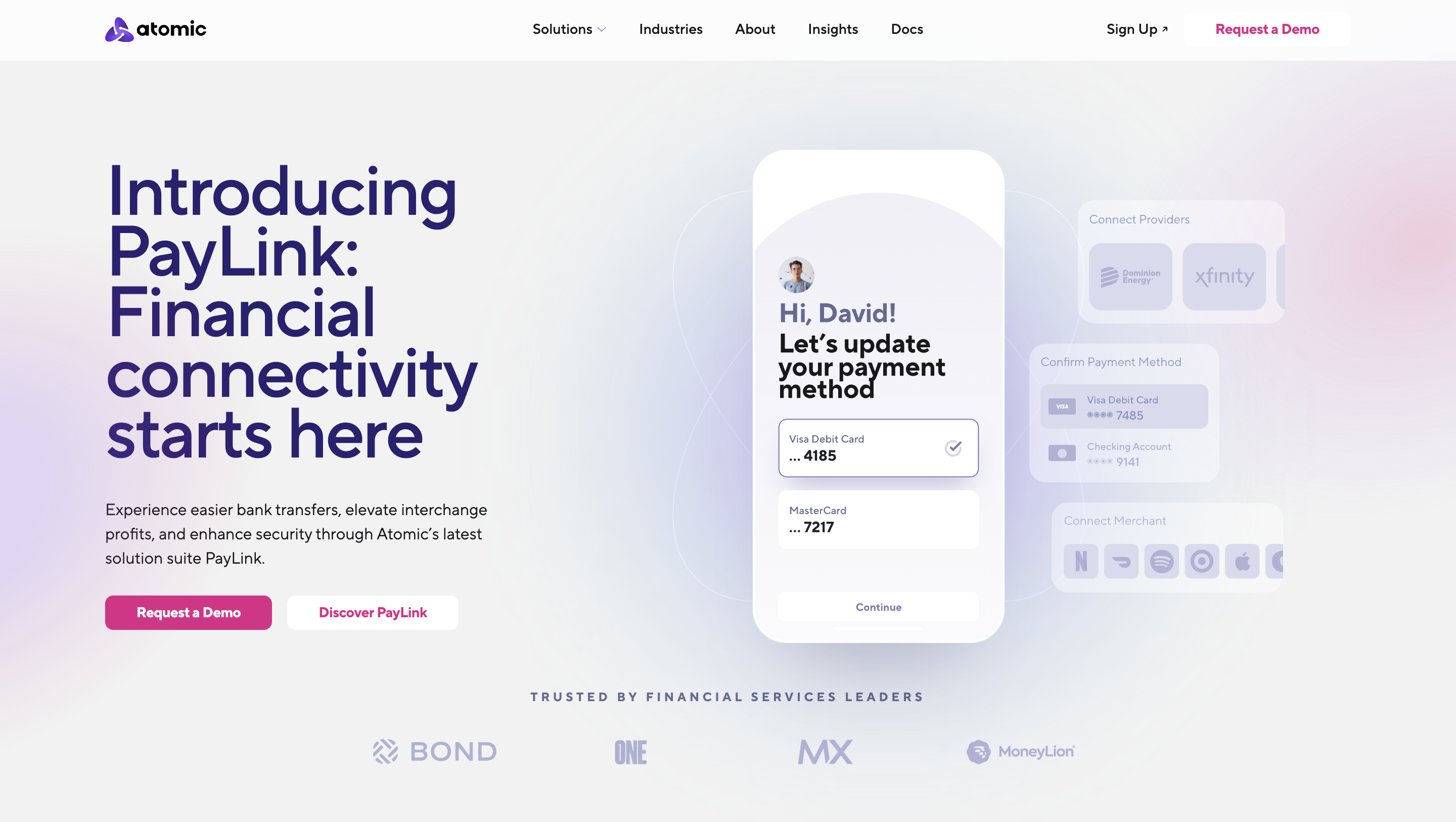

What is the future of open banking in the U.S.? Today, financial connectivity innovator Atomic launched PayLink, a new suite of solutions that streamline payment switching for consumers.

The new offering provides for an improved user experience for financial services consumers. It is also a big step towards helping banks and other financial institutions align themselves with the Consumer Financial Protection Bureau’s goals with regards to open banking.

We talked with Andrea Martone, Head of Product for Atomic, to learn more about PayLink, and the drive toward a more open banking system in the U.S.

Headquartered in Salt Lake City, Utah, and founded in 2019, Atomic made its Finovate debut two years ago at FinovateFall 2021. Jordan Wright is co-founder and CEO.

Congratulations on the launch of PayLink. Tell us more about this new suite of products.

Andrea Martone: Thank you! We’re thrilled about the launch of PayLink. We’ve taken our expertise in building user-permissioned connectivity for sharing and updating data and expanded it to merchant accounts, streaming services, and recurring bill providers, enabling consumers to seamlessly update their payment methods on file and retrieve information on upcoming payments. Building PayLink was a natural next step on our journey towards helping consumers update their primary banking relationship as it helps overcome a major point of friction in the process. To build it, we leveraged our cutting-edge TrueAuth technology that allows users to authenticate directly on their devices, without ever sharing login credentials.

For our readers who are new to Atomic, can you tell us a little about the company?

Martone: At Atomic we believe that making it simple for consumers to access, share, and update their financial data is key to unlocking new financial opportunities. By embedding Atomic’s SDK into their online and mobile banking applications, financial institutions can enable consumers to easily update direct deposit instructions, verify income and employment, import W2s and, now, update payment methods on file with merchants without leaving their application. With our solutions, financial institutions help grow new account adoption, qualify borrowers, and streamline tax filing.

Open banking was a major topic of conversation at our FinovateFall conference a few weeks ago. What is your take on the state of open banking in the U.S.?

Martone: Open banking in the U.S. is at an interesting juncture. With the CFPB taking bold steps in their public commentary, there’s an exciting momentum building around the consumer-centric transformation of financial services. While Europe has been ahead in this race, the U.S. is catching up, and I believe we are headed for an ecosystem that allows for significant innovations to support both consumers and financial institutions.

One of the issues that came up in our discussion on open banking was the idea that open banking is integrally related to the issue of digital identity. Do you agree? Why is this so and why is it important to keep in mind?

Martone: Digital identity is the backbone of a secure open banking ecosystem. As we democratize access to financial data, establishing secure, verifiable digital identities becomes crucial. It’s not just about sharing data, but ensuring that the right data gets shared with the right entities for the right purposes – securely. Our TrueAuth technology, for example, is designed to enhance credential security while empowering consumers.

The CFPB is working on regulations that could impact personal data rights. What are your thoughts on these potential regulations and their impact on companies in the open banking space – as well as the impact on consumer adoption of open banking?

Martone: I view the CFPB’s focus on personal data rights as a necessary step toward fostering a fair, transparent financial ecosystem. Giving consumers greater portability over their financial data opens the door for increased innovation and competition in the financial services space. However, it also creates a wider surface area for exploitation and misuse of data, as well. As a result, regulations will need to set the standards that ensure consumer privacy and data security and, in turn, build consumer trust. For companies evolving into the open banking space, this is an opportunity to align their products with consumer-centric values, which I believe will accelerate consumer adoption and loyalty in the long run.

Atomic is headquartered in Salt Lake City, Utah. We’ve seen a surprising number of innovative fintechs headquartered in Utah. What is it like to be a tech startup in the Beehive State?

Martone: Being headquartered in Utah has been fantastic for us. The state offers a thriving tech scene, a highly skilled workforce, and a business-friendly environment. We also have a dynamic team located throughout the country, which ensures that we comprise a diverse workforce.

What can we expect to see from Atomic over the next few months and into next year?

Martone: We have a busy roadmap ahead! You can expect to see more advanced features being rolled into PayLink, further strengthening its capabilities. You will also see us double-down on our strengths in expanding connectivity where it can benefit consumers to access, share, and update data in secure, transparent, and reliable ways to expand their financial opportunities. Key to this is continuing to advance our authentication methods, including our TrueAuth technology. Additionally, we’ll be focusing on strategic partnerships to widen our reach. Our aim is to continue leading the charge in making open banking a tangible, beneficial reality for all.