Banks are facing an increased number of competitors these days. Not only are traditional banks vying for customer deposits, but fintechs and challenger banks want part of their funds, as well.

The average U.S. savings rate is just 0.09% APY, so any amount banks can offer beyond that is a differentiator. However, some banks have gone all out and are offering more than 2% interest. The highest APY we saw totaled a whopping 6.17%.

Here are the 8 financial institutions (listed in alphabetical order) we found that are offering accounts currently paying more than 2% interest:

BrioDirect

2.1% APY with a minimum balance of $25

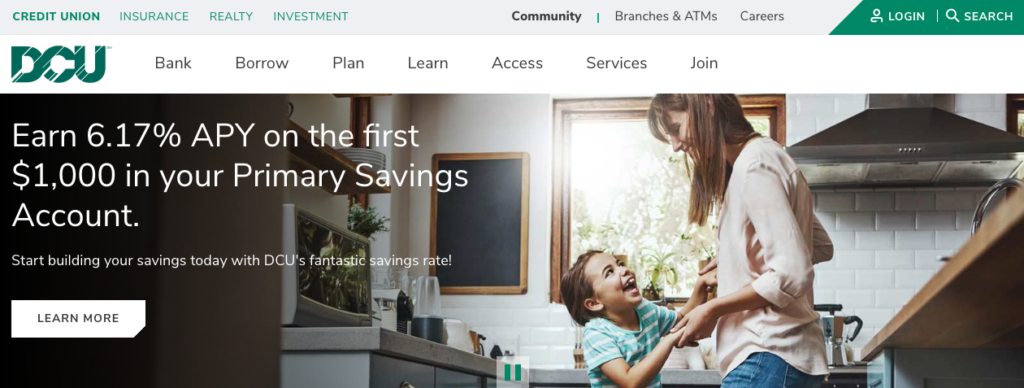

Digital Federal Credit Union

6.17% APY on first $1,000 with a minimum balance of $5

Elements Financial

New accountholders can earn 2.1% APY for one year on a minimum of $2,500 that has been transferred from another financial institution.

Fitness Bank

Members earn 2.20% APY on a minimum balance of $100 if they walk 12,500 steps or more per day (or 10,000 steps per day for those age 65 or older) as calculated on their fitness tracker.

GreenDot

Users earn 3% APY, which is paid on a maximum of $10,000 and is held in a separate account that the consumer is unable to access until the account anniversary. The high yield savings account must be opened in tandem with Green Dot’s Unlimited Cash Back account, which pays customers a 3% cash-back bonus on all online and in-app purchases. The account charges a $7.95 monthly fee if a consumer’s purchases (excluding mobile bill payments, ATM withdrawals, and ACH transactions) are less than $1,000.

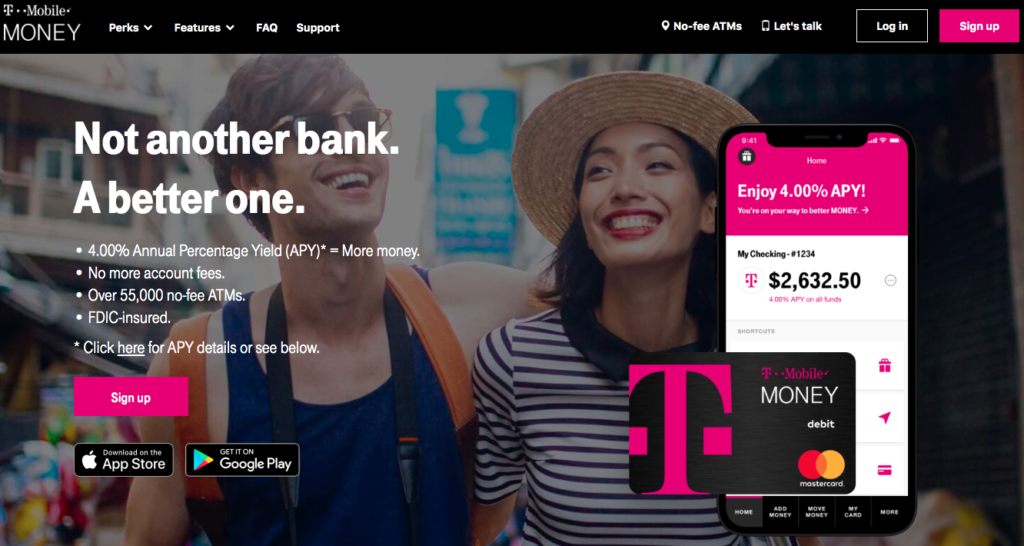

T-Mobile Money

Users earn 4% APY on balances of $3,000 or less. Any amount over the $3,000 threshold earns 1% APY. There is no minimum balance requirement but account holders must deposit at least $200 per month into the account to earn 4% APY.

TotalDirectBank

2.1% APY on balances of at least $5,000 and no more than $500,000.

Vio Bank

2.02% APY with a minimum deposit of $100

Many of these financial institutions are able to offer higher-than-average rates by keeping their operating costs low. In most cases, the lower operating cost is the result of being an online-only bank. However, two of the banks listed above (Digital Federal Credit Union and Elements Financial) have physical branch locations, as well.

Another aspect that helps with offering high interest is setting appropriate limitations. Interestingly, the two banks on this list that have branch locations (re: higher operating costs) are the two with the most stringent restrictions on their savings accounts. Setting up appropriate limits on account earnings can make banks’ offerings look attractive without costing too much. Conversely, too many restrictions will frustrate consumers and, perhaps worse, compromise trust.