Without expansive brick-and-mortar operations to generate

business, card companies typically devote far more resources to direct

marketing and cardholder retention than retail banks. You can learn a lot by

watching what the card companies do online.

One

Develop a Killer App

Profitable online originations involve good marketing and a great

application. It must be short and sweet and loaded with imbedded help for

every term, otherwise only the desperate or dishonest will submit it. Most

major credit card applications today are a model of simplicity. For example,

Juniper’s online application (below) consists of a single screen

posing just seven questions beyond standard identification information

(name, address, phone number, etc.).

Two

Screen Out Improper Applications Before Submission

One of the main problems with non-preapproved credit card applications is

all the worthless applications received. Not only has time been wasted

researching the applicant’s credit report, but also your company must

carefully follow regulatory requirements for communicating denials, lest you

become a target of class-action litigators. Financial institutions,

especially credit card issuers, now start the application process with two

or three screener questions to reduce the number of applicants applying for

products for which they are completely unqualified. This is a win-win,

saving the bank application-processing costs, and helping applicants prevent

lowering of credit scores due to application denial. Juniper uses a popup to

deliver the screener questions (below).

Three

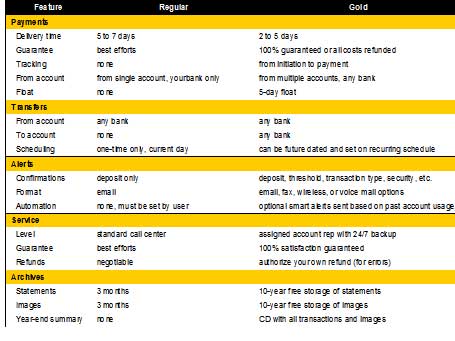

Segment Your Base with Regular, Gold, Platinum, and So

On

We believe that premium channels will be the next big thing in online

banking. That’s why we selected Money HQ from Online Resources

as our top innovation of 2003. A review of the credit card industry provides

clues as to how online banking may play out. American Express was a

segmentation pioneer, rolling out a Gold Card in 1966, only eight

years after the introduction of its standard charge card. After the huge

success of the Gold strategy, widely copied by bankcards in the late 80s,

the company further segmented its card base with the Platinum in 1984—again,

widely copied by bankcards in the mid-to-late 90s. Now American Express

operates a half-dozen card lines: Green, Gold, Platinum, Optima, Delta

SkyMiles, and Blue, with plenty of sub-segments of each.

We expect to see the same thing happen with online banking. Now that

leaders such as BofA, Wells, and Citibank have offered online banking for 15

years or more, and with penetration closing in on 50% of their checking

account bases, the companies will begin offering different versions of their

online programs. Expect to see differentiation around payment capabilities,

credit access, account aggregation, service levels, human attention, and

account alerts (see Table 9, below).

Table 9

Premium Online Banking Offerings

possible features and benefits

Source: Online Banking Report, 2/04

Four

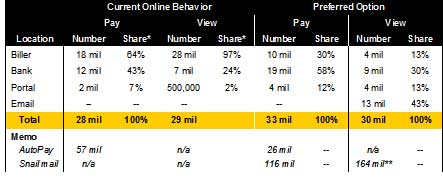

Use Real-time Payments to Drive Users Online

According to Gartner’s latest research,* in the United States, biller

direct payment is used by six million more adults than online bill payment

through a bank, 18 million vs. 12 million. However, according to Gartner,

respondents prefer bank sites for payment by almost two-to-one, 19 million

vs. 10 million, although both options trail preauthorized debit, preferred

by 26 million, and snail mail preferred by 116 million.

Banks can tap into the growing popularity of electronic payments by

offering simpler bill-payment sites that allow users to make one-time

payments or setup preauthorized debits, without a lengthy signup process.

Banks can also win more user by offering more choices, such as paying via

credit card.

Table 10

Bill Payment According to Gartner

millions of U.S. adults paying bills online

Source: EBPP Future Blends Direct Bank Aggregation Models,

Jan 13, 2004, by Avivah LItan, Gartner,

http://www.gartner.com/ $95,

data from survey fielded May 2003

AutoPay = preauthorized electronic debit

*Can choose more than one option, so the sum is higher than 100%

**Total the still wants to receive bills via snail mail

Five

Cross-sell

Credit card issuers have long been far more aggressive than banks

pitching ancillary services, such as credit card registration, credit report

monitoring, and credit insurance. They are beginning to take that approach

to online marketing. For example, last year, Chase’s credit card

group sent me more than 40 sales/service email messages. Issuers have also

found profits selling all types of unrelated products and services from

flashlights to magazine subscriptions. While, we don’t think banks should

start pitching knife sets online, they could be more aggressive in selling

related products, especially credit report monitoring, insurance, and value

investments.

Six

Use Email for Retention

Credit card issuers are much further along in providing email messages to

users. Card companies are using email to remind users of payment due dates,

confirming charges and payments, marketing messages, balance transfer

offers, line increase notifications, credit card check offers, e-statements,

credit report and other ancillary product sales, holiday messages, and other

relation-enhancing messages: even early collection efforts have gone

electronic. Chase is one of the most prolific emailers. During 2003,

we received at least 70 email messages from the bank about our active

credit card account, 46 of the messages (at least the ones we saved), were

marketing/service oriented (see example left) and the other 24 had to do

with scheduling and confirming payment of the bill (see OBR website for more

examples).

Seven

Provide Compelling Online Account Management

Card issuers provide an online experience on par with similarly sized

banks; however, some are becoming more creative with their

account-management websites. For example, American Express offers its

Small Business Dashboard to manage charge card (see screenshot left).

One of its distinguishing features is a credit-status bar that graphically

shows whether the charge account is approaching its limits (e.g., green

means in good standing, yellow means charging privileges at risk,

and red is account suspended).

Card issuers are also making online statements interactive with the

ability to click through to get more information or dispute a charge,

contact the merchant, or re-sort transactions.

Eight

Make Transfers Simple

For several years, companies such as Bank of America

www.easybt.com have

provided simple online balance-transfer solutions for cardholders. Banks too

should make it simple for users to consolidate deposit and loan balances in

a similar manner using account aggregation technology and interbank-funds

transfers. Citibank’s new A2A service and Money HQ from

Online Resources are on the right track.

Nine

Integrate with Direct Marketing

The latest trend is to provide special URLs and/or application numbers

in preapproved snail-mail solicitations so recipients can respond quickly

online. For example, Fleet’s

www.applybizcard.fleet.com

This is a win-win, giving the customer faster direct access to the special

offer and providing an interactive environment for the card issuer to

encourage balance transfers or other upsells. This integrated technique will

quickly become a standard practice for financial direct marketing.

Ten

Get Rid of the Paper

With ever increasing printing and postage costs, the business case for

e-statements continues to grow stronger. Although paper-suppression efforts are

still in their infancy, we expect credit card issuers will be the first to

successfully wean a critical mass of users off paper. Although it will take

years of marketing efforts, for example, we’ve already received eight messages

from Chase encouraging us to switch to a

credit card e-statement; the formula for adoption is relatively simple: