This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

Finovate webinar, in collaboration with InterSystems, Thu 12 Oct, 3pm BST / 10am ET

How can financial services firms improve the client journey and experience? Next-generation technologies that advance digital transformation are at the heart of that answer, but these rely on the firm’s ability to gather and analyze all available data across the business.

By now, many in financial services will have adopted technologies such as AI, ML, and analytics to enhance the experience their customers receive. However, to reach their full potential, they depend heavily on a solid data technology platform to build, train, and continuously improve model quality and predictions.

Hyper-personalization can foster loyalty in an era in which loyalty has declined, and it pushes customers and investors towards those firms which can be agile in what they offer. This level of hyper-personalization offers immense growth opportunities for all providers if they can cater to small and specific groups – but on a large scale.

Watch this webinar and learn from the experts:

How to achieve competitive differentiation by delivering better customer experiences.

How to optimize your existing infrastructure with a smart data fabric.

How other firms are building these data foundations and the results of their deployment.

On the panel:

Joe Lichtenberg, Global Head of Product and Industry Marketing, InterSystems

Virginie O’Shea, CEO and Founder, Firebrand Research

How will AI help drive fintech innovation? How can digital transformation power greater financial inclusion? Where is the smart money investing in fintech? What will be the Next Big Thing in financial services?

FinovateFall wrapped up just days ago – and much of the three days of fintech demoes, keynote addresses, and panel discussions was dedicated to providing answers to these questions.

Here we’ll reflect of those responses and highlight some of the key takeaways from our mainstage fintech experts, our innovative demoing companies, and Finovate attendees themselves.

What we learned from the experts

Our invitation-only, Leaders+ session held the evening before the conference began featured a number of insights on the present and future of fintech. The lead-off address on major fintech themes set a tone for our invitees that foreshadowed much of what the rest of our attendees would see and hear once FinovateFall got underway the following morning.

Analyst and expert Alex Johnson of Fintech Takes provided one of the more surprising insights of the night in his keynote on top trends in banking and fintech. Johnson suggested that the relatively unglamorous areas of the industry may turn out to be the “Coming Attractions” in terms of fintech innovation over the near term. Much of the fintech revolution to date, Johnson explained, involved solving consumer problems – many of them bearing an uncanny resemblance to the problems of the company founder’s themselves.

As innovation in this space runs its course, opportunities in other, neglected areas can emerge. Johnson encouraged invitees to keep an eye on “the boring stuff” like payments infrastructure and the B2B world when gauging the overall level of innovation and opportunity in the fintech and financial services industry.

Johnson also observed that we should continue to see fintech deployed to solve problems that are not necessarily considered to be financial problems. Our own Finovate research team has noted the increased news flow from companies looking to help small businesses survive supply chain financing challenges. It was heartening to hear Johnson use the example of fintechs providing financing to SMEs caught in supply chain snafus in that part of his presentation.

The other major topic of conversation in our Leaders+ session was AI and the metaverse. This was another discussion that extended over the balance of FinovateFall. The jury may still be out on the impact of the metaverse in banking. But the potential of AI in fintech and financial services seems clear.

From greater personalization of services to more efficient, more secure, and more innovative financial products, banking and financial services are ready to find roles for AI.

Start with Generative AI. One commonality between keynote speakers on AI was to compare the adoption rate of a Generative AI solution like ChatGPT to the adoption rate of previous popular technologies from the past. Think everything from Napster to LinkedIn to TikTok. GenerativeAI was clearly in a class of its own. This sentiment – that AI is here to stay – was echoed in virtually every discussion of the technology – from Leaders+ and keynote speaker Tomas Chamorro-Premuzic to Analyst All-Star Tiffani Montez of Insider Intelligence. At one point, even David Letterman’s classic skewering of the Internet in an interview with Bill Gates back in 1995 (“Does radio ring a bell?”) was deployed to remind our FinovateFall audience that we’ve underestimated innovation before.

What we learned from the innovators

There is no better way to feel the pulse of fintech innovation than by attending the Demo Days at a Finovate event. And there is no better distillation of what direction fintech innovation is going than the companies that take home Finovate Best of Show awards.

FinovateFall was no exception. Of the six companies that won Best of Show last week, we saw three companies demo solutions in areas that observers long have said are ripe for innovation. Chimney demoed a solution for homeowners that gave them actionable advice on their home’s value and equity, their borrowing power, and the availability of relevant pre-qualified offers. Trust & Will demonstrated technology that streamlines and simplifies estate planning and settlement with attorney approved, legally valid documents. Wysh, an innovator in the insurance space, demoed a deposit solution that provides micro-life insurance coverage of up to 10% of the account holders balance.

Best of Show winning companies like eSelf.ai showed fintech to be at the cutting edge of enabling technologies like AI, as well. The Israel-based company, whose founder helped launch three-time Finovate Best of Show winner Voca.ai, demoed eSelf.ai’s AI-powered client interaction solution that provides human-like conversation and engagement. Mahalo Banking, headquartered in Michigan and also winning Best of Show in its Finovate debut last week, demonstrated fintech’s commitment to diversity and inclusivity. The company leverages innovative technology to deliver online and mobile banking solutions for credit unions that help them serve neurodiverse customers with visual, cognitive, and other challenges.

And the return of Debbie to the Best of Show winner’s circle is a reminder that solutions that respond to the basics of financial wellness – saving and reducing debt – remain critical components of the fintech ecosystem. Having won Best of Show in its Finovate debut last fall, Debbie was back with new tools to help users manage debt, including a credit card refinancing marketplace for credit unions.

Where we go from here

There were a few dogs that did not bark – at least not as loudly as they once did. Cryptocurrency and digital assets, for example, did not draw as much attention this year as they have in previous years. We’ve seen more from mortgagetech, as well. It is hard not to wonder what the impact of higher interest rates will have on this industry and other consumer-facing, interest-rate sensitive sectors and services from lending to Buy Now Pay Later.

Therein lies the opportunity. The problems may seem more intractable and the solutions not as sexy as they used to be. But the eagerness of founders and financial institutions to embrace both new technologies like digitization, automation, and AI – as well as new causes like financial inclusion and sustainability – is a strong sign for the future of our industry.

They are cheering in Times Square tonight as the winners of Best of Show at FinovateFall 2023 are crowned. After two days of live fintech demos from more than 60+ innovative fintechs, our delegates have decided. Here are the winners of Best of Show for FinovateFall 2023.

Chimney for its Chimney Home solution that gives homeowners actionable advice about their home value, equity, borrowing power, and pre-qualified offers. Video.

Debbie for its rewards app for debt payout and its new credit card refinance marketplace for credit unions. Video.

eSelf.ai for its technology that delivers the next generation of client-financial institution interaction, enabling human-like conversations and efficient personalization. Video.

Mahalo Banking for its intuitive and neurodiverse-inclusive online and mobile banking solutions for credit unions with tight core integrations. Video.

Trust & Will for its technology that simplifies estate planning and settlement with attorney-approved, legally valid documents. Video.

Wysh for its innovative deposit solution called Life Benefit that provides micro-life insurance coverage up to 10% of an accountholders’s balance onto an existing deposit account. Video.

We want to thank our demoing companies, our partners, our sponsors, and – last but not least – our valued attendees whose engagement continues to make Finovate a must-attend event on the fintech conference calendar. We look forward to seeing you again next year in The City That Never Sleeps for FinovateFall 2024!

Notes on methodology:

1. Only audience members NOT associated with demoing companies were eligible to vote. Finovate employees did not vote.

2. Attendees were encouraged to note their favorites during each day. At the end of the last demo, they chose their six favorites.

3. The exact written instructions given to attendees: “Please rate (the companies) on the basis of demo quality and potential impact of the innovation demoed.”

4. The six companies appearing on the highest percentage of submitted ballots were named “Best of Show.”

5. Go here for a list of previous Best of Show winners through 2014. Best of Show winners from our 2015 through 2023 conferences are below:

The financial technology landscape is ever-evolving, with innovation and creativity driving the industry forward. It’s in this dynamic environment that the Finovate Awards stand as a testament to excellence. We are thrilled to present this year’s Finovate Award winners.

The Finovate Awards honor both established institutions and rising stars that have made significant strides in delivering cutting-edge products and services to the financial sector. From breakthrough banking platforms to revolutionary AI-powered solutions, these winners have not only adapted to the demands of the modern financial world but have also set new standards for innovation and customer-centricity. Each winner was selected from the a group of finalists that demonstrated exceptional contributions to society and developed groundbreaking solutions that have reshaped the fintech landscape.

Without further ado, let’s celebrate the visionaries and innovators who have earned their place in the spotlight as this year’s Finovate Award winners.

Quadient has integrated REPAY’s embedded payments technology into its Accounts Payable automation solution.

The embedded payments capabilities will enable Quadient clients to pay vendor and supplier invoices using digital payment methods.

By including embedded payments in the accounts payable process, companies save time, reduce costs, and benefit from increased visibility around their expenses.

Customer experience expert Quadient has teamed up with payment processing company REPAY to create a better user experience around its Accounts Payable automation solution.

Under the partnership, REPAY’s embedded payments technology will be available to companies using Quadient’s Accounts Payable automation solution. The integration will enable Quadient clients to pay vendor and supplier invoices using digital payment methods, including virtual card, ACH, Enhanced ACH and Real-Time Payments. As a result, companies save time, reduce costs, and benefit from increased visibility around their expenses.

“Both Quadient and REPAY are committed to the ongoing evolution of embedded payment solutions that drive automation while simplifying and optimizing the accounts payable process,” said REPAY EVP, Business Payments Darin Horrocks. “We’re thrilled to join forces with Quadient and look forward to working together on new ways to optimize payments and integrate our technologies for improved cash flow, streamlined internal processes, and increased customer and vendor satisfaction.”

Quadient, formerly known as GMC Software, was founded in 1924 to offer companies mailing solutions and business supplies. Over time, the company transitioned into the digital world, and now– in addition to paper mailing solutions– offers both accounts payable and accounts receivable automation tools, as well as customer communication technologies.

Atlanta, Georgia-based REPAY was founded in 2006 and offers payment processing tools to its 24,500 clients. The company, which processes $27.2 billion each year, counts clients across a range of industries, including healthcare, banking, education, automotive, and more.

While much of the talk around embedded finance centers around the end consumer, there is a lot of room for embedded finance tools in the enterprise space. Embedded payments solutions, specifically, remove friction, speed up processes around invoice payments, and create a better overall user experience.

Paysafe and Eightcap are expanding on their partnership to offer an Embedded Trading Wallet solution.

The Embedded Trading Wallet brings Paysafe’s digital wallet infrastructure together with Eightcap’s trading technology to create a white-label wallet for their shared partners and merchants.

Paysafe and Eightcap first partnered in 2016.

Global payments provider Paysafe has expanded on its partnership with online trading platform Eightcap to launch an Embedded Trading Wallet solution.

Under the agreement, the two will offer an embedded finance solution for Eightcap’s and Paysafe’s shared partners and merchants. The Embedded Trading Wallet combines Paysafe’s digital wallet infrastructure with Eightcap’s trading technology to create a white-label, plug-and-play trading and payment wallet for their retail traders.

“We’re delighted to be embarking on this strategic partnership with Eightcap and facilitating its embedded trading wallet solution through white labelling our products and services,” said Paysafe SVP of Crypto and Digital Assets Micah Kershner. “Embedded finance is the future, and we believe this solution will revolutionize the trader’s experience.”

U.K.-based Paysafe was founded in 1996. The company now offers payment processing, digital wallet, and online cash solutions connecting businesses and consumers across 250 payment types in over 40 currencies around the world. Paysafe has processed $130 billion in transactions. The company is publicly listed on the New York Stock Exchange under the ticker PSFE and has a market capitalization of $816 million.

Eightcap, which first teamed up with Paysafe in 2016, facilitates retail derivatives trading for investors in more than 120 countries. The company’s B2B embedded trading API allows partners to offer over 1,000 tradable instruments in stocks, indices, crypto, FX, and commodities.

“We are extremely excited to be entering into this new phase of our partnership. This solution will enable unparalleled payment capabilities for our global partners and traders,” said Eightcap Director of UK Patrick Murphy.

Environmental, social, and governance– better known as ESG– initiatives are hot topics across the fintech and banking sectors. And as a fintech and banking conference, we’ve taken a look at our own operations to improve our environmental, social, and governance practices.

Below is a breakdown of each ESG aspect, and what we are doing at FinovateFall this year to support and promote a healthier environment.

Environmental responsibility

Reducing carbon emissions We’re reducing carbon emissions not only in the way we conduct FinovateFall, but also in how we travel to the event by carpooling and taking public transportation when possible.

Environmental sustainability content FinovateFall will host dedicated on-stage content on environmental sustainability in fintech. In addition to featuring demos from fintechs supporting sustainability, we’re hosting a keynote by Greg O’Gara, Lead Analyst, Wealth Management at Javelin Strategy & Research on Climate Change, ESG & Financial Services, What Do Wall Street & Your Customers Want?

Sustainable development

Sustainable Fintech Scholarship With our demo scholarship program, Finovate will spotlight underrepresented founders and startups tackling climate change, diversity, and financial inclusion. The program will also help us expand our demo line ups to include more voices, more perspectives, and more cutting-edge thinking within fintech.

Sustainable development goals Our aim is for FinovateFall to promote long-term sustainable development – in the way that we run the event but also in how it’s implemented in the market as a whole. We are committing to:

Using our content to support the sustainability of the fintech market

Developing close partnerships with charities, companies and associations and giving them a platform to promote their work in the field

Facilitating discussions on pertinent topics including diversity and inclusion, gender balance, sustainability trends, the impact on the environment, and more.

Governance

Operation Backpack We are supporting Operation Backpack, a Volunteers of America non-profit that provides brand new backpacks and grade-specific school supplies to children living in homeless shelters throughout the five boroughs of New York City. Please help us support this important work by making a donation. Even a small contribution will help!

Diversity and inclusion content We’re hosting a fireside chat on diversity, and one on financial inclusion. Jim Perry, Senior Strategist at Market Insights will discuss why diversity matters and Melissa Koide, CEO of FinRegLab will talk about driving purpose and profit through financial inclusion.

Startup Booster FinovateFall’s Startup Booster program offers smaller fintechs a voice in front of a large investor audience. The program is limited to fintech and tech startups who are less than five years old and have raised, at most, Seed capital. Participants will attend a 60-minute reception that will offer face time with investors, as well as a dedicated cocktail table and sign at the event.

Our driving force

Overarching all of this is our initiative called FasterForward, our parent company Informa’s program that embeds sustainability into everything we do and aims to help our customers do the same. With FasterFoward, we are striving to achieve nine specific goals:

Become carbon neutral as a business and across our products by 2025

Halve the waste generated through our products and events by 2025

Become zero waste and net zero carbon by 2030 or earlier

Embed sustainability inside 100% of our brands by2025

Help and promote the achievement of the UN’s Sustainable Development Goals through our brands

Enable one million disconnected people to access networks and knowledge by 2025

Contribute $5bn per year in value for our host cities by 2025

Contribute value of at least 1% of profit before tax to community groups by 2025

Temenos unveiled a new solution, based on Generative AI, that automatically classifies customers’ banking transactions.

The new offering will help banks offer more personalized insights and recommendations to their customers.

Temenos’ Generative AI solution is part of the company’s strategic AI roadmap. Other use cases for the technology include chatbots and guiding customer journeys.

How will financial services companies take advantage of Generative AI? One way, courtesy of a new solution from Temenos, will be to leverage the technology to automatically classify customers’ banking transactions. This functionality will make it easier for banks to offer personalized insights and recommendations to their customers.

While traditional AI and machine learning technologies have been deployed by financial services firms in a variety of contexts, generative AI and Large Language Models (LLMs) offer these companies the ability to enhance both operations and customer experiences even further. This is due to the fact that Generative AI and LLMs outperform traditional AI and machine learning approaches when it comes to understanding language, images, sound, video, and code – and then leveraging these inputs into a variety of solutions for customers.

Temenos’s new Generative AI-based offering enables banks to automatically classify and label customer transactions. The technology has a high degree of accuracy and operates in multiple languages. The automatic customer transaction capability has a number of use cases including cashflow prediction, customer attrition analysis, next best product, and more.

“We have continually invested in embedding Explainable AI and ML capabilities into our banking platform and making available all products through an easy-to-use interface or APIs,” Temenos President of Product and COO Prema Varadhan said. Varadhan referred to the new offering as part of the company’s strategic AI roadmap and underscored the value of transparency and explainability when it comes to deploying AI.

Temenos has deployed explainable AI in a wide variety of use cases ranging from wealth management, AML, credit scoring, smart money management, collection optimization, and more. However, transaction classification is the first instance of leveraging Generative AI in a Temenos product. The company said in a statement that it plans to extend the technology to chatbots and customer interfaces, as well as in guiding customer journeys and responding to customer queries.

A Finovate alum since 2013, Temenos was founded in 1993 and is headquartered in Geneva, Switzerland. The company serves 3,000 customers and its open platform enables more than 1.2 billion individuals to conduct their daily banking activities. Two-thirds of the top 1,000 banks in the world and more than 70 challenger banks in 150+ countries use Temenos’ technology. Max Chuard is CEO.

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

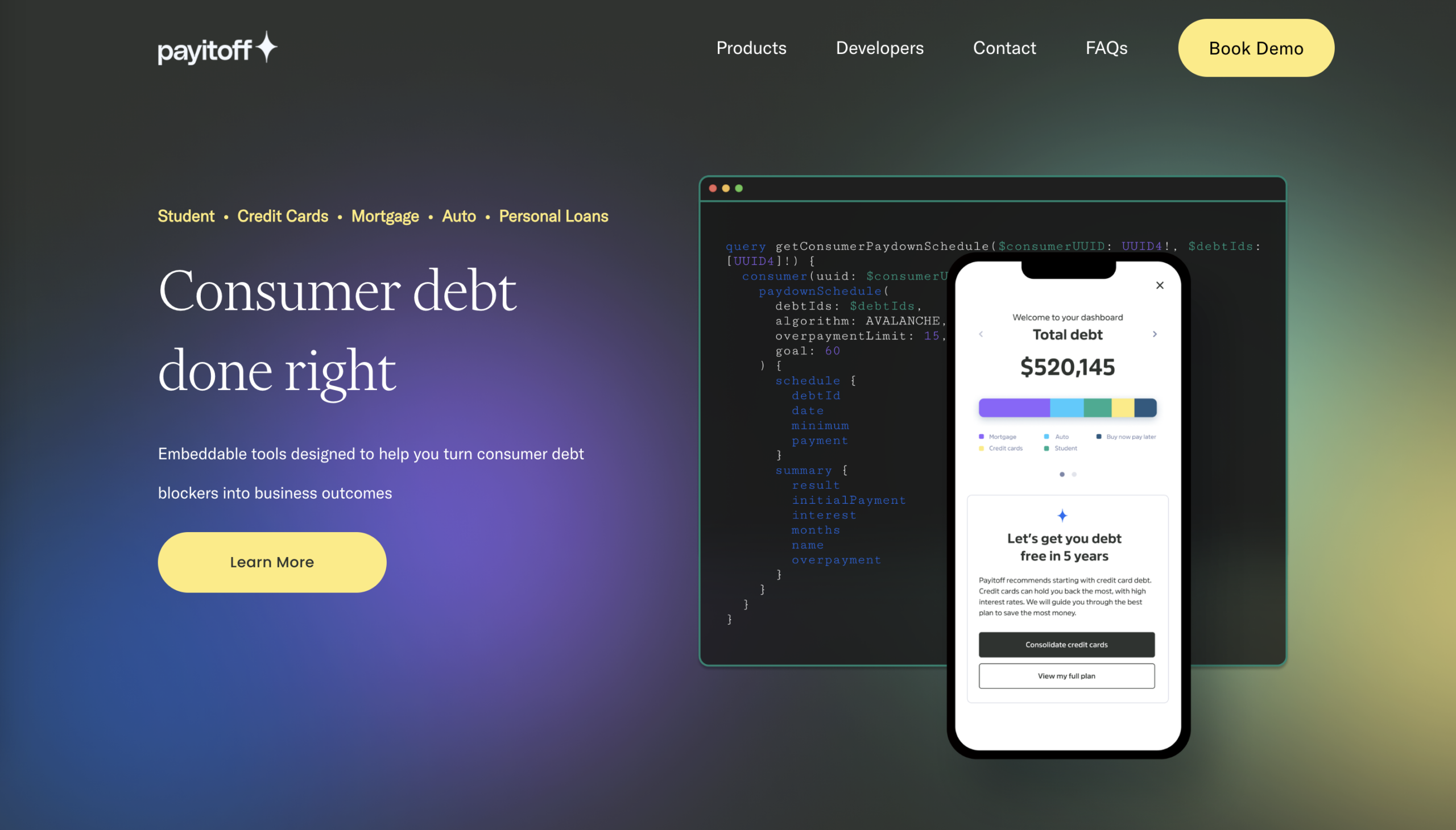

Payitoff is a leading provider of embeddable tools designed to help turn consumer debt blockers into business outcomes.

Features

Link: Connect consumer debt accounts with a phone number

Guide: Provide the best next action to improve their financial outcomes

Act: Money-saving actions taken in-app by customers

Why it’s great

This debt guidance technology achieves remarkable outcomes while maintaining an efficient use of developer resources as a no-code solution with options for embeddable and API-first implementations.

Presenter

Bobby Matson, CEO & Founder Matson turned his student loan frustration into an automated debt management system, providing clarity to millions with the institutions they trust. LinkedIn

ThetaRay raised $57 million in a round led by Portage.

The funds bring the company’s total funding to $112 million.

ThetaRay will use the funds to fuel global expansion.

Financial crime fighting fintech ThetaRayannounced today it has received $57 million. The growth round, which boosts the company’s total funding to $112 million, was led by Portage, with contributions from existing investors JVP, OurCrowd and others.

Israel-based ThetaRay will use the funds to accelerate global growth. “Guided by the adept leadership of Peter Reynolds, the resolute ThetaRay team stands ready to expand its financial technology footprint across continents – spanning North America, South America, Europe, Africa, and Asia – and venture into uncharted realms of innovation,” said ThetaRay Founder and Chairman of JVP and Chairman of ThetaRay Erel Margalit.

“Global payment infrastructure too often fails to accurately differentiate between perfectly legitimate transactions and ones from bad actors dealing with illicit funds,” said ThetaRay’s recently appointed CEO Peter Reynolds. “We’re proud to be at the forefront of the revolution to make global transactions easier, safer, and cheaper and are keenly aware of the massive vote of confidence this investment is in both our technology and our team.”

Founded in 2013, ThetaRay leverages AI to monitor 11 billion transactions valued at $15 trillion on an annual basis. The company’s AML transaction monitoring and screening solution, SONAR, helps banks and fintechs screen both cross-border and domestic payments for money laundering. When compared to rule-based systems, SONAR results in 99% fewer false positives. Among the company’s clients are ClearBank, Travelex Bank, and Santander.

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

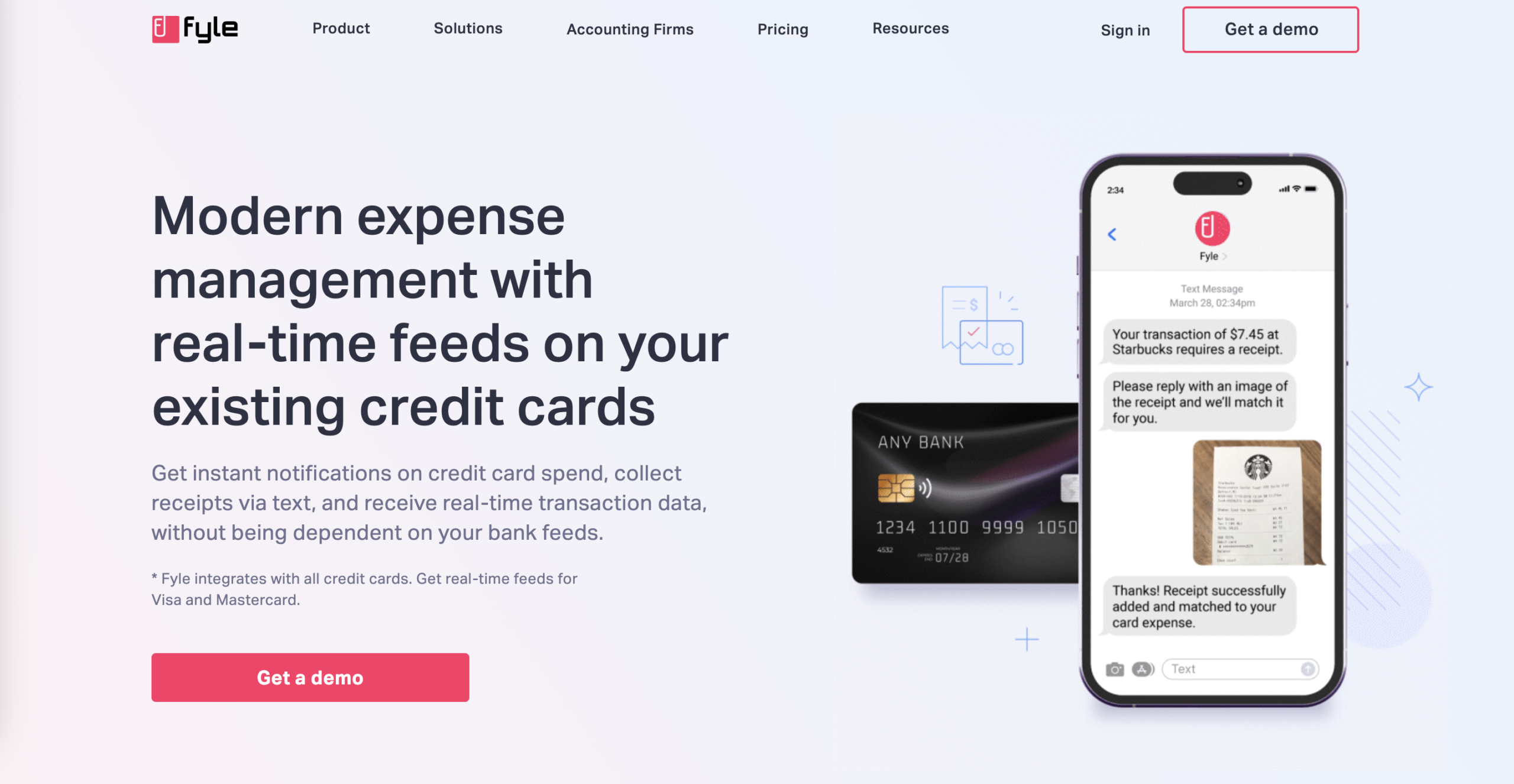

Fyle’s no-code expense management platform offers a modern fintech-like experience on bank-issued card programs.

Features

Real-time card integration with instant transaction data & notifications

Direct card enrollment (independent of banks, aggregators)

No code platform with no dependency on bank tech stacks

Why it’s great

Real-time card integration with transaction data and instant notifications via SMS.

Presenters

Yashwanth Madhusudan, Co-Founder & CEO With an extensive background in customer experience, Madhusudan has a passion for product development and solving problems that have a large scale business impact. LinkedIn

Sivaramakrishnan Narayanan, Co-Founder & CTO Narayanan has been part of two acquired startups and has authored 15 publications and 9 patents. LinkedIn

A look at the companies demoing at FinovateFall in New York on September 11 and 12. Register today and save your spot.

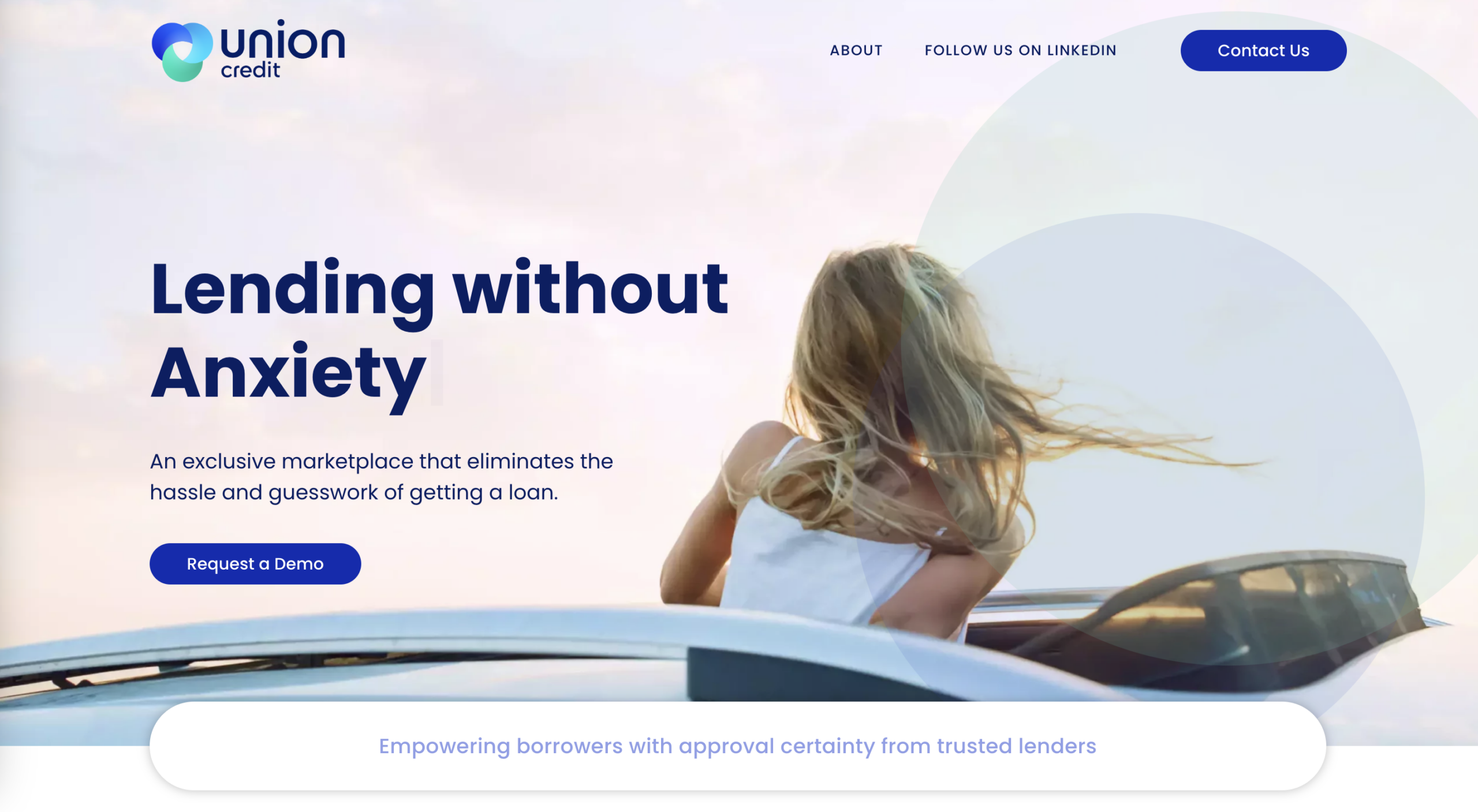

Union Credit is the first marketplace for credit unions to deliver firm credit approval and one-click loan activation to new members embedded within their daily activities.

Features

Helping credit unions promote their products to millions of credit-worthy consumers

Providing publishers/merchants with a new revenue source

Why it’s great

Union Credit will change the game for credit unions, helping them serve locally while also reaching into new markets with easy, one-click consumer lending.

Presenters

Barry Kirby, Co-Founder & CRO Prior to Union Credit, Kirby was the SVP and Managing Director of CuneXus. He has an extensive background in fintech and the credit union space. LinkedIn

Stefan Ionescu, Engineering Lead Ionescu is the engineering lead at Union Credit, driving the development of the company’s flagship product. Before that, he led the development of the innovative DecisionLender4 loan origination system at TCI.