There has been no shortage of major announcements in the payments space in the past few weeks.

- Facebook added a “send money” option to its messaging service

- Starbucks added pre-ordering into 650 northwestern U.S. locations in advance of a national rollout

- PayPal acquired the platform upon which MCX is built on

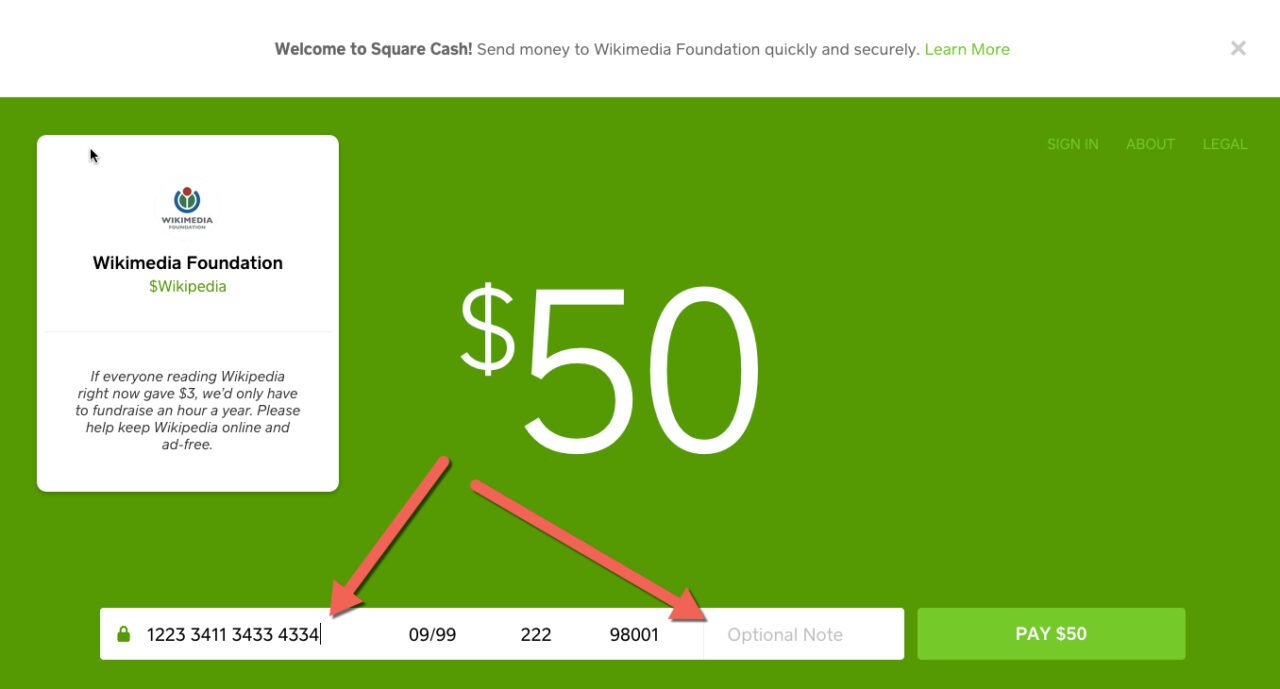

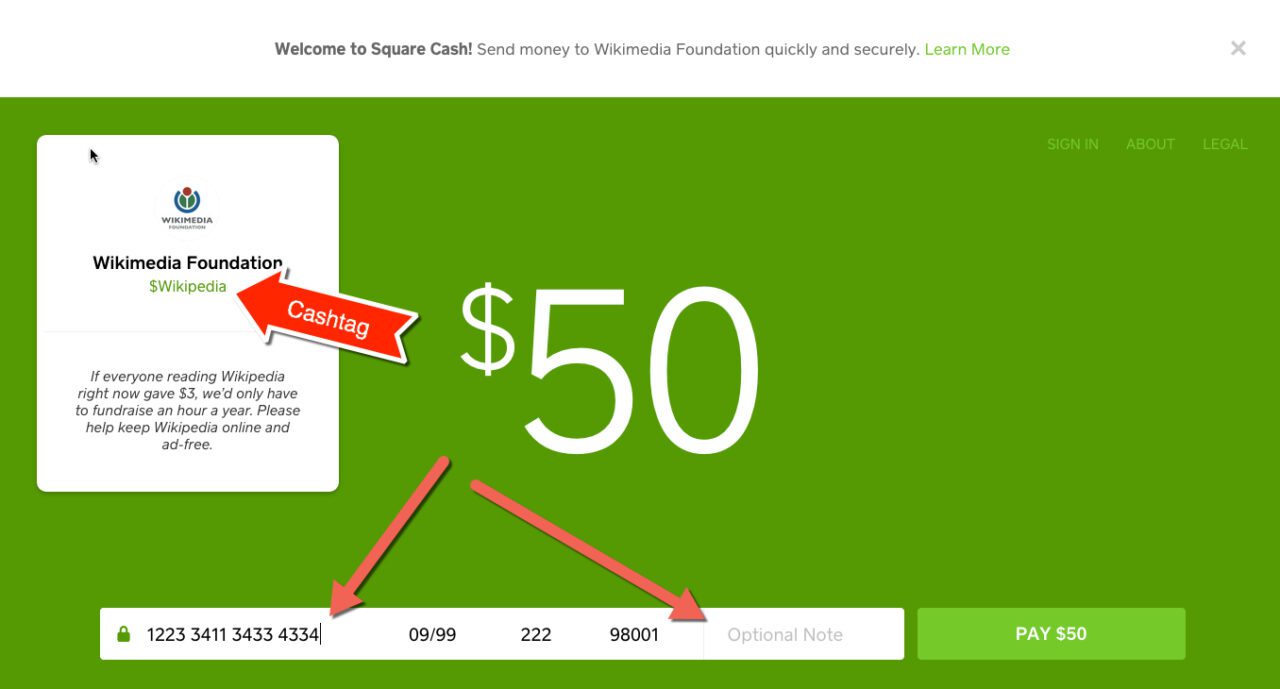

And yesterday, Square launched an SMB version of its Square Cash, brilliantly named Cashtags. Any person, business, or non-profit can create a cashtag out of its name (first-come, first-served) at cash.me/$yourname. Then to pay by debit card, users click on your cashtag, enter their debit card number, postal code, CVV and amount to pay. Space for an optional message to the business is also included. First time users also have to confirm their email address or mobile phone number, before the payment is sent.

For businesses, it’s not much different than using PayPal. But the setup is slightly less intimidating Square onboards new merchants gradually, so as to not scare them off before finishing the process. When I set up my original cashtag, all they asked was my email address or mobile phone number, which was subsequently verified. It was only later when I was playing with that app, that they hit me up for my full name and last 4 digits of my social security number.

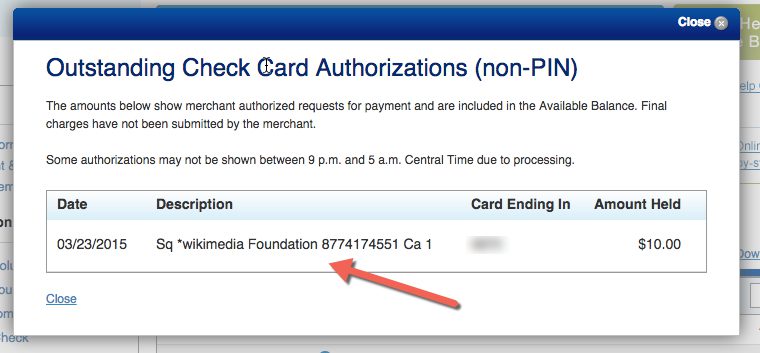

The big difference is in pricing. Square Cash business recipients pay a 1.5% transaction fee (with no per-transaction flat fee), undercutting PayPal business account fees by about 50% (both Square & PayPal have free options for non-business person to person transfers). I sent a few bucks off to Wikipedia and it worked perfectly (see screenshot above). As it should, the debit authorization showed up right away in online banking (see below, from U.S. Bank).

FI Opportunities & Threats:

For financial institutions not actively involved in the acquiring business, here’s a chance to build ties between your business debit card and your small-business (SMB) customers, at little cost and with no cannibalization of existing revenues. The zero-cost approach is to simply educate your customers about this new option from Square. Since cashtags are available on a first-come-first-served basis, it would make a timely subject for an email, blog post, or online article.

A more involved strategy would be to incorporate Square Cash and Cashtags directly into secure online banking. While Square has not published an API to make integration easier, access to Square Cash could be added to your dashboard, even though it would still run through the Square UI.

The main downside for at least endorsing Square, and it’s potentially a sticky issue, is that Square Cash/Cashtags is part of a larger payment and lending business being built by Square. It’s possible, but not all that likely, that at some point Square could be considered a material competitor to your core business. However, if you are not in the acquiring business, you have already opened the door for others to provide payment services to your customers. Square is probably less of a direct threat than Chase, Wells Fargo or other major merchant acquirers.

And regardless of whether or not you steer customers to Square, you can mine debit card transaction history. Personal checking accounts with numerous Square and/or PayPal transactions are likely being used by someone with recurring revenues. That’s your first clue there is a potential new business banking customer in the mix.