While everyone else was playing Pokemon Go last month, I was doing something more appropriate for someone my age, crowdfunding a house flip in La Jolla. Amazingly, I was able to view the property and public records (Google Streetview, Bing, Zillow, Redfin, Trulia); check out the construction-cost estimates; review the revised floor plan; and check out the actual appraisal for the as-built value against four comps in detail, all from the comfort of my home.

Ever since a brief stint in the early 1990s at a mortgage bank, I’ve known there was great demand, and tidy profits, in financing major home rehabs. I never thought I’d have the guts to flip a house myself, and I still don’t, but I can do the next best thing: loan money to real estate rehabbers through crowdfunding sites such as Realty Mogul, Patch of Land, RealtyShares and the like.

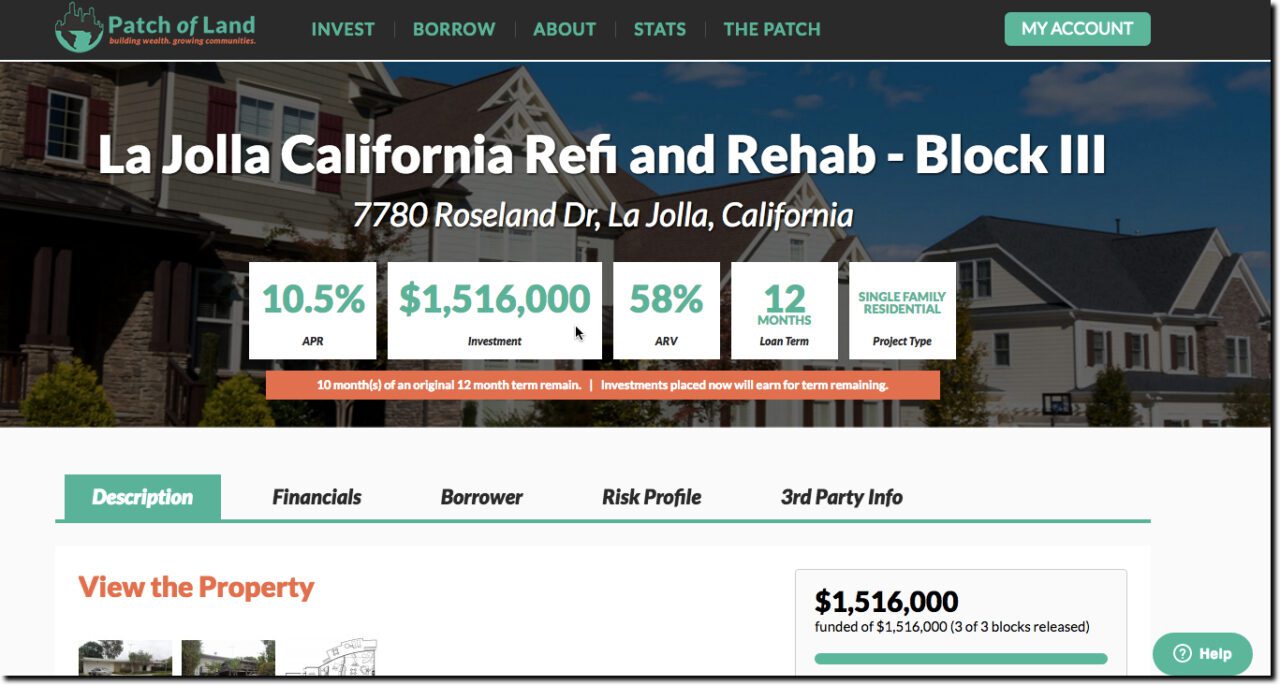

For my first try, I chose Patch of Land because they are a Finovate alum (see note 1), but mostly because their email showcasing a new rehab investment opportunity in La Jolla, California (where I honeymooned) caught my attention (see investment page above). The developer bought a 3-bedroom, 3-bath house in May for $1.3 million and is putting $500,000 into a major remodel, creating a 4-bedroom, 2-bath (which the appraiser objected to by the way). The work has already begun, but Patch of Land was still looking to fund the final 10% of the loan. The startup prefunds the projects with its own money, then resells them to investors. This particular house will pay 10.5% interest for the 11 months remaining on the original 1-year term; however, it is likely to be paid off early if all goes well and the house is sold before the end of the 12-month period.

The real estate crowdfunding industry is already bigger than I expected. I haven’t found reliable stats for 2015, but the market was estimated at $1 billion in funding in 2014. Patch of Land has done $150 million since inception, and Realty Mogul, more than $200 million. According to (an undated post) in the Real-Estate Crowdfunding Review, more than 100 such sites exist. They rated eight as all-stars, including two Finovate alums: Realty Mogul ($200 million in cumulative originations) and Patch of Land ($100 million in originations as of March 2016), along with Acquire Real Estate, LendingHome, Peer Street ($75 million in originations), Real Crowd, Realty Shares ($130 million through Feb 2016) and Roofstock.

Bottom line: If you are looking for alternative investments to recommend to clients, consider working with a major crowdfunder to white-label or co-brand the service.

——-

Note: If anyone wants to talk real estate crowdfunding, or anything else, at Finovate NYC in two weeks, drop me a line ([email protected]).