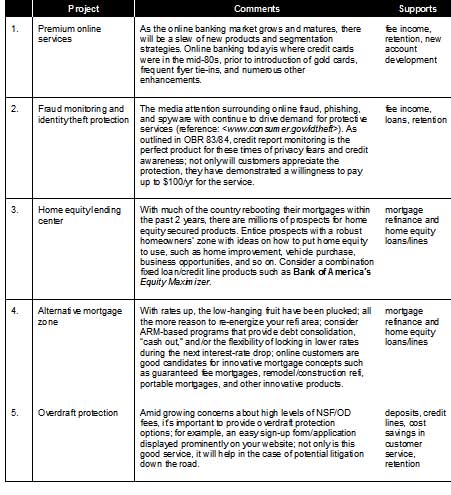

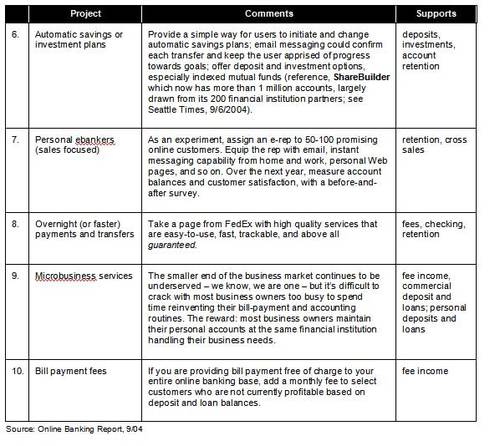

Following are our ten most-promising tactics for generating incremental revenues during calendar year 2005.

Finovate is part of the Informa Connect Division of Informa PLC

This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Following are our ten most-promising tactics for generating incremental revenues during calendar year 2005.

A crucial part of the planning process is reaching deeply to find the

best ideas. Many companies already have a process in place, but if you are

looking for inspiration, consider the following six-step approach.

Six Steps to the Big Idea

1. Do Your Homework (Immersion): Study the situation, visit

competitors, read new research, talk to customers, interview employees,

attend a conference, poll your customer base, and so on.

2. Optimize the Environment: Clear away constraints to

thinking, go off site, stockpile the food and coffee, play music; do

whatever it takes to let your thoughts flow freely.

3. Rattle the Brain: Perform “thinking exercises” to

limber up the brain before tackling your specific problem (see our ideas,

left, or Jump Start Your Brain by Doug Hall for 37 more).

4. Generate Idea Nuggets (free form): Think of every

possible solution to the problem, regardless of how crazy; write them down

without judgments or justifications.

5. Assemble Idea Nuggets Into Strategies and Tactics:

Transcribe each nugget on a

3×5 card and arrange the cards into bigger concepts and ideas.

6. Be Bold: Don’t immediately dismiss strategies that seem

too big for your budget; winners

could be shopped to strategic investors or other financial institutions for

additional funding.

Source: Adapted from Jump Start Your Brain by Doug Hall, Warner

Books, 1995. A new version, Jump Start Your Business Brain was

published in Sept. 2001. Both are available in paperback from Amazon for

about $12 each.

Do Your Homework

To see potential opportunities in a new light, look beyond your normal

circle of peers, subordinates, and other industry sources.

| 1 |

Observe First-Hand: Find out how consumers really use online

financial services and observe how the services could be improved. For

example:

| 2 |

Attend an industry conference: Away from the daily grind,

surrounded by the latest technology and bombarded by new ideas: a perfect

prescription for breakthrough thinking. The two biggest U.S. online banking

conferences take place in the fall, the American Banker’s just-completed

Financial Services Technology Forum and BAI’s Retail Delivery

which will be held next month in Las Vegas.

| 3 |

Dive in to third-party research: Grab a few research reports, head

to a quiet table in your favorite coffee shop, and turn off your Blackberry.

Now, really read the whole report, skipping the executive summary

until the very end. Take notes and highlight pertinent pages. At the end of

the day, create your own executive summary with a list of possible action

ideas and questions to share with your team.

| 4 |

Commission your own research: Research culled from your own

customers and in-market prospects is infinitely more believable than

national studies. If research budgets are nil, you can still post a short

survey on your Web for next to nothing and have results tomorrow. The data

won’t be applicable to your entire customer base, but it might provide a

number of good ideas and insights.

Or if you’d prefer to take a quick reading of consumer sentiment without tipping

your hand to the competition, consider tapping into the preassembled panels of

Web research companies. At InsightExpress http://www.insightexpress.com/

it’s possible to ask 200 consumers what they think of your idea for an

out-of-pocket expense of about $1,500. Questionnaires are easily

composed using online templates, and you’ll have results back within hours. All

results are stored online where you can run your own reports and cross

tabs.

If a picture is worth a thousand words, what’s a Flash demo worth? Even

though we go to great lengths to describe innovative new services, it doesn’t

really sink in until you’ve personally sampled it. To loosen the cobwebs, we

recommend a hands-on session running an innovative online service through its

paces. If you need ideas, see Table 2, below. These are the innovative services

we’ve selected each of the past six years. You can find more information about

each by consulting the appropriate OBR back issue.

Table 2

OBR Thinking Exercises

1999 through 2004

|

Year |

Subject |

Exercise |

| 2004 | Integrated account aggregation | Use OneView from Everbank |

| 2003 | Premium online banking | Review 1st Source Bank of Indiana’s segmented online banking offering |

| 2002 | Account alerts | Use fyiAlerts from Charter One |

| 2001 | Savings | Open a savings account and setup automatic transfers at ING Direct |

| 2000 | P2P payments | Pay for an eBay purchase with PayPal (now owned by eBay) |

| 1999 | Account aggregation (stand alone) | Sign up and use account aggregation at VerticalOne (now Yodlee) |

Source: Online Banking Report, 9/04

2004 Exercise:

Integrated Account Aggregation

Direct banking pioneer Everbank (Jacksonville, FL; $2.7 billion) has

raised the bar again with its new online banking platform (screenshot left).

There is

much to be learned from its implementation, the culmination of three years of

effort. We’ll be reporting on it in depth in an upcoming report. But don’t wait

for us to tell you about it. Get out a pad of paper, study its website, and take

notes. If you really want to see it in action, you’ll need $1500 to open an

account, and you’ll need to wait a week for your paperwork to be processed.

Either way, pay special attention to the degree of integration occurring with

the account aggregation technology.

Time Needed:

– 60 to 90 minutes

Material Needed:

– paper for note taking

– (optional) $1500 to fund an initial deposit

– (optional) username/password for at least one outside

account to aggregate at Everbank

Instructions:

1. Visit the bank

www.everbank.com

2. Navigate to online banking demo and follow the instructions.

Optional: Open an actual account ($1500 needed). Note how Everbank’s account

opening process works compared to yours; jot down ideas for improvement.

3. Observe how the bank displays its online banking options. Pay

special attention to how account aggregation plays a role throughout the

service.

4. Finally, look closely at the boxed content on the right. Note the

features and functionality and think about what you would put in a similar box

within your online banking application.

Every year it’s a battle to win approval for your business

plans. This process, though far from perfect, is a necessary evil to ensure

that only the most promising plans are funded.

Online banking, which in the U.S. generates little direct

revenue, often requires creative spreadsheeting to show a positive

NPV. Following are some of the positives to incorporate into a winning

business case.

Stay competitive: improving account retention and

increasing sales

Improve sales by differentiating your products and

services with online functionality

Increase cross sales, especially credit/loan

products

Increase online banking and bill payment

transaction fees

Create a new stream of monthly and/or annual

service fees with a premium service option

Use marketing dollars more effectively through

targeted online promotions

Reduce costs through self-service

Improve customer satisfaction, retention, and

cross sales

Allocating scarce budget dollars

If you are looking for the biggest bang for your buck, look

to online lending and small- and micro-business initiatives. According to

Celent’s study across 1.5 million Digital Insight users (in 2001),

online lending generates four times the combined value (NPV) of banking/bill

pay. Business services were even more valuable, resulting in returns of

nearly six times that of banking/bill pay.

Everbank made a sizable investment in a new online

banking platform, a highly customized mix of Metavante and Teknowledge

software. Previously, the bank used the S1 online banking platform.

NPV from various online banking products

|

|

$ Return (NPV)1 |

||

|

Product |

5-Yr Total |

Per Cust2 |

Index |

|

Banking, statement info. |

$6,000 |

$0.12 |

1x |

|

Bill pay |

$17,000 |

$0.33 |

3x |

|

Lending |

$83,000 |

$1.65 |

14x |

|

Small business |

$123,000 |

$2.45 |

20x |

|

Total |

$228,000 |

$4.56 |

38x |

|

Combinations |

|

|

|

|

Banking and bill pay |

$23,000 |

$0.45 |

4x |

|

All except small business (lending, banking, bill |

$105,000 |

$2.10 |

18x |

Source: Celent, 10/01 For a better understanding, read

Celent’s Customer Retention and Cost Savings Drive Online Banking ROI,

Oct. 17, 2001

(1) NPV over 5 years at a 50,000-customer bank; includes direct revenues,

cost savings, and retention. (2) Per-customer figures are across all

customers, on- and off-line, consumer and small business.

As we discussed last month , there’s a real void in the marketplace when it

comes to premium online banking services. In today’s retail environment,

where you can choose from hundreds of varieties of every product on the

shelf, it’s shocking that Bank of America provides just a single flavor of

online banking to its 11+ million subscribers. Granted, users choose which

features to use, so the service isn’t truly identical for all.

But surprisingly, everyone still pays a single price: $0. For Bank of

America, that price point has been an important and highly visible component

of its strategic branding message. However, we view 100%-free online banking

as a temporary aberration. U.S. banks have had their hands full during the

past few years complying with new regulatory initiatives and fighting

fraudsters from around the globe.

And it’s a relatively recent phenomenon that online banking penetration

has surpassed 20% at many banks. Below that point, there aren’t enough

customers to make a segmented offering profitable. So even though it will

require extensive buyer education, we believe that by this time next year,

at least one, and possible two or three, top-10 U.S. banks will offer

premium online banking options.

The pioneer in this area is Online Resources, which began offering

MoneyHQ, a premium online banking option, late last year. Early

results are mixed. While Online Resources admits that client adoption has

been slower than expected, it is pleased with consumer adoption, which

stands at 9% of bill pay customers across the 45 clients who’ve been live

for at least four months. In total (as of Sep. 29, 2004), 120 clients are

signed, with 90 operational, representing 33% and 25% respectively of

eligible clients.

Strategically, we have no doubt that MoneyHQ is the right

direction, and the 9% initial adoption rate is encouraging. However, it’s

difficult for ORCC’s community bank and credit union clientele to

successfully educate the market on the benefits of premium online banking.

It may take the multi-million dollar advertising budgets of the big players

to really jump-start the service. We should know a lot more as 2005 unfolds.

Jim Bruene, Editor & Founder

We just sent our latest report, “Pricing: The Fee vs. Free Controversy” to the printer. It should arrive in your mail in a week to 10 days.

In the report we look at the widespread practice of offering of online bill payment free of charge. You can read the report for our detailed conclusions, but suffice it to say, we are not wild about this trend. Online banking and bill payment provides significant value. And without a tangible revenue stream, it’s difficult to make the appropriate investments in the channel. We think bank customers will actually be better off in the long run if they shoulder at least a portion of the extra costs of a robust online banking service.

Free bill payment is particularly vexing. Here’s a service that runs circles around the paper equivalent. Users can save time, save money (postage, late fees, and check printing fees), can improve bill tracking and budgeting, and make their financial life easier. And, if the electronic payment doesn’t post at the biller on time, the bank and/or processor will go to bat for them to resolve the problem. Try doing that with a paper check that’s “lost in the mail.”

So why do banks insist on providing this beneficial and costly service free of charge? They are doing it for the “relationship” value. No doubt users love getting something for nothing. And we won’t dispute the correlation between bill pay users and higher household profitability. But so what. You can correlate higher profits with any service designed for a well-heeled audience.

The bigger question is this: Is free bill payment, costing $50 to $100 per customer per year, the best way to gain more loans and deposits from your best customers? It may be, but there may also be less expensive ways to achieve similar results, such as lifetime transaction archives or more account security options.

It’s a tough call.

If you’d like to learn more about the future of online bill payment, check out the Online Banking & Bill Pay Forecast: Current, future and historical usage: 1994 to 2016 from our sister publication, The Online Banking Report.

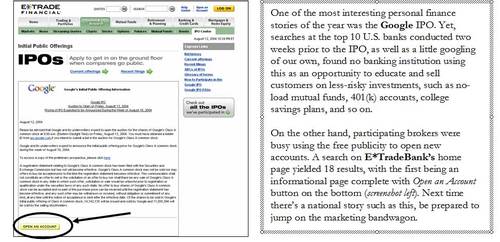

AmSouth Bank has posted a new "special offer" on its home page. The bank’s "Click to Switch" program promises, "The fast online way to tell your bank it’s over."

Clicking on the graphic leads to a page with some advice for switching checking accounts. It’s the usual laundry list of advice, none of which is really helped by the online connection. There is one useful link for changing the direct deposit of social security benefits. Though, that is likely to be of little use to most online users contemplating a switch to AmSouth Bank.

We like what AmSouth is doing, we just wish there was more meat in the offer.

By now you’ve probably dealt with the repercussions from the June 14 MSNBC

report by Bob Sullivan entitled, Survey: 2 million bank accounts robbed,

followed by the subhead, Criminals taking advantage of online banking,

Gartner says. A consumer (or senior banking manager) reading the article

would likely come away believing that two million U.S. consumers lost money from

their checking accounts due to online banking. 1

In fact, here is what Gartner actually said in

its report2:

Illegal access to checking accounts is the fastest-growing type of

consumer fraud, and may be proliferating through online channels.

(emphasis mine)

The report goes on to say that most consumers do not know how their checking

accounts were robbed: Only 17% believed their info was stolen off the Internet;

another 10% reported wallets stolen; and only 5% recalled giving up personal

info to phishers.

Gartner also said that 70% of the online consumers reporting losses also

report that they banked or paid bills online, “which exposes their (codes) to

the Internet.” However, what Gartner failed to point out was nearly 70% of

online consumers that weren’t robbed also bank or pay bills online, so

it’s a meaningless correlation.

Finally, consider the research methodology. It looks staggering in the

headlines to say that two million people were robbed. But my

back-of-the-envelope calculations indicate this huge number was extrapolated

from fewer than 75 respondents reporting a recent unauthorized checking account

withdrawal (from Gartner’s survey of 5,000 online adults). Some fairly large

errors can occur generalizing a small sample size to the entire population. I’m

not saying it’s wrong, but one should be wary.

As bad as the MSNBC article looks for the online banking industry, the NBC

Nightly News with Tom Brokaw got even more carried away. They took an even

bigger number, 4.5 million, which Gartner said is the number of people who have

ever had an unauthorized checking account withdrawal, and mistakenly said that

all those people were robbed via online banking. Here’s MSNBC’s synopsis of the

TV feature posted online next to the Sullivan article (see inset):

An estimated 4.5 million Americans have had money stolen from their

Internet bank accounts. NBC’s Bob Hager reports.

This is a great example of what happens when a respectable piece of research

is taken out of context. It begins to have a life of its own as other news media

echo the original broadcast.

While many subsequent news articles echoed the conclusions of the original

MSNBC piece, some dug deeper. For example, NBC affiliate WEEK-TV quoted

Peoples Bank (Bloomington/Normal, IL) CEO Ed Vogelsinger as saying that

despite having 20% of their base using online banking, so far no one has

reported any Internet banking fraud. Way to go, Ed.

We urge our readers to take appropriate steps through their PR channels to

set the record straight. At a minimum, be prepared to rebut the MSNBC numbers if

approached by the media, and feel free to send any reporter our way to

corroborate your position.

Contact: Jim Bruene, Editor, Online Banking Report, 206-517-5021 or email

[email protected] .

1 Reference: <

http://www.msnbc.msn.com/ /id/5184077/>

2 Banks Must Act

Urgently to Stop Account Hijackers, by Avivah Litan, Gartner, June 14,

2004

Eliminating bill payment fees is the simplest way to make customers happy.

However, there may be less expensive alternatives that position you better

for the long term.

First, let’s look at how consumers choose a bill payment service

provider. It’s not so much about the price. What they want is to have their

bills paid in a timely manner with the least amount of effort and maximum

amount of control. Other factors play a role as well:

Table 9, right, lists 43 attributes related to the consumer’s bill

payment purchase decision.

So, rather than offering it fee-free, perhaps you could improve your

value-proposition in other ways to provide a similar adoption lift without

losing the fee income altogether. Following are five alternative

approaches.

1. Conditional (on another purchase)

· Free if you do add something that improves revenues, such as

adding an account

· Free if you do something that lowers costs such as switch to

estatements*

· Free with minimum balance levels

· Free as part of an overall relationship account

2. Crippled (reduced features and benefits)

· Free with usage limited to electronic merchants only

· Free with reduced or pay-per-incident customer service

· Free with reduced functionality

· Free with reduced usage

*Two top-50 banks are using this approach,

First Tennessee and

National Commerce Financial

Table 9

Factors Used by Consumers When Selecting a Bill Payment Provider

Source: Online Banking Report, 8/04

3. Substitute other lower-cost FREE services

· Free paper check and statement archives

· Free account aggregation with online bill manager (see

www.LowerMyBills.com

)

· Free 24/7 customer service

· Free interbank transfers

· Free credit report information

· Free account alerts

· Free companion air fare or other non-banking incentive

4. Provide overall relationship incentives

· Higher rates or lower fees on checking or other deposit accounts

· Lower rates and/or higher lines of credit

· Higher service levels and better guarantees

5. FREE as part of plain-vanilla, reduced-benefit online banking

package

· Actively upsell advanced fee-based packages with numerous

additional features and benefits (see Table 10 below)

· Limit the life of the plain-vanilla package; enact forced

conversion after several years into fee-based product

Table 10

Bill Payment Product Differentiation

Source: Online Banking Report, 8/04

The real question: Does subsidizing bill payment improve profits more than

spending that money in other ways, e.g., better service, better branches, better

website, and so on? Only individual financial institutions can answer the

question, factoring all the alternative uses of capital. However, we caution

against blindly jumping on the fee-less bandwagon. Think of free bill pay as

just one more strategic choice, not a mandate from the marketplace.

The simplest approach is a breakeven analysis

(see Table 8, right). In other words, will my current bill pay base, and

the new customers attracted to a free offering, bring in enough extra business

to cover the $50 to $75 annual subsidy?1

On the deposit side, the case is pretty weak: to offset a $60 annual subsidy,

you’d need incremental balances of $3,000 at a 2% spread or $6,000 at a 1%

spread. On the loan side, the numbers work better. At a 4% spread, you only need

an extra $1,500 to break even. But is subsidized bill payment really the most

cost effective way to increase loan balances? If so, you should probably make a

more direct tie-in, such as waving bill pay fees for taking a new credit line (see

“Bill Pay Credit Lines,” OBR 81

Mini Business Case

A more precise measure of the balance levels needed to cover bill payment fee

waivers looks at the total cost of bill pay and the number of incremental

customers attracted. For this calculation, use the following assumptions:

· $90 annual cost for each bill pay customer, including internal

servicing costs and outsourced processing

· 50% of bill pay customers would pay $5/mo

· 50% are incremental, drawn by the free offer

· 10,000 total users

So the total incremental cost is:

· New users: 5,000 x $90 = $450,000

· Forgone fees from existing users:

5,000 x $60 = $300,000

· Total incremental costs: $750,000

Table 8

Breakeven Incremental Balances

|

|

Incremental Balances Needed to Breakeven |

|

|

Spread |

Total |

Per Bill Pay Customer |

|

1% |

$75 million |

$7,500 |

|

1.5% |

$50 million |

$5,000 |

|

2% |

$38 million |

$3,750 |

|

2.5% |

$30 million |

$3,000 |

|

3% |

$25 million |

$2,500 |

|

4% |

$19 million |

$1,875 |

|

5% |

$15 million |

$1,500 |

|

6% |

$13 million |

$1,250 |

|

7% |

$11 million |

$1,100 |

Source: Online Banking Report, 8/04

Results

Even with a modest base of 5,000 bill pay customers currently paying $5/mo

for the service, you may need to attract $25 million or more in incremental

balances to make back the $750,000 in incremental costs. Even if you think

that’s possible, is that the best return on the $750,000 “investment.” Would

that money provide a better return if spent on service upgrades, marketing, or

employee education?

When deciding whether you can bring in enough offsetting balances, keep in

mind the demographic trend is moving in the wrong direction. Bank of America may

have been able to improve overall profit 30% after costs; however, that was

against an affluent, early adopter crowd. Going forward into the mass market,

will the same profit lift be seen in the 2005 to 2008 period? We doubt it. The

newest wave of users is less affluent overall, so it will be harder for them to

bring in the balances needed to offset the $50 to $100 subsidy.

1 Assumes total out-of-pocket and internal costs of bill payment

are $6 to 8/mo.