I was packing up my hotel room after five great days in NYC putting on Finovate, when I got a call from a reporter who asked me if I’d “heard the news.” Since we’d been talking P2P lending earlier in the week, I figured his question was related to that. But I couldn’t imagine what news could compete with the launch of Loanio, the closing of Zopa (US), the delayed launch of Pertuity Direct, and the grand reopening of Lending Club. That was already a full year’s worth of major developments packed into a two-week period.

I was packing up my hotel room after five great days in NYC putting on Finovate, when I got a call from a reporter who asked me if I’d “heard the news.” Since we’d been talking P2P lending earlier in the week, I figured his question was related to that. But I couldn’t imagine what news could compete with the launch of Loanio, the closing of Zopa (US), the delayed launch of Pertuity Direct, and the grand reopening of Lending Club. That was already a full year’s worth of major developments packed into a two-week period.

So I about fell off the bed when he told me Prosper had closed off new lending until the completion of its SEC registration process, entering the same regulatory twilight zone from which Lending Club had just emerged the previous day. And this was only 14 hours after Chris Larsen had been quoted in an upbeat Prosper company blog entry about the role of his company during the credit crunch (note 1):

“At a time when every sector in the economy seems to be under pressure and shrinking, the growth Prosper has experienced is very respectable.”

Impact on Loanio

Because I’d just spent an hour with Loanio founder Michael Solomon the day before at our Finovate conference, I immediately wondered if he might be facing the same registration hurdle. But I reached him a few minutes ago via email and he’s thinking this probably benefits his new marketplace since lenders are frozen out of Prosper. He also doesn’t expect to enter into a similar registration process in the foreseeable future.

Here’s his full statement:

“…from the perspective of (Prosper) going silent, it is actually great for us as I think we will quickly gain lots of lenders and hopefully we can wow them into sticking around. From a regulatory standpoint, we believe that at some point we will seek to introduce a secondary market platform, but we will focus the greater part of the next 12 months on building our platform and seeking out a national bank partner to cover the rest of the U.S. Our plans for a secondary market are too far ahead for me to contemplate at this time.”

Thoughts

Regulators certainly have a right to require transparency in the marketplace and protection for consumers. But Prosper, with an open API of its transactions, balances and even repayment behavior, and which uses a completely market-driven, open-bidding process to set rates and select loans to fund, is about as open a business as you ever will see, especially in financial services.

For the sake of the nascent industry, I hope the registration is put on a fast track and Prosper is back in the game faster than the six months Lending Club waited. At this point, an alternative credit supply, albeit only $100+ million per year right now (note 2), sourced directly from willing individual investors and not from capital-constrained financial institutions, seems like something we should encourage.

Ultimately, Lending Club and now Prosper should benefit from improved liquidity that the secondary market allows. Since Prosper is not allowed to comment on the move, we can only speculate on what happened. But the timing of all this seems a bitter irony. Wasn’t a breakdown in the secondary markets a big part of what put us in such a bind now?

According to its blog, Prosper will continue to make loans “through alternative sources (of funds)” (note 3). So perhaps the impact to the Prosper marketplace will be small. Especially if they are back in full swing by year-end or early 2009.

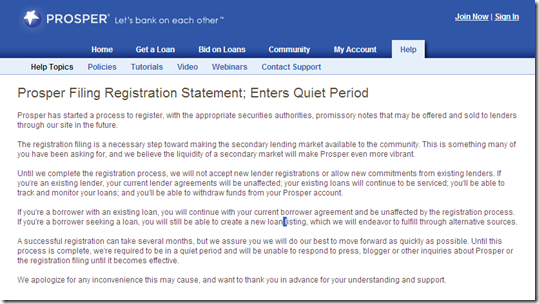

Notice on Prosper’s website announcing quiet period (isn’t that an oxymoron?) 16 Oct. 2008

Notes:

1. See today’s NY Times article for more info on this week’s developments. Don’t miss the picture of Lending Club CEO Renaud Laplanche standing outside the Finovate 2008 demo hall.

2. For more info on the market, see our Online Banking Report on Person-to-Person Lending.

3. Presumably, to keep the loans flowing, Prosper can tap its own funds as well as those of institutional investors or other professional investors. We’ll know soon, thanks to its open API.

In the early commercial Web era (1995 to 1998), five financial startups inspired me in terms of their innovative products and services:

In the early commercial Web era (1995 to 1998), five financial startups inspired me in terms of their innovative products and services: