SmartMoney just published its annual stock broker rankings (Note: currently the 2003 survey is posted, the 2004 should be there shortly).

There are now two categories of discount brokers: Premium and Basic. THere was little movement in the premium category year over year other than Vanguard droping from second to sixth and E*Trade making its inagural entry at number 2. Last year it was ninth in the basic category.

The best premium discount brokers:

____2004_________2003

1. Fidelity……….Fidelity

2. E*Trade………Vanguard

3. Schwab……….Schwab

4. USAA………….Quick & Reilly

5. T. Rowe Price..USAA

6. Vanguard…….T. Rowe Price

The basic category was more interesting with OptionsXpress coming out of nowhere to take the number one spot. SmartMoney’s comment, “nearly flawless.”

_____2004____________2003

1. OptionsXpress…….TD Waterhouse

2. Muriel Siebert……..Muriel Siebert

3. TD Waterhouse……Bidwell

4. Ameritrade…………ScottTrade

5. HarrisDirect………..HarrisDirect

6. FirstTrade…………..BrownCo

7. ScottTrade………….FirstTrade

8. Wall Street Access…Ameritrade

9. BrownCo…………….E*Trade (moved to premium)

10. WallStreet*E………Wells Fargo (moved to premium)

Widespread Misuse of Gartner Online Banking Fraud Estimates

By now you’ve probably seen the MSNBC report by Bob Sullivan entitled, Survey: 2 million bank accounts robbed, followed by the subhead, Criminals taking advantage of online banking, Gartner says. The MSNBC article seems to say that 2 million U.S. consumers lost money from their checking accounts due to online banking.

In fact, here is what Gartner actually says in its report:

“Illegal access to checking accounts is the fastest-growing type of consumer fraud, and may

be proliferating through online channels.” (italics are mine)

The report goes on to say that most consumers do not know how they theft occured, only 17% believed that their info was stolen off the Internet, another 10% reported their wallet was stolen, and only 5% recall giving up personal info to phishers.

Gartner also says that 70% of the online consumers reporting losses also report that they banked or paid bills online, “which exposes their (codes) to the Internet.” However, what they don’t say is that close to 70% of ALL online consumers are banking or paying bills online, so it doesn’t look like there is strong correlation between the two.

Finally, let’s not neglect the sample size. It looks staggering in the headlines to say that 2 million people were robbed. But my back-of-the-envelope calculations show that the multi-million number was extrapolated from fewer than 75 respondents reporting a recent unauthorized checking account withdrawal (from Gartner’s survey of 5000 online adults). I’ll let the market research experts debate the exact reliability of Gartner’s extrapolation, but one should be wary.

As bad as the MSNBC article looks for the online banking industry, the NBC Nightly News with Tom Brokaw got even more carried away. They took an even bigger number, 4.5 million, which Gartner said is the number of people who have ever had an unauthorized checking account withdrawal, and mistakenly said that all those people were robbed via online banking. Here is the exact synopsis of the TV feature from the MSNBC website:

“An estimated 4.5 million Americans have had money stolen from their Internet bank accounts.

NBC’s Bob Hager reports.”

This is a great example of a respectable piece of research taken out of context which then begins to have a life of its own as other news media echo the original piece. Hopefully, someone will dig a little deeper and set the record straight. Since I was quoted in the original Sullivan story, before I had seen the actual Gartner research, I will be contacting him to urge a followup.

Just to show that not everyone takes the 2 million number at face value, a story posted today at NBC affiliate WEEK-TV quotes Peoples Bank (Bloomington/Normal, IL) CEO, Ed Vogelsinger as saying that despite having 20% of their base using online banking, so far no one has reported any Internet banking fraud. Way to go Ed.

We urge our readers to take appropriate steps through their PR channels to set the record straight. At a minimum be prepared to rebut the MSNBC numbers if approached by the media. Feel free to send any reporter our way.

Contact: Jim Bruene, Editor, Online Banking Report, at 206-517-5021 or email [email protected].

Reference: “Banks Must Act Urgently to Stop Account Hijackers,” by Avivah Litan, Gartner

Phishers Target the Royal Bank

Phishers struck another blow to the banking system when they demonstrated that they no longer need rely on random blanket emailing blasts. Case in point: within 24 hours of a real systems glitch at Royal Bank, the email thieves sent a massive fraudulent email playing off the legitimate systems outage.

One can only hope that this particular theft didn’t enrich the thieves. Otherwise you have a situation where there is an incentive for a thief to create havoc with a bank’s systems and then cash in through a well-timed phishing fraud.

Read more on the prevention of phishing at Online Banking Report (subscription required).

Washington Mutual Small Business Resource Center

Although not as robust as Barclays, Washington Mutual is

the only top-10 U.S. bank with prominently targeting startups. Through its

partnership with StartupNation, the bank has posted several articles on

its website, and also sends users to a cobranded

www.StartupNation.com

website to sign on for more tools and resources including webinars, resources,

and coaching. We don’t know the terms of the relationship, so we can’t judge the

cost effectiveness. However, we definitely like how WAMU is positioning itself

as a supporter of

small business.

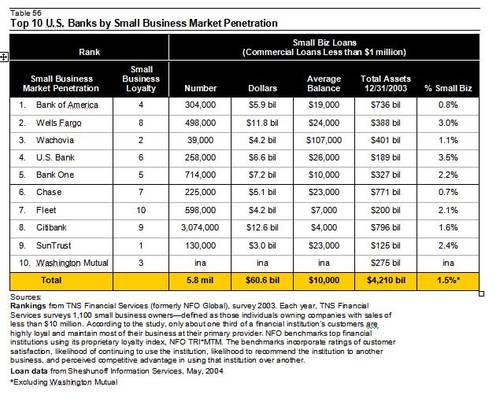

Top 10 Financial Services Providers by Small Business Market Penetration

In the 2002 study of small business, TNS (formerly NFO Global Financial

Services) looked at which banks had the largest share of small businesses

relationships and which were ranked highest by small business clients.

SunTrust ranked highest in customer loyalty, followed by Wachovia

and Washington Mutual.

1. Bank of America

Pros:

· Three levels of business online banking: online banking with

bill pay, Business Connect for multi-users with varied levels of

access, and Bank of America Direct to manage all business finances

online.

· Good comparison chart of the three choices

· Resource center with informative articles on starting a

business and other topics

· Protect against online fraud link

Cons:

· Must scroll down to see all choices

· Hard-to-read small blue font for most links

· No separate URL or bookmark helper

2. Wells Fargo

Pros:

· Small business tab

· Excellent navigation and design, all viewable on a single

screen without needing to scroll.

· Clients can view personal and business accounts from a single

sign-on

· Single page, informative Small Business Newsletter

· Customers and non-customers can enter email address to signup

for newsletter

· Relevant and useful tips on product pages

· Product comparison pages as well as best product for your

business quiz

· Push a button to switch from English to Spanish and back again

· Link to Make this your first page at WellsFargo.com

Cons:

· No link to Security on the main page

· Not using liquid layout, so homepage appears small and

off-center at higher resolutions

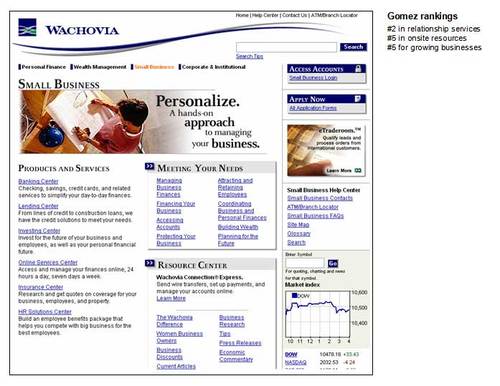

3. Wachovia

Pros:

· Small business is one of the four main navigation

choices on the top

· Copy and headlines are solutions-oriented, e.g., Meeting

Your Needs, Resource Center

· Excellent navigation and layout on a single page

· Separate small business FAQs

· Relevant products and services packaged into “centers”:

Banking Center, Lending Center, Investing Center, Online Services Center,

Insurance Center, and HR Solutions Center

Cons:

· Must scroll to see information on bottom of screen

· No link to Security

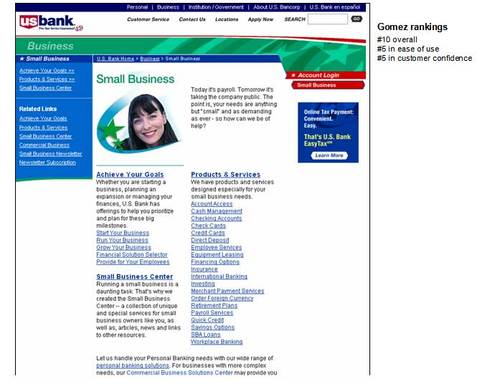

4. U. S. Bank

Pros

· All major links are contained on a single page without

scrolling

· The no-frills style is easy to read

· Two solutions-oriented sections: Achieve Your Goals and

Small Business Center

· Separate Small Business login

· Link to Newsletter subscription

Cons

· Layout and design could be improved

· No link to Security

5. Bank One

Pros

· Product-oriented layout makes it easy to find specific products

· Small link to Security on bottom (not visible on

screenshot)

Cons

· There is no small business section, in fact the term is

not used in any header, although it is mentioned in the opening paragraph;

choices are Business Banking and Commercial, that defies

industry conventions and could cause lost business

· No solutions-oriented areas or resources section

· Copy is cliché-ridden and not benefits oriented;

for example under Insurance:

“You’ve invested your heart in your small business.

We can help you find ways to protect it.”

6. Chase

Pros

· Small business is one of the four primary navigation

choices on the top

· Excellent design and layout that fits on one page without

scrolling

· Solutions-oriented sections: Plan and Learn,

Solutions, and Business Stages

· Link on left to Have Chase Small Business contact you

· Privacy & Security link on top

· Prominent Open an Account and Online Banking: Enroll

Now boxes in upper right

· Liquid layout

Cons

· No quick navigation or separate URL for the small business

page, you have to click on the Small Business section on the home

page, then move your cursor down the cascading menu to the Small Business

Home, it only takes a few seconds but it’s still unnecessary extra

effort

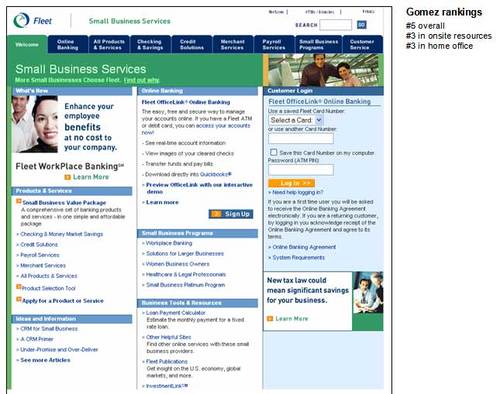

7. Fleet

Pros

· Separate URL

http://www.smallbiz.fleet.com/

· Tabs across the top help users find important subjects

· Link to Small Business Value Package (Note: Fleet also

offers a Small Business Platinum Program with a dedicated

relationship manager, faster funds availability, and priority phone service

· Solutions-oriented areas: Ideas and Information,

Business Tools & Resources

Cons

· Layout and design is a bit overwhelming

8. Citibank

Pros

· Using the drop-down menu you can navigate directly to relevant

business unit pages; the AAdvantage Business Card main page for

example is very well done

Cons

· Poor navigation off the home page: The only way to navigate to

the small business section is to use the drop-down menu on the right;

and because it doesn’t have a Go button, it took us 30 seconds before

we figured out you have to cursor down to Small Business at-a-glance

(screenshot above) in order to move to the small business section

· Poor navigation within the small business section: The four

main choices at the top of the page (Products, Planning, Investing,

and Special Offers) are NOT related to small business, they take you

back to consumer

http://www.citibank.com/ pages, and if you don’t use your back

button, you have to go through the full navigation routine to get back to

small business

· Must scroll down to see all the choices

· Main banking link (Checking, Savings, & Financial Services)

as well as the Online banking link cause a pop-up screen to load

which is dominated by an outdated self-promotion for online personal banking

with 2001 testimonial from Forbes magazine

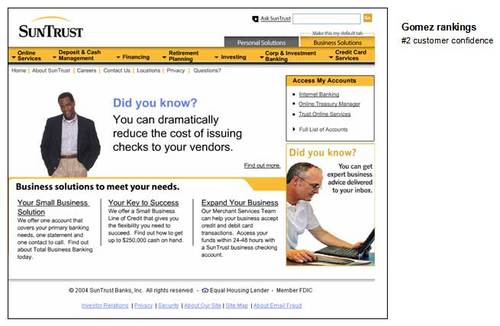

9. SunTrust

Pros

· Small Business Resource Center is a good area, although

it’s buried under the Online Services tab in the Business

Solutions area

· View only option for online banking, no money movement

allowed

· Ask SunTrust search box in upper right is handy, but it

doesn’t distinguish whether user in searching from business or personal

pages

Cons

· The top navigation bar is a mine field of cascading menus that

launch when the mouse travels over them, an out-of-date and annoying method

for primary navigation

· No dedicated Small Business homepage, other than the

Small Business Resource Center mentioned above and a mid-page link to

Your Small Business Solution which leads to a curious page entitled

Benefits that talks about Total Business Banking, but it’s not

clear if it’s geared to small businesses or not.

· Unclear and vastly different navigation/organization in the

various areas devoted to small business (e.g., Small Business Resource

Center)

10. Washington Mutual

Pros

· Link to content from StartupNation in upper-left corner; the

only bank in top 10 with headline targeting startups (see back page for more

information)

· Good online banking demo with audio highlights

· All the information shows on a single page without scrolling

· Liquid layout

Cons

· No link to Security

· Copy and headlines could be more solutions-oriented

· Layout is a bit sparse for a bank

Innovators in Small Business Online Delivery

Innovators in small business online delivery

|

Table 55 Watchfire/Gomez Small Business Scorecard

Source: Watchfire, 6/04 <gomezpro.watchfire.com> |

Our first report on small business banking was produced in the fall of 1997

(OBR 29).

At that time, few banks were specifically targeting small businesses. Then,

a Yahoo search for “small business” and “banking” yielded only 19

results compared to 2.5 million today. In the late 1990s, most banks were

still busy building out their consumer interfaces. Even as recently as 2001

(OBR 70/71), we found few major innovations to report on. Our

favorite small business banking service was OneCore

http://www.onecore.com/ which was

shuttered shortly thereafter, at least as a direct provider.

Today much has changed. Everywhere you look, banks are innovating to

serve the small business market more effectively. According to

Watchfire’s GomezPro unit the best small business banking sites

are Bank of America and National City, tied for first place in

its year-end 2003 scorecard (see Table 55, right).

Other online innovators in the small business market:

- Barclays Bank (London; $800 billion) uses its

website to target startup businesses with a broad array of support

services that many startups would find essential, including a free

business checking account for the first year. It’s so impressive, we’ve

given it our second Best of the Web award this year

(see next page). - PNC Bank (Pittsburgh, PA; $70 billion) and

NetBank have both announced plans to offer remote check deposits,

something most U.S. banks will support within a few years. One of the

last reasons to visit the branch will be eliminated when clients can

feed paper checks into a scanner instantly depositing the cash into

their account and storing the image into their online banking archive

This service is a shoo-in for an OBR Best of the Web once it goes

live. - NetBank (Alpharetta, GA; $4.1 billion) which

launched a new small business initiative a year ago, has attracted 1,600

businesses with $38 million in deposits ($24,000 average deposit). If it

keeps to the announced third-quarter launch, NetBank may be the first

bank to offer remote paper check scanning

Barclays provides valuable services for startups

Why do the U.K. banks do a better job serving small businesses online

compared to their U.S. counterparts?1 Perhaps U.S. banks are

underestimating the value of services targeted directly to small business

owners. Or maybe they’ve found it too difficult because business owners

won’t bother switching bank accounts to save a few bucks a month. That’s why

it makes so much sense for Barclays Bank to focus on startups

at its business website <business.barclays.co.uk>. After all, if you

succeed in being a startup’s first bank, you have the inside track to retain

its business over time.

Barclays business homepage (see below) is dominated by a shaded

area asking the important question, Starting a business? Even though

the vast majority of visitors already have a business and a banking

relationship with Barclays, those most likely shopping for services are

startups. The bank also offers Pain relief in a box, a proprietary

business management and accounting program targeted for tiny businesses or

startups that haven’t settled on an accounting software system.

1Two out of three of our Best of Web winners for small

businesses are headquartered in the U.K.

Barclays’ small business Starter Accounts consist of the following

features and benefits:

- Current account (checking) with an overdraft facility; free

for the first 12 months, 18 if you also maintain personal accounts at

Barclays - Savings account

- Loans, subject to credit approval of course

- Insurance

- 45-minute free consultation with a business/marketing

consultant - 45-minute free consultation with an accountant

- 30-minute free consultation with an attorney

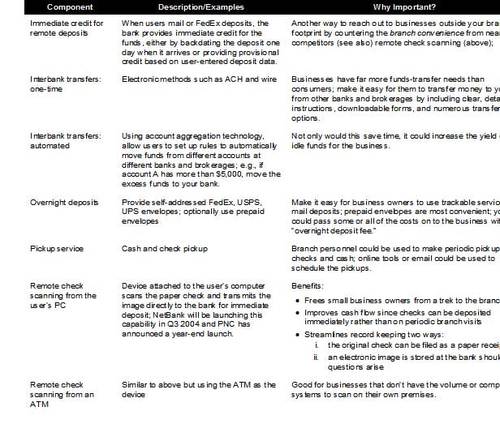

NetBank and PNC to offer remote deposits

According to recent press reports, both NetBank (American Banker,

May 20) with 1,600 small business clients and PNC Bank (Wall Street

Journal, June 8) with 200,000, will launch remote deposit service for their

business customers. Although details of the yet-to-be-launched services are

sketchy, it is expected that business customers will be able to scan paper

checks into a remote device that transmits images to the bank for immediate

deposit. PNC estimates the scanners will rent for $15 to $25 per month. No word

on pricing from NetBank. The NetBank service is expected in late third quarter

and PNC expects to roll-out by yearend. Alogent

http://www.alogent.com/ is the

technology provider for NetBank.

Benefits for small business owners:

1. Saves time/money: Frees business owners from the daily/weekly

trek to the branch, something 80% of online self-employed households reported

doing during the past 30 days according to Javelin Strategy

2. Improves cash flow: Checks can be deposited immediately rather

than collecting dust waiting for the owner’s next trip to the branch

3. Streamlines record keeping:

i. the original check can be filed as a paper receipt if desired

ii. a back-up electronic image is stored at the bank if questions arrive

4. Improves customer service: Check images can be quickly retrieved

and emailed if

a dispute arises

5. Saves storage space/cost: Paper checks can be destroyed much

sooner, eliminating storage and security issues

6. Improves management control: Owners can spot-check deposit

activity by looking at actual check images, rather than staff-entered accounting

entries

Speaking as both as a small business owner and an industry analyst, this is a

great service and a strong candidate for a Best of the Web award once it

becomes operational.

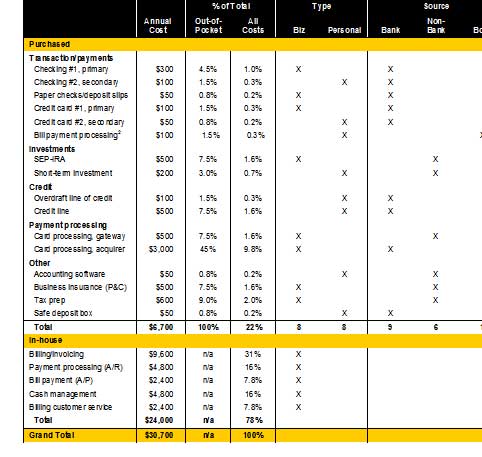

Small Business Case Studies: Putting it all Together

Case Study: Financial product usage at one small business

Microbusinesses typically purchase a hodgepodge of

services culled from both retail and commercial banking product lines. For

example, at our own small business, we purchase 16 financial products evenly

split between consumer and business products (see Table 52, below).

Nine are sourced from banks, six are from non-banks, and one is a combined

effort. Overall, we spend $6,700 annually in fees, interest paid, and

interest foregone (for checking). But the internal costs for managing our

billings, payments, and banking, are more than three times as much, an

estimated $24,000 per year. We would gladly outsource these to a

high-quality and VERY trustworthy third party, preferably someone with a

regulatory and fiduciary responsibility to safeguard our information and

assets, like a bank.

Table 52

Financial Products & Services Used by One Small Business

Source: Online Banking Report, 6/04 1Fees and net

interest foregone (deposits) or paid (loans) assuming 2% cost of funds

2Purchased through US Bank, but processed by CheckFree and user

interface by Microsoft Money

Package accounts targeted to business segments

Most banks offer small business bundles that include checking and

other basic transaction services. However, we believe the online platform

can be used to assemble more valuable offerings targeted to small businesses

with various financial management needs. Table 53 (below) shows ways

that the small business market could be segmented. Table 54 (p 53)

outlines major feature that could be included in package accounts targeted

to the financial management needs of the small business.

Table 53

Potential Business Segments to Target

Virtual financial management packages

Most banks offer small business account bundles that include checking

and other basic transaction. We believe that there is a significant

opportunity to expand into hosted financial and customer management systems

with monthly fees of $100 or more. Following are the pros and cons of moving

into the financial management arena:

Pros

- Profitable, incremental fee income

- Publicity and image enhancement from being the first in

your market to integrate banking functionality into an overall Web-based

small business management suite - Product differentiation and an impressive unique

selling proposition - Positive word-of-mouth within the local business

community - Powerful retention tool

- Potential for licensing to other financial

institutions

Cons

- Weak/uncertain demandd: Until recently, small

businesses have been slow to adopt new banking technology. It may take

several years of marketing, sales, and training before you begin to see

a payback. - Development costss: Building a robust, highly secure

new system will be pricey; you will probably want to partner with an

accounting software developer that already has code for the basic

functionality. - Uncertain ongoing servicing costss: Being on the

bleeding edge has its risks; it will be difficult to predict ongoing

costs for system maintenance, software development, and customer

support. - Lack of employee confidence: Financial institution

front-line personnel have been known to steer clear of discussing small

business and/or online banking subjects due to uncertainty with their

operation, cost, and overall value.

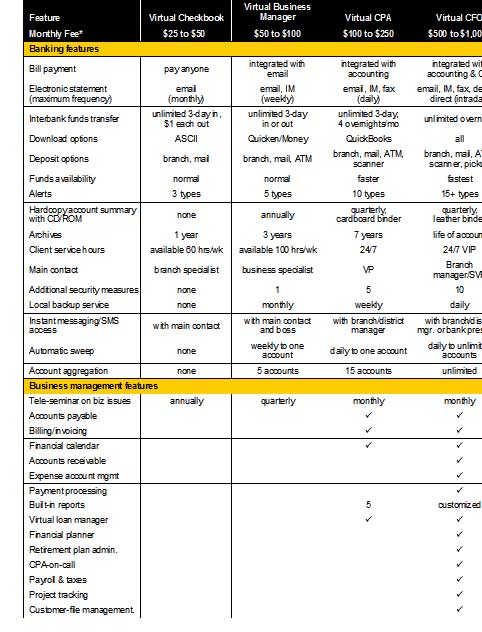

Table 54

Features of Virtual Accounting Package Accounts

*Approximate monthly subscription price; additional transaction fees

would apply for certain services.

Package Account Descriptions

Virtual Business Manager

Description: A secure place for small businesses to set up an

online home base, similar to corporate intranets. Possible names: virtual

office, virtual desk, virtual briefcase, or personal intranet. It could also

be marketed to the estimated 39 million U.S. households with a home office.

Functionality: For a financial institution, the key to making it

work is tight integration with banking and financial matters. A further

emphasis on local content/links could keep you ahead of the competition.

Banking and financial management feature are listed in Table 54 (previous

page), including:

- Financial calendar/datebook/reminder service

integrated with bill payment - Virtual safe deposit service that automatically

stores financial and other files in secure, encrypted, off-site back-up

files not accessible by anyone but the owner (not even bank personnel);

can be retrieved on CD for disaster recovery - Virtual receptionist that tells visitors how to get

in touch with someone at your business - Company message boards for internal users

- Company blogs for external users

- Ability to post documents to the Web, which can be

shared with everyone or just authorized employees and/or customers

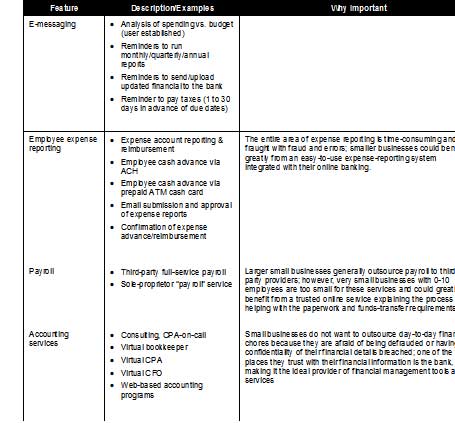

Virtual CPAA

Description: As its name implies, the Virtual CPA provides

extensive accounts-receivable and accounts-payable services from a Web

interface.

Functionality: In addition to the Virtual Business Manager

features listed above and the banking/financial management features listed

in Table 54, the VirtualCPA could also provide the following features

(for more ideas, see the features built into Intuit’s QuickBooks

http://www.quickbooks.com/

- Billing statements and invoicing via email, fax, or

snail mail; includes reminders, and confirmations - Online, cash-based accounting functions including

data entry, categorizing, and basic report generation - Bill-payment/accounts-payable monitoring functions,

such as email notification when payment transactions are awaiting

authorization by business owner; email flags when payment transactions

don’t clear in a reasonable time - Autopay function that pays certain bills

automatically each month when preauthorized by the client - Virtual credit card terminal with integrated email

and accounting - Lock-box service for paper check processing with full

integration to client’s accounting system - Option to share selected information with outside

advisors, such as a CPA

Virtual CFOO

Description: This top-of-the-line service has it all. Just as in

the real world, the Virtual CFO takes the raw data and puts it into a

broader perspective that allows a business to be more profitable.

Functionality: The following features could be added to those

already offered in the Virtual CPA and Virtual Business Manager

modules:

- Online payroll with paper or direct-deposit paychecks

and electronic tax payments - Online federal and state tax return preparation and

filing - Full-fledged, double-entry online accounting

- Complete disaster-recovery services including a

redundant data center – an area in which banks’ inherent in-house

expertise could be turned into a profit center - Complete Web-based customer file management and

communications including:

– invoicing/billing with Web integration, e.g., bill presentmentt

– payment services/inquiry via the Web

– email/fax/voice messages automatically confirming payment - Access to a CPA-on-calll for accounting and tax

questions; advice could be delivered publicly on your Web, privately

through confidential conversations, or both. - Automatic excess funds allocation to minimize

interest expense and/or maximize interest income. For added value, the

funds “sweep” could go to investment and loan accounts at any financial

institution (not just yours). - E-commerce services for hosting secure transactions

- Accounts-receivable management that automatically

notifies the business owner and/or customers when accounts are past due;

includes linkages to a virtual payment window - Bank-branded virtual payment windoww, which clients

can display on their website to increase end-user confidence in paying

by credit card or electronic check (ACH); includes integrated messaging

confirming orders. - Extensive management reporting easily customizable

using drop-down menus; for example, revenue reports by customer,

accounts receivable aging, quarterly P&L; and so on. - Mail-merge capabilities that work across any medium,

email, fax, page, voice message, or snail mail; option to outsource

snail mail services to a mail house; includes label-printing utility. - Retirement plan administration including Web views

for participants - Project tracking module integrated with reminders and

other Virtual Officee services - Employee-expense reporting, cash advances and

reimbursement services - The ability to issue/reload prepaid credit

cards for customer rebates, expense account cash advances, and so on..

Recommended Online Products and Services for Micro Businesses

Small business attitudes are changing as online banking services become

easier to navigate and more useful. While it currently seems impossible to

eliminate the dependence on the branch for physical deposits, with the

widespread adoption of check imaging and electronic payments, most

non-cash-oriented businesses will be able to bank remotely. Both PNC Bank

and NetBank have announced plans to equip their business customers

with paper check scanners that will allow the remote deposit of paper

checks.

But even the best website and product offering cannot substitute entirely

for the human touch. Every business should have a contact available by

phone, email, or instant message. Small business owners should be treated

like private banking clients.

Recommended online products and services

In theory, small and micro businesses represent one of the most

lucrative, and relatively untapped, sources of incremental business. The

reality is that businesses are difficult to reach unless you are competing

for their loan business. A product offering optimized for business will

differ somewhat from one built for consumers. The following sections detail

potential online features for various microbusiness products.

A. Transaction accounts: checking & cards

While the overall banking relationship may revolve around the

commercial loan, online banking is all about the transaction account(s),

e.g., checking and credit card accounts. Smaller businesses often track

their financial progress through their bank accounts, using them as a proxy

for sales, cash flow, and profits. Business users are also more likely than

consumers to value advanced features such as downloads, reporting, alerts,

and multiple authorization levels. Some of the more promising features:

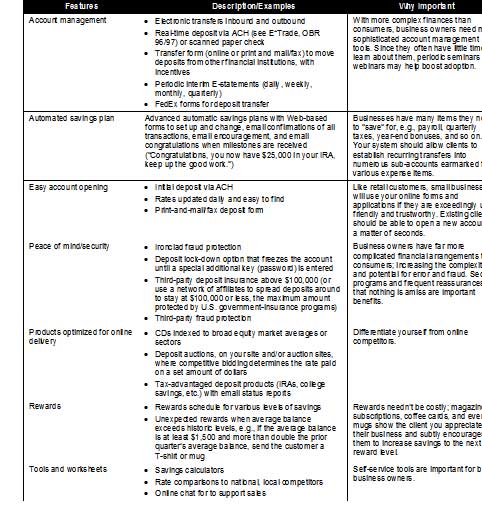

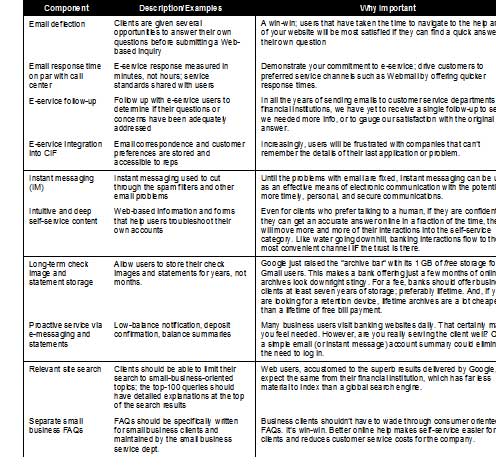

- Custom data delivery: Periodic summaries of account

activity whenever (daily, weekly, monthly) and wherever (text email, HTML

email, or fax) the client chooses - Long-term archives: If

Google can provide 1GB of

storage for users of its FREE email service, banks should be able to provide

unlimited archives for a fee

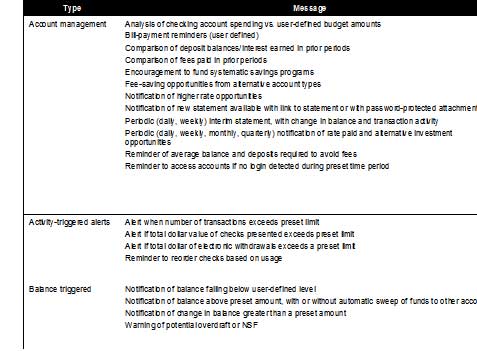

Table 27

Checking & Savings Account Deposit Options

Table 28

Online Features for Transaction Accounts: Data Display, Storage, and

Value Adds

Table 29

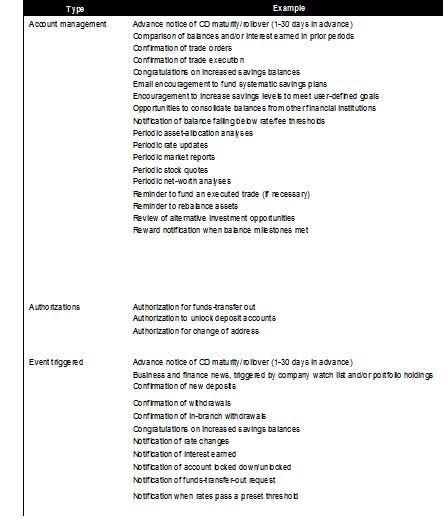

Event Triggered Alerts & Authorization Messages to Support

Transaction Accounts

Table 30

Balance, Activity, & Account Management Messages for Transaction

Accounts

B. Payment and billing services

Next to statement information, epayment services are the second most

important drivers to the adoption of online banking by small businesses. And

unlike data access, epayments have the potential to become profit centers

and/or a significant source of online differentiation. Most businesses make

far more payments than consumers, so the importance of electronic

alternatives is magnified. On the other hand, existing businesses already

have a system for payment and billing, so it may be difficult to convert

them to a new one that requires changes in internal procedures or software.

Your best opportunities may be in less systematic services (i.e.

one-offs) such as electronic transfers between a business’s accounts at

other financial institution (account-to-account transfers) and the

occasional rush payment.

Table 31

Online Features for Billing, Payment Processing, & Funds Transfer

Services

Table 32

Online Features for Payment and Accounts Payable Services

Table 33

E-messaging to Support Epayments and Ebilling

C. Credit and loan accounts

Every small business relationship should include a credit component. It’s

the lifeblood of business, and a profitable product for financial

institutions. However, many banks have been reluctant to make commercial

loans to the microbusiness market. Average loan sizes, which are dwarfed by

typical commercial loans, make the effort seem fruitless. Yet profit margins

on the small business segment can be higher. Microbusinesses often use

personal credit, primarily credit cards and home equity secured loans, to

finance their businesses.

We believe every creditworthy microbusiness customer should

have a package of three or four credit lines with your financial

institution: an overdraft line of credit (connected to checking), a home

equity line of credit secured by their personal real estate (if applicable),

a business line of credit, and a business credit card. Even if the total

commitment is no more than $10,000 initially, it will make the business

owner feel like a valued customer; and each line can grow larger over time.

Table 34 contains a number of ways to use the online channel to

strengthen credit relationships with small businesses. Some of the more

important tactics:

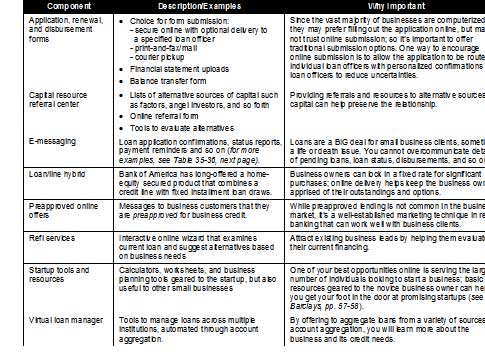

- Loan/line Hybrid: A flexible financing vehicle that

includes an integrated line of credit and the ability to take out fixed

loans from the overall credit line. - Startup Center: Information, tools, and resources geared

towards startup businesses.

Table 34

Online Features for Lending and Credit

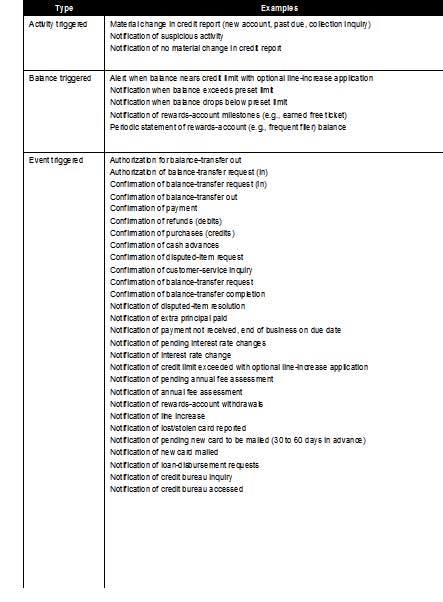

Table 35

Triggered Alerts for Credit and Loans

Table 36

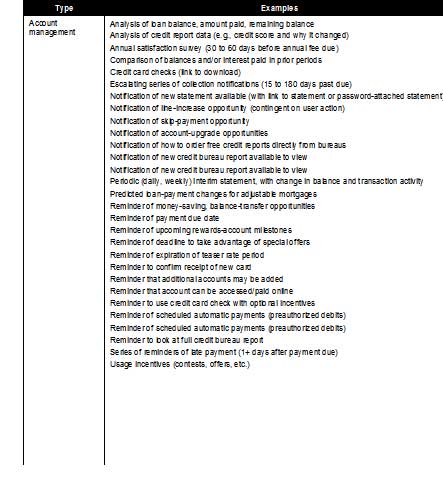

Account Management Messages for Credit and Loans

Table 37

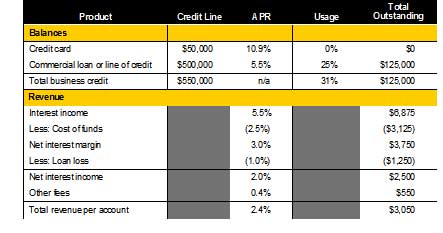

Example: Potential Annual Credit Product Revenue from a Microbusiness1

Source: Online Banking Report, 6/04

1Example for illustration purposes only, not based on actual

research results

Table 38

Example: Potential Annual Credit Product Revenue from a Larger Small

Business1

Source: Online Banking Report, 6/04

1Example for illustration purposes only, not based on actual

research result

D. Deposit and investment accounts

The online component of deposit and investment accounts is far less

important than for transaction and payment services. However, a robust

online offering can boost deposit-gathering initiatives and improve

retention. Key online components are listed below: Refer to the

Checking/Transaction section for more ideas.

Table 39

Online Features for Investment and Deposit Products

Table 40

E-messaging for Deposits and Investments

E. Financial management & accounting

Although automated accounting and financial management services offer the

biggest potential payback to small business owners, they are challenging to

deliver. However, working through third parties, financial institutions of

all sizes can help cement banking relationships with financial management

services such as:

- Visible and easy-to-use data downloading services

- Tools to make annual financial updates and tax prep simpler

- Online wrap accounts that handle all financial and accounting

needs for an annual fee, see the section on the Virtual CFO, CPA, and

Business Manager

Eventually, it won’t be enough to simply offer robust cash management and

online balance reporting to your business clients. Using the Web as a

platform to build industry- and customer-specific service offerings, we

expect a proliferation of specialized small business services during the

next few years. For example, several years ago QuickBooks opened its

code to developers

http://www.developer.intuit.com/ spawning numerous niche services

built on the small business accounting program. Check out the QuickBooks

Solutions Marketplace

http://www.marketplace.intuit.com/

As the economy continues to improve, big banks will aggressively court

small and mid-size businesses with creative financial management via

Web-based services. These innovations will help counteract the perception

that community banks provide better service. In turn, community banks will

fight back with online offerings that enhance personal service

delivered to local businesses. Luckily, vendor offerings will make even the

most complicated Web-based service affordable to the smaller financial

institution.

Intuit has already built impressive software-to-bank linkages for

QuickBooks and Quicken customers. To some extent, the shrink-wrapped

software is a Trojan horse, positioning Intuit-controlled links to its

partner banks right on the desktops of your best clients. You can fight back

by incorporating billing, accounting, and financial management functions on

your website using account aggregation, instant messaging, and “push”

publishing technologies. Although, it will take time, we think smaller

businesses will be very receptive to financial and management services

running on encrypted, secure, and trusted servers controlled by the bank..

Table 41

Online Features for Financial Management

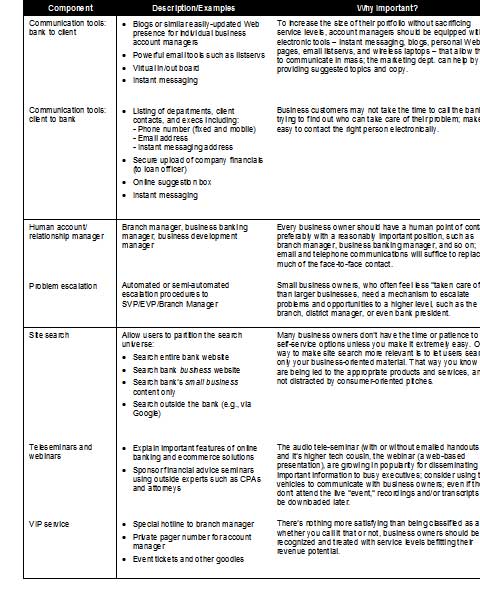

F. Service & client relations

Online services and other automation tools can be used to help

relationship managers service and cross-sell to small business clients. Used

judiciously, these tools can improve the perception of personalized service,

even while they improve the productivity of the relationship managers by

allowing him or her to handle a larger portfolio. Key components include (see

Table 42 below for more):

- Library of recommended preformatted emails that relationship

managers can easily customize and send to clients - Private-banking-like service that treats small business owners

like VIPs - Instant messaging for more private/secure connection between

the client and their business banking officer

Table 42

Online Features for Self-Service

Table 43

Online Features for Client Relations

Table 44

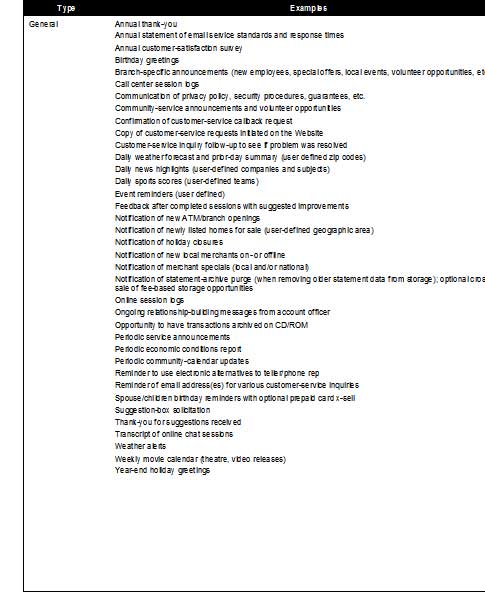

General E-messaging to Support Client Relationship Management

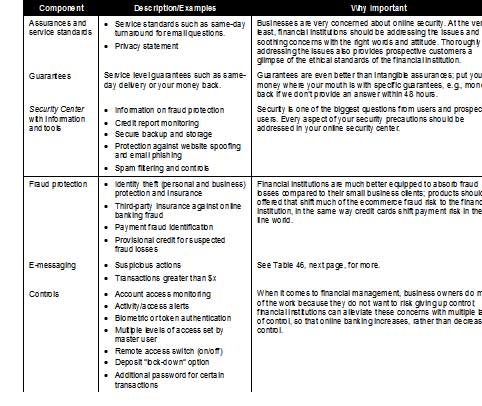

G. Security and privacy

Although business users may understand the tradeoff between convenience

and risk, the stakes are much higher. A breached small business bank account

could cause thousands of dollars of lost productivity and sales, in addition

to any funds that disappear. In addition, larger small businesses are always

up against the threat of insider theft and fraud. So business owners need,

expect, and will pay for more sophisticated security controls. For example:

- Additional authentication and/or authorization for outbound

funds transfers or payments - Token- or SMS-based authorization to access the account’s

master level where new payees can be added, permissions can be granted, and

so on - Frequent email messages tracking online account access and

alerting the business owner to any suspicious or out-of-character usage,

e.g., login from an IP address in Liberia - Comprehensive assurances and guarantees that accounts will not

be compromised

Table 45

Online Features for Security & Privacy

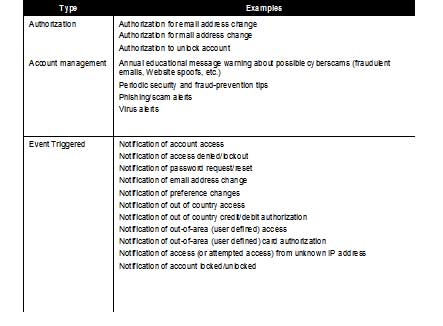

Table 46

E-messaging to Support Security & Privacy

H. General website content/features

As branches are gradually replaced by websites as the place where most

banking business is conducted, your online presence will become a critical

part of your overall brand image. Branches will still have a role, but it

will be limited to account openings, cash deposits, and the occasional visit

to the safe deposit box. Websites catering to small businesses will become

far more sophisticated, yet highly customizable and easier to use. Important

features include:

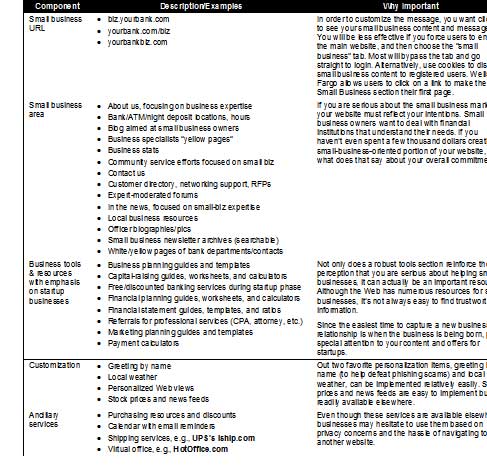

- Resources and discounted banking packages for start-up

businesses - Separate URL that business clients can enter to skip the

consumer section

Table 47

General Website Features to Support Small Business

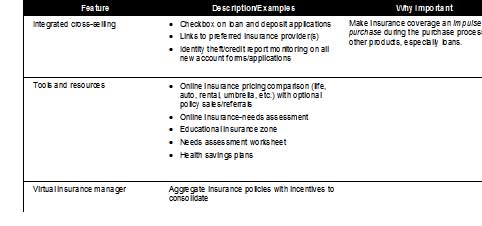

I. Insurance

Compared to consumers, small businesses buy a lot of insurance compared

to consumers. While banks may not be “top of mind” when it comes to

supplying insurance, financial institutions can use their online presence to

change that perception.

Table 48

Online Features for Insurance

Table 49

E-messaging to Support Insurance

J. Online sales and marketing

Even though microbusinesses are difficult to reach through traditional

direct marketing, we believe they will readily seek you out if you provide

credit and payment solutions targeted specifically to them, especially when

in startup mode.

It’s important to make sure everyone, especially the line staff,

understands that microbusinesses are to be actively courted, not avoided.

Typically, bankers roll their eyes and trot out horror stories about past

“nightmares” with flaky microbusinesses. Staff must be educated to the

facts: Microbusinesses can be risky, but with proper pricing and risk

management, the segment provides an excellent source of incremental profits.

In sales efforts, leverage the cachet of the branch manager. A single

telephone call or visit with the local branch manager could be enough to

land an entire microbusiness account. This all-important relationship with a

human must be nurtured after the initial sale. Email, instant messaging, and

other electronic tools can be effective in keeping the communication

channels open.

Some other effective ways to increase your share of the microbusiness

market:

- Uncover microbusinesses within your own retail customer base by

looking for random and fluctuating deposit activity. - Develop Web content

that caters directly to the small business segments you are targeting, such

as- – Part-time businesses

- – Self-employed (including full-time sales) or 1-person business

- – Micro employers with fewer than 5 employees

- Use professional copywriters familiar with small business

terminology to create website copy, including FAQs. - Give business bankers “ownership” of the business part of your

Web site to make sure it is up-to-date and speaks to the target markets. - Enlist business owners to evaluate your website and other

marketing material

Table 50

Online Marketing & Sales Tactics for Small Business Acquisition and

Retention

Table 51

E-messaging to Support Small Business Sales & Marketing

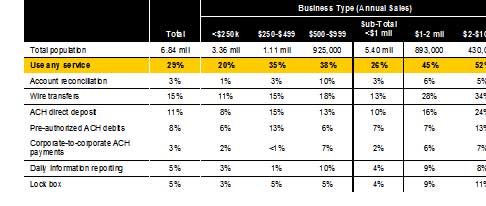

Small Business Online Banking Usage

Online banking usage

Up until a few years ago, small business usage of online banking trailed

consumer adoption. In late 2000, 13% of small and microbusinesses used

online banking compared to 16% of consumers . Three years later, online banking penetration is similar to that of

consumers, an estimated 30% overall. At the largest small businesses, those

with sales between $5 and $10 million, usage is now more than 40%, double

the rate three years earlier.

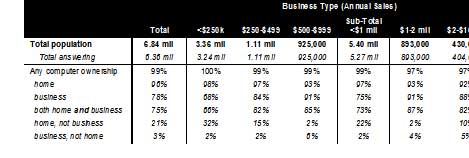

It’s likely we’ll see continued rapid growth for a few more years. Almost

all (99%) small businesses are computerized, either at the business or at

the owner’s home, or both (see Table 18, above) and more than 75% are

using their personal computers for financial activity (see Table 21, next

page). It’s only a matter of time before the majority of small

businesses bank online. Looking at the 7.3 million small and microbusinesses

universe, we predict that we’ll pass the 50% penetration point within four

years. However, we may reach that point much sooner. One researcher,

Synergistics Research, is already saying that online banking usage

has passed the 50% mark in the $100,000- to $10-million segment, with the

largest small businesses

($5 to $10 million) topping out at 75% penetration.

Table 21

Small business online and PC financial services usage,

2002

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use

Reasons for not banking online are typical, with security and

inconvenience (compared to current methods) the most-cited reasons (see

Table 22, below). Only 8% mentioned it was too expensive and only 5%

said they didn’t have the necessary equipment (presumably convenient online

access).

Table 22

Reasons for not conducting either business banking or

investing online

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use

Table 23

Online banking, billing, payment and other online activities

Q. Does your company use the Internet …?

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use, April 2003

Table 24

Cash Management Usage

Q. Please indicate if the service is

used?

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use, April 2003

Advisor usage

While small businesses still turn to their banker for loan

advice, only 17% use a banker for cash management advice, and just 4% for

retirement planning (see Table 25, below). Because small businesses are

skeptical of bankers’ expertise in non-traditional areas, banking organizations

must first explain why they are selling the product, and why the bank’s solution

is superior to more traditional sources. It may be advantageous to partner with

brand names that are more closely associated with the non-traditional product,

e.g., Safeco for business insurance.

Regardless of the channel the customer chooses to get

information and make transactions, a human is usually needed to close the sale.

In a recent Synergistics Research survey of 600 small businesses, only 7% had

opened bank accounts remotely (see Table 26, below). The sales process

can be assisted by email and phone with a branch manager, business banking

officer, or a special small business liaison.

Small Business Loyalty & Growth Potential

Small business loyalty

One consistent trait across all small businesses: loyalty.

Once you land one, it takes significant upheaval, such as a new commercial

loan relationship, before they make a move. NFO research indicates that 81%

of small businesses use the same bank for personal and business services.

And in a survey of Barlow Research clients, about 60% said they kept their

personal and business accounts at the same bank. Evidently, it’s just not

worth the entrepreneur’s time and energy to shop banks, unless they are in

the midst of raising capital. That’s why we believe it is vitally important

to establish a credit relationship with every small business customer

regardless of size.

However, high loyalty is not necessarily the same as high

satisfaction. According to NFO, in 2003 57% of small businesses are very

or extremely satisfied with their primary financial institution, up

from 50% in 2002. This is a mediocre score overall. And with the advent of

the online channel, it is easier than ever to shop around. And since only

22% of small business customers report being actively courted for their

deposits and investments, incumbent financial institution may be vulnerable.

Typically it has been the interaction between the business

owner and the commercial loan officer that has maintained, or sunk, the

relationship. Though personal relationships are still the primary factor,

electronic communications and online services are becoming important side

benefits. The savvy loan or banking officer can use email, instant

messaging, and a Web presence to supplement and extend the face-to-face

relationship. Staying in touch, asking for feedback, and identifying new

needs can all be done through frequent electronic communications.

Growth potential

|

Table 17 Accounting Method by Small Business Type

Source: Online Banking Report, 5/04 |

The small and microbusiness market holds much promise for financial

institutions looking to grow revenues and profits. Smaller businesses, which

are almost 100% computerized (Table 18, next page), are particularly

well-suited for online delivery; however, since most lack dedicated

resources to handle banking matters, they can be reluctant to change

existing processes and procedures. Even though your bank’s latest online

feature may draw an enthusiastic response in focus groups, expect slow

adoption by small business clients. They are simply too busy to pay

attention to incremental banking improvements.

While banks and other financial providers have long coveted the small

business market, most have found it difficult to provide the high-touch

services needed by business owners at prices that a smaller business can

afford. However, we believe small business online banking offers a new

paradigm. Automated online tools and electronic communications such as

instant messaging and webinars, allow banks to deliver customized products

at affordable price points, both for the smallest home-office-based sole

proprietor as well as companies with hundreds of employees.

Table 18

Small business PC ownership

Source: NFO Financial Services Group SOHO/Small Business Owner 2002 Online

and Channel Use

The Forecast Growth New Small Business Online Banking

Looking at the entire universe (including self-employed and contractors),

for 2004 we project growth of 2 million new small business online banking

users, a slight decline from the 2.5 million who came online in 2003. And

the rate of growth, due to the higher base, will slow to 17% from

2003’s 28% (see Table 9, below).

Table 9

Forecast of U.S. Small, Microbusiness, and Self-Employed Online

Banking Usage

includes broadest definition of small business

users, population estimated at 23 million

Source: Online Banking Report projections based on industry data (+/-

30%), 3/04;

% OLB = percent of total population that is actively banking and/or paying

bills online (activity within past 6 months)

Table 10

OBR Forecast: Small Business Use of Online Banking

businesses with annual revenues from $50,000 to $10 million, not

including self-employed/contractors

Sources: 1998 to 2002 estimates, TNS Financial Services Small Business

Market Track, April ’03; (1) 1995 to 1997 and 2003 to 2013: Online

Banking Report estimates plus or minus 33%

The opportunity at your financial institution

For a rough approximation of the small business potential in

your market, use the national average business-to-consumer penetration. For

example, there are approximately 90 million U.S. households with bank

accounts. Therefore about 25% (23/90) are business owners. About 8% (7.3/90)

own businesses that are relatively easy to find via identifiable business

phone lines, D&B reports, compiled lists and so on. The difference, about 16

million, are harder-to-find self-employed and contractors.

Table 11

Estimating the Number of Microbusinesses in Your Market

Number of banking households in your market

(fill in)

Multiply by the percentage of all households that are microbusinesses

x 8% or 25%*

Approximate number of microbusinesses in your market

= _____

Source: Online Banking Report, 6/04 *Depends on whether you are looking

at all businesses including self-employed/contractors, or just the

larger small and microbusiness segment

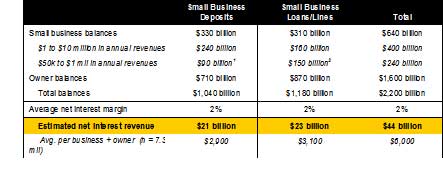

Total market size of balance-driven banking products

Looking at just the 1.2 million larger small businesses with

revenues from $1 million to $10 million (not including

self-employed/contractors), TNS Financial estimates total business deposits

of $240 billion and the total loans and lines of $160 billion for a total of

$400 billion. In addition, we estimated the microbusiness segment ($50k to

$1 million) has another $240 billion in deposits and loans. In addition, NFO

estimates that small- and microbusiness owners have another $1.6 trillion of

deposit and loan balances in their personal accounts, for a total of $2.2

trillion. Assuming a 200 basis point (2%) spread on the balances, the sector

is generating about $44 billion in net interest revenues, an average of

$6,000 per business/owner.

But, this only accounts the money paid out to financial

services companies. It ignores the significant internal and often hidden

costs associated with financial management: accounting, bookkeeping,

payroll, treasury, and so on. With the Web, banks have an opportunity to

compete not just for the traditional financial products, but also for the

entire financial operations of the business.

Table 12

Deposit and Loan Balances and Net Interest Margin from Small-and

Microbusinesses

Source: Small business ($1 to $10 million) segment and owner balances

from TNS Financial Services Group 2003 Small Business Studies, 4/03;

Microbusiness balances and average net interest margin are estimates from

Online Banking Report, accuracy estimated at plus 100%, minus 50%

1OBR estimate of $15,000 per microbusiness, n =

6.0 million

2OBR estimate of $25,000 per microbusiness, n =

6.0 million

Table 13

Small Business Assets by Type, Numbers and Balances

Source: Balances from TNS Financial Services Group (formerly NFO World

Group) 2003 Small Business Studies, 4/03

Table 14

Small Business Liabilities by Type, Numbers and Balances

Source: Balances from TNS Financial Services Group (formerly NFO World

Group) 2003 Small Business Studies, 4/03

Table 15

Misc. Product Usage

Source: Balances from TNS Financial Services Group (formerly NFO World

Group) 2003 Small Business Studies, 4/03

Table 16

Financial Products Purchased for Personal Use1 by Small

Business Owners

Warning: Small sample sizes of respondents with large balances may distort

the numbers.

Source: Balances from TNS Financial Services (formerly NFO World Group/PSI

Global) 2002 SOHO and

Small Business Owner Studies, 4/02; number of small and microbusinesses from

NFO’s 2003 Small Business Study, 4/03

Total population (N) = 7.3 million U.S. small and microbusinesses, not

including self-employed/contractors, OBR estimate +/- 20%

Does not include the value of the owner’s business, commercial real estate

investments, stock options, and other misc. categories

1Products used personally, not for the business

2Total market = (% using) x (average balance) x (7.3 million micro

and small business owners)

3Total balances only, does not include auto leases or insurance

4Across all business owners, users and non-users

5Net worth = personal assets less personal liabilities, does not

include net value of business or non-residential real estate holdings

6Total personal assets less value of residential real estate, does

not include net value of business or non-residential real estate

Barclays Small Business Banking

Q. When is a business most likely to open a new bank account?

A. When they are first starting out.

Recognizing that the best time to get their foot in the door at a business is before the doors even open, Barclays Bank (UK), addresses the issue front and center on its small business banking home page Barclays Small Business Banking : Small Business.

The company offers a number of startup service including complimentary consultations with business advisors and fee-free checking accounts (18 months if you also bank personally at Barclays, 12 months otherwise).