I get dozens of newsletters and marketing pitches from my various financial accounts every month. While they are interesting to me as an analyst, for the average consumer there’s rarely any actionable information.

I get dozens of newsletters and marketing pitches from my various financial accounts every month. While they are interesting to me as an analyst, for the average consumer there’s rarely any actionable information.

However, one financial company consistently drives users to its site month over month with their email missives. And they don’t even have to change the creative.

Free-credit-score provider Credit Karma simply reminds users that it’s been more than two weeks since they last checked their credit score. The company goes on to encourage users to check in every month to to make sure no adverse changes have occurred (see first screenshot below). It’s a simple yet powerful message that drives traffic to the company’s ad-supported site (see second and third screenshots).

I’ve received this message on the 16th of each month this year, except May, when I must have already visited Credit Karma in the two weeks prior. A large yellow button invites the reader to click through to see the latest score (see first screenshot).

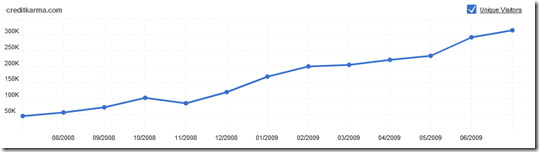

And the technique seems to be working. Traffic, measured in unique visitors by Compete, is up six-fold in the past 12 months, to 310,000 visitors in July (see chart below).

Credit Karma email (received 16 July 2009; 10:05 AM Pacific)

Subject: Credit Karma update

Current landing page after clicking “update” button in email (13 Aug 2009)

Note: Virgin Money’s friends-and-family mortgage offering is the lead product placement while The Easy Loan Site has the top banner. Lending Club is also running a banner across the top.

Landing page two months ago (16 June 2009)

Note: Virgin Money’s friends and family was also the lead product placement, while ING Direct’s Sharebuilder had the banner. Virgin Money also has a product offer in the middle of the page.

Note: For more info on the market for credit scores and monitoring see our Online Banking Report on Credit Report Monitoring (published Aug 2007).