What happens when you’re facilitating the trade of a product that is experiencing extreme hockey stick growth? You expand your team and operations as quickly as possible.

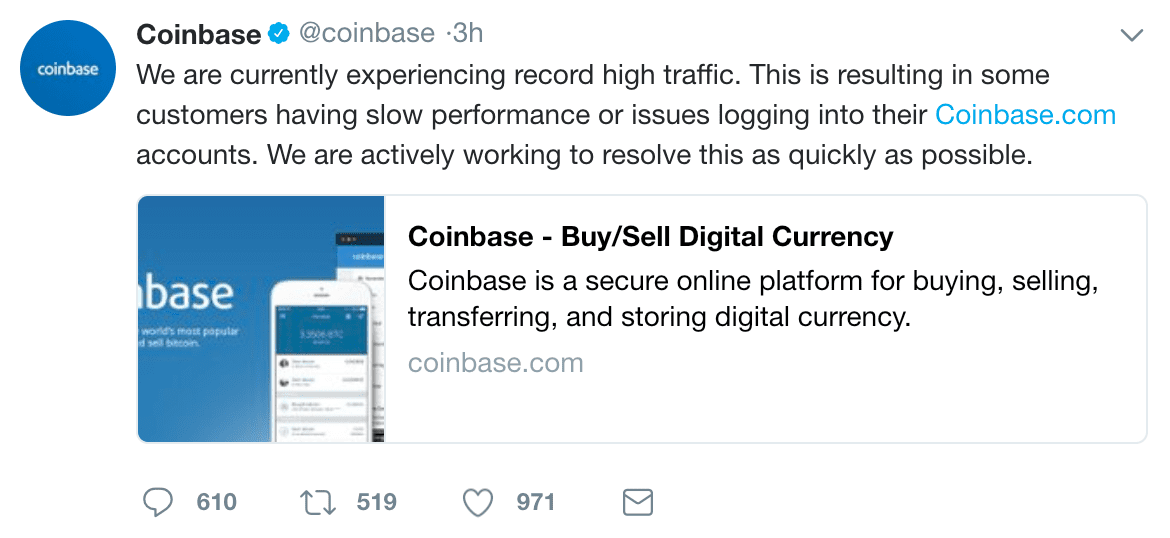

This is what Coinbase, an exchange platform for bitcoin, ethereum, and litecoin, is experiencing. The California-based company will have plenty of war stories to tell once this season mellows out. After bitcoin blew past $16,000 earlier today*, the company tweeted:

The New York Times, in its piece Coinbase: the Heart of Bitcoin Frenzy, explained Coinbase’s popularity over other cryptocurrency trading platforms. Author Nathaniel Popper said, “Coinbase has been the dominant place that ordinary Americans go to buy and sell virtual currency. No company had made it simpler to sign up, link a bank account or debit card, and begin buying Bitcoin.”

Because of this growth, Coinbase now has more customers than E-Trade and Charles Schwab, having increased by 7.8 million accounts since January of this year. However, Coinbase CEO Brian Armstrong sees past the hype into a more stable future for cryptocurrency. He told the New York Times that bitcoin is “probably a little bit too focused on the price or people trying to make money.” He added, “The thing I’m passionate about with digital currency is the world having an open financial system.”

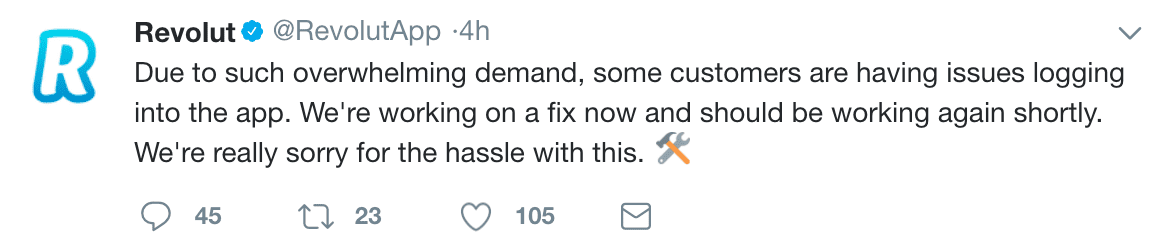

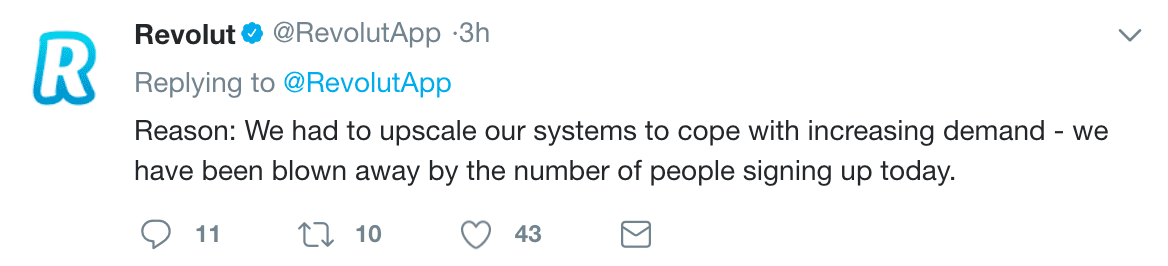

Coinbase isn’t the only one experiencing growing pains. Global banking company Revolut, which launched a cryptocurrency trading feature today, sent out this series of Tweets this morning:

Founded in 2012, Coinbase demoed Instant Exchange at FinovateSpring 2014. In August, the company became a fintech unicorn after it closed a $100 million round of Series D funding. At that point, Pitchbook estimated Coinbase’s value to be $1.6 billion.

*Note: Earlier today Bitcoin’s value spiked over $17,300 but at press time sits at $17,099.