Continuing our series on wealth tech (check out our first post highlighting top trends), I wanted to step back and look at the industry as a whole. While multiple published analyses about robo advisors can be found, little is published regarding the broader wealth tech industry.

What is wealth tech?

Simply put, wealth tech is a segment of financial technology that focuses on enhancing wealth management and investing. That means that while robo advisors are a large—and quite popular—piece of the wealth-tech puzzle, other pieces merit discussion, too.

What does wealth tech encompass? Exclude?

Technology from traditional wealth management firms, alternative investment solutions from non-bank players, and tools to support financial advisors—all fall under wealth tech. Ancillary technology, such as PFM, are not considered part of wealth tech.

A robo advisor by any other name

While the term robo advisor is commonly used (a Google search produces 2.2 million results), not all automated management and advisory companies appreciate the name. For example, Personal Capital (FS14, FDSV16) CEO Bill Harris doesn’t classify his company as a robo advisor, which he views as a wholly automated investment tool. Instead, he strives to balance high tech with high touch. In an interview with WealthManagement.com Harris said, “We do have technology that is helping to automate and scale what we do, but in addition to that technology, just as important, are the individual advisers. Ultimately, the job of matching a household with the optimal portfolio is a more complicated thing than plugging information into a series of algorithms.” iQuantifi (FF14) is on the other end of the spectrum. In his demo at FinovateFall 2014, iQuantifi founder and CEO Tom White said, “We’re the only true robo advisor, and we’re not ashamed to call ourselves a robo advisor.”

Industry movement

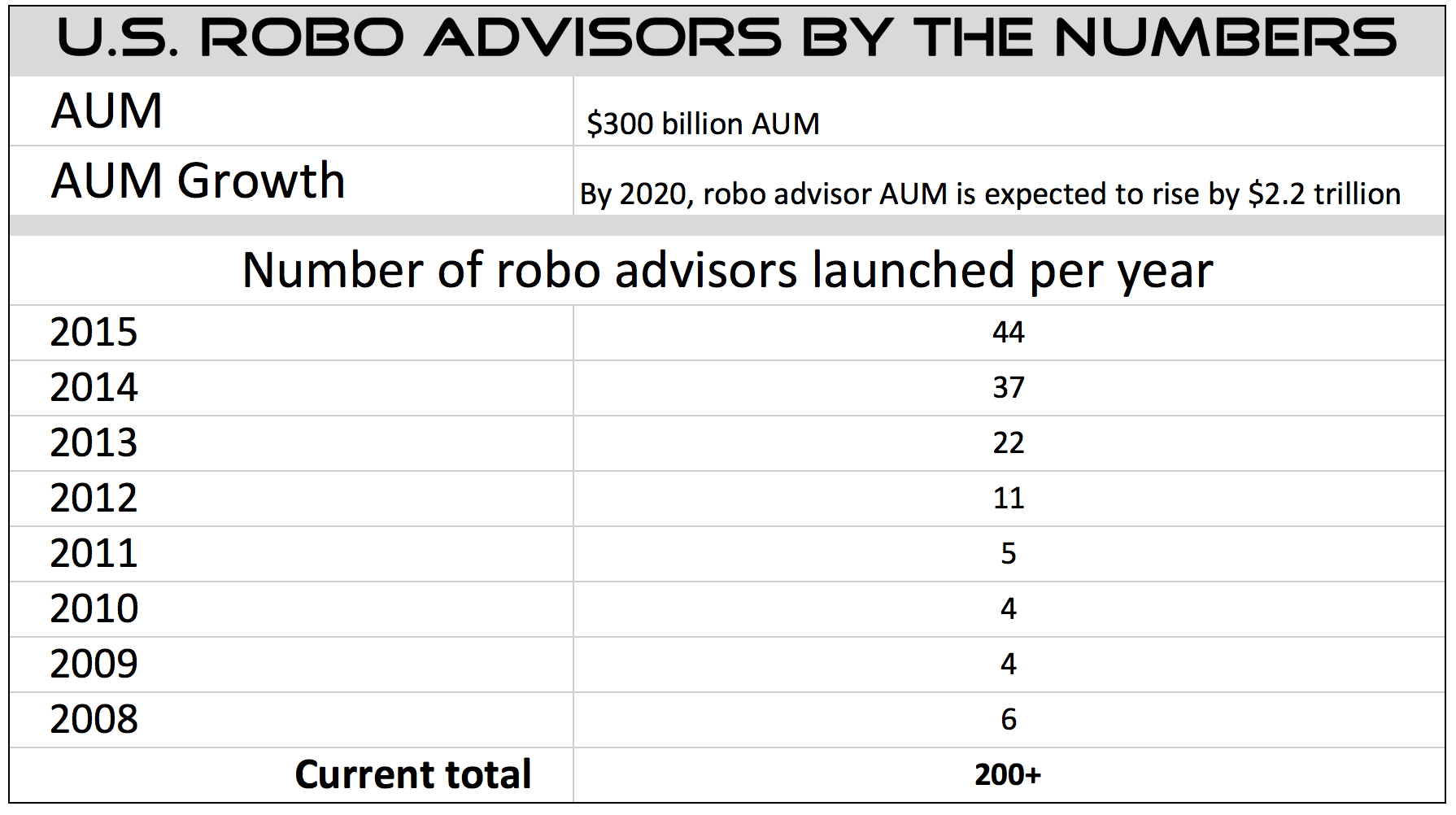

Since the advent of robo advisors in 2008, we’ve seen a lot of growth in the U.S. robo advisory market. Take a look:

Assets under management are predicted to climb six-fold in the next three years, to $2.2 trillion. With the number of robo advisor launches increasing by an average of 43% YOY since 2008, it’s likely we’ll see a decrease in the number of robo advisor launches in the U.S., combined with an increase in M&A (mergers and acquisitions) activity to further consolidate the industry.

Next week, I’ll continue the wealth tech industry analysis by taking a look at divisions in the industry and reviewing some key players.

Sources:

Financial Review

Logging on to the Future of Financial Advice

by James Frost

A.T. Kearney

Hype vs. Reality: The Coming Waves of “Robo” Adoption

by Teresa Epperson, Bob Hedges, Uday Singh, and Monica Gabel