In theory, small and micro businesses represent one of the most lucrative,

and relatively untapped, sources of incremental business. The reality is that

most small and even mid-size businesses are too busy to spend much time changing

banking relationships, unless they are a pre-startup1

and/or shopping for a credit line or loan. As we outlined in OBR 107/108, a

product offering optimized for business will differ somewhat from one built for

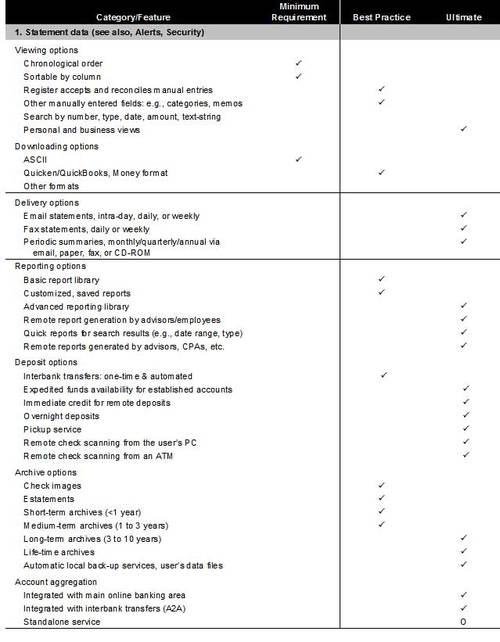

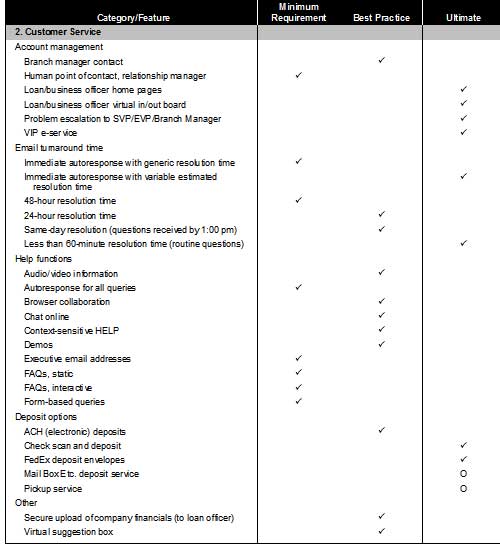

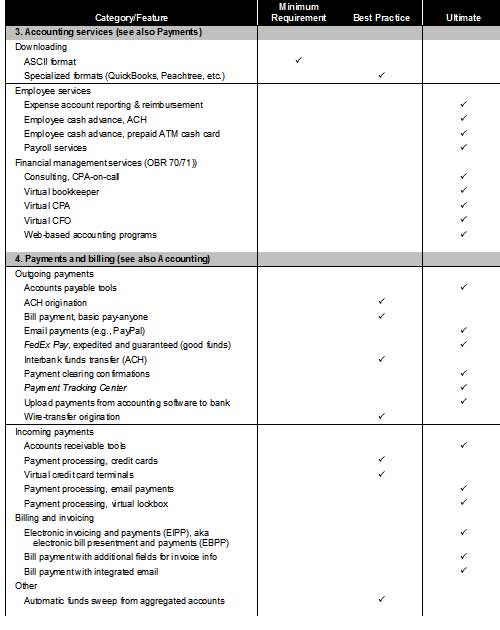

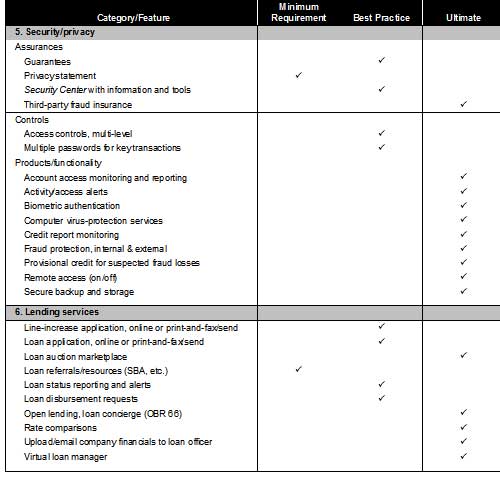

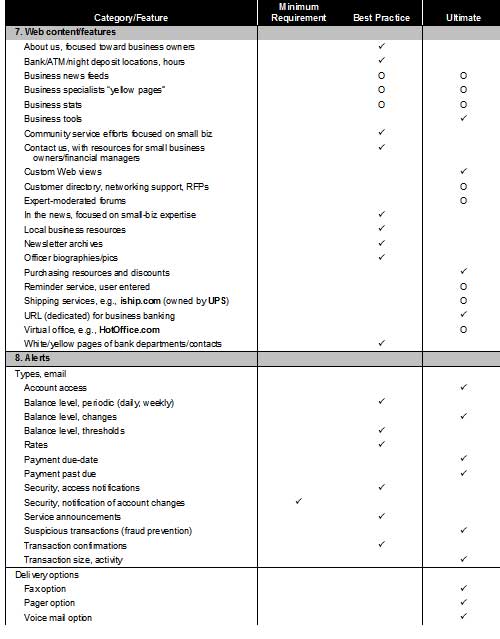

consumers. The following chart summarizes the product options for small- and

microbusinesses. See our prior report for more detail on each feature. The

options are divided into nine categories:

1. Statement data: viewing and organizing balance

2. Customer service: customer care delivered over the Internet

3. Accounting services: financial management tools

4. Payments and billing: e-checks, bill pay, email payments, ACH,

wires, invoicing, card processing

5. Security/privacy: privacy, security, permissions, guarantees

6. Lending: business tools, news, information

7. Website content/features: non-financial tools and information

8. Alerts: email, fax, telephone, and mail activity- and balance-level

alerts

phase. One of the first things an entrepreneur will do is open separate bank

account(s) for a new business venture; it helps keep records straight for

tax-reporting purposes. So it does little good to target any startup, since

most will already have business banking relationships established; you

really need a foot in the door in “pre-startup” mode, when the kernel of an

idea is just forming (see OBR 107/108, for ideas on how to target

pre-startups).

Online Services for Microbusinesses

checkmark = must have feature; R = recommended feature; O = optional feature

Source: Online Banking Report, 9/04 checkmark = must have feature; R =

recommended feature; O = optional feature