simon Costello (CEO) and Aaron Chipper (CTO). The company leverages more than 350 data sources to enable businesses to quickly and securely onboard more customers. Headquartered in Australia, FrankieOne notes that its customers see a 11% uplift in match rates after transitioning to FrankieOne.

Goalsetter has partnered with MSU Federal Credit Union’s (MSUFCU’s) Reseda Group this week.

As part of the partnership, Reseda Group has invested $1 million in Goalsetter, bringing its total funding to $20.5 million.

MSUFCU will white label Goalsetter’s youth banking platform for its members and will deploy the company’s classroom curriculum across local communities.

MSU Federal Credit Union’s (MSUFCU’s) Reseda Group is taking a step toward helping members and their families create better financial futures. The group announced today it has partnered with financial literacy platform Goalsetter.

The aim of the partnership is to help members and their families build better spending, saving, and investing habits. To accomplish this, Reseda Group will offer Goalsetter’s financial education tools and resources to members and their families.

There are three significant pieces to note from today’s deal. First, Reseda Group invested $1 million in Goalsetter, boosting the New York-based company’s total funding to $20.5 million. President and CEO of Reseda Group and MSUFCU April Clobes said that Reseda Group invested in Goalsetter because it is the “best solution for credit unions that want to attract and retain the next generation of members.” She added that integrating Goalsetter’s offerings can help credit unions “increase brand affinity with Gen Z members, deposits, and overall membership numbers.”

The second big piece for Goalsetter is that MSUFCU has agreed to white label Goalsetter’s youth banking platform for its members. Thirdly, MSUFCU will deploy the Goalsetter’s classroom curriculum in local school systems and community organizations across its branch locations.

“The award-winning, proven Goalsetter platform focuses on providing financial tools, education, and innovative financial wellness content built around pop culture, memes, GIFs, and game-based learning that resonates with young consumers. It will enable MSUFCU to effectively engage with younger consumers and provide them with the personalized services they seek,” said Goalsetter CEO Tanya Van Court. “We are proud to bring these solutions to the MSUFCU member community alongside Reseda Group, an organization that has been instrumental in the growth and ongoing success of the Goalsetter platform.”

Goalsetter was founded in 2016 and helps families offer their kids a NCUA-insured savings account where they can receive allowance, a Mastercard debit card with parental controls, game-based financial education quizzes, and more.

Goalsetter fits into the same category as Greenlight, which facilitates banking services through Community Federal Savings Bank, and GoHenry, which was acquired by Acorns earlier this year.

Credit union marketplace Union Credit has announced a collaboration with financial resource network Your Money Further.

The partnership will enable users of Your Money Further to access the Union Credit Marketplace of pre-approved financing offers.

Union Credit made its Finovate debut earlier this month at FinovateFall.

Fresh of its debut at FinovateFall in New York last week, marketplace for credit unions Union Credit has announced a collaboration with financial resource network Your Money Further.

“This collaboration with Your Money Further demonstrates our commitment to expanding our reach to communities and creating a level playing field for credit unions, while also empowering consumers to accomplish their financial goals,” Union Credit Chief Revenue Officer and co-founder Barry Kirby said.

A CU Awareness company, Your Money Further helps consumers find the credit union that best suits their needs. Courtesy of the firm’s collaboration with Union Credit, credit unions in Your Money Further’s network will be able to access the Union Credit Marketplace. This will give the more than 12 million consumers who visit Your Money Further every year access to financing options from nearly 300 credit unions that are now eligible to join.

“Union Credit’s marketplace … (provides) our users wth firm, pre-approved offers of credit,” CU Awareness Executive Director Chris Lorence said in a statement, “eliminating the hassle and guesswork that comes with applying for a loan and empowering consumers to take commands of their finances.” Lorence added that the rising interest rate environment was a challenge that was making consumers increasingly anxious about their financial decision-making.

Union Credit gives consumers access to one-click credit offers embedded in their daily activities. The company’s marketplace enables credit unions to enter new markets both at the front end of purchases as well as part of a financing experience. Additionally, the marketplace gives credit unions the opportunity to boost loan volume and brand-awareness. Your Money Further users will be able to compare and choose offers and rates for home purchasing, equity loans and personal loans, and refinancing, as well as new and used auto loans – all from local credit unions looking to serve new credit-worthy members.

“Your Money Further is dedicated to empowering consumers to make financial decisions with confidence,” Lorence said, “and we’re here to help them learn more about the unique benefits of joining a credit union.”

CU Awareness is a subsidiary of Credit Union National Association (CUNA). Recall that CUNA announced just last month that it would merge with the other major credit union organization in the U.S., the National Association of Federally-Insured Credit Unions (NAFCU).

Headquartered in Santa Rosa, California and founded in 2022, Union Credit demoed its Always Approved Marketplace at FinovateFall 2023 this month. The startup has more than 130 million consumers in its publisher network and approved loan offers can be activated within 90 seconds. There is no cost to credit unions for participating in Union Credit’s marketplace. Co-founder Dave Buerger is Union Credit’s CEO.

iProov and Ping Identity announced a partnership that will bring liveness detection to Ping Identity’s DaVinci digital identity verification platform.

Liveness detection is a key component of facial biometric authentication to ensure that the person seeking access is both the right person and a real person.

Both iProov and Ping Identity are Finovate alums. iProov has won Finovate Best of Show awards on three separate occasions.

Per the partnership, iProov will deliver a DaVinci connector that integrates with its iProov Biometric Solution Suite. This will enable businesses and organizations to deploy technologies like liveness detection as part of their identity access and customer identity access management processes. Liveness detection is a key feature of facial biometric verification and authentication. It ensures that the individual seeking access is both the right person and a real person – not the product of spoofing techniques used by fraudsters and cybercriminals, techniques that range from simple photographs to deepfakes created by Generative AI.

iProov’s biometric verification solutions have been deployed by organizations from the U.S. Department of Homeland Security to UBS Group AG.

“Many organizations across the globe are already using iProov facial biometric technology to verify the online identity of citizens, workforces, and customers more securely and effortlessly than ever before,” iProov Chief Product and Innovation Officer Joe Palmer said. “Partnering with Ping Identity will help us to expand our reach even further and we’re delighted to be bringing this integration to PingOne DaVinci.”

A Finovate alum since 2017, iProov has earned Finovate Best of Show awards on three separate occasions. The company most recently demoed its technology at FinovateEurope in 2021. At the conference, iProov showed how its Flexible Authentication solution combined two of the company’s innovations – Genuine Presence Assurance and Liveness Assurance – to ensure that organizations apply the appropriate level of verification for a given situation.

Founded in 2003 and headquartered in Denver, Colorado, Ping Identity made its Finovate debut in 2012. The company’s PingOne DaVinci solution is a vendor-agnostic, no-code, identity orchestration service. DaVinci streamlines the process of integrating and deploying identity verification solutions from a variety of vendors. The solution currently has more than 100 out-of-the-box connectors to services ranging from identity to automation.

Earlier this week, Ping Identity launched its PingOne for Customers Passwordless solution. The new offering helps companies migrate toward a secure, seamless, password-free digital experience for their customers.

Quadient has integrated REPAY’s embedded payments technology into its Accounts Payable automation solution.

The embedded payments capabilities will enable Quadient clients to pay vendor and supplier invoices using digital payment methods.

By including embedded payments in the accounts payable process, companies save time, reduce costs, and benefit from increased visibility around their expenses.

Customer experience expert Quadient has teamed up with payment processing company REPAY to create a better user experience around its Accounts Payable automation solution.

Under the partnership, REPAY’s embedded payments technology will be available to companies using Quadient’s Accounts Payable automation solution. The integration will enable Quadient clients to pay vendor and supplier invoices using digital payment methods, including virtual card, ACH, Enhanced ACH and Real-Time Payments. As a result, companies save time, reduce costs, and benefit from increased visibility around their expenses.

“Both Quadient and REPAY are committed to the ongoing evolution of embedded payment solutions that drive automation while simplifying and optimizing the accounts payable process,” said REPAY EVP, Business Payments Darin Horrocks. “We’re thrilled to join forces with Quadient and look forward to working together on new ways to optimize payments and integrate our technologies for improved cash flow, streamlined internal processes, and increased customer and vendor satisfaction.”

Quadient, formerly known as GMC Software, was founded in 1924 to offer companies mailing solutions and business supplies. Over time, the company transitioned into the digital world, and now– in addition to paper mailing solutions– offers both accounts payable and accounts receivable automation tools, as well as customer communication technologies.

Atlanta, Georgia-based REPAY was founded in 2006 and offers payment processing tools to its 24,500 clients. The company, which processes $27.2 billion each year, counts clients across a range of industries, including healthcare, banking, education, automotive, and more.

While much of the talk around embedded finance centers around the end consumer, there is a lot of room for embedded finance tools in the enterprise space. Embedded payments solutions, specifically, remove friction, speed up processes around invoice payments, and create a better overall user experience.

Paysafe and Eightcap are expanding on their partnership to offer an Embedded Trading Wallet solution.

The Embedded Trading Wallet brings Paysafe’s digital wallet infrastructure together with Eightcap’s trading technology to create a white-label wallet for their shared partners and merchants.

Paysafe and Eightcap first partnered in 2016.

Global payments provider Paysafe has expanded on its partnership with online trading platform Eightcap to launch an Embedded Trading Wallet solution.

Under the agreement, the two will offer an embedded finance solution for Eightcap’s and Paysafe’s shared partners and merchants. The Embedded Trading Wallet combines Paysafe’s digital wallet infrastructure with Eightcap’s trading technology to create a white-label, plug-and-play trading and payment wallet for their retail traders.

“We’re delighted to be embarking on this strategic partnership with Eightcap and facilitating its embedded trading wallet solution through white labelling our products and services,” said Paysafe SVP of Crypto and Digital Assets Micah Kershner. “Embedded finance is the future, and we believe this solution will revolutionize the trader’s experience.”

U.K.-based Paysafe was founded in 1996. The company now offers payment processing, digital wallet, and online cash solutions connecting businesses and consumers across 250 payment types in over 40 currencies around the world. Paysafe has processed $130 billion in transactions. The company is publicly listed on the New York Stock Exchange under the ticker PSFE and has a market capitalization of $816 million.

Eightcap, which first teamed up with Paysafe in 2016, facilitates retail derivatives trading for investors in more than 120 countries. The company’s B2B embedded trading API allows partners to offer over 1,000 tradable instruments in stocks, indices, crypto, FX, and commodities.

“We are extremely excited to be entering into this new phase of our partnership. This solution will enable unparalleled payment capabilities for our global partners and traders,” said Eightcap Director of UK Patrick Murphy.