This site is operated by a business or businesses owned by Informa PLC and all copyright resides with them. Informa PLC's registered office is 5 Howick Place, London SW1P 1WG. Registered in England and Wales. Number 8860726.

Finovate Blog

Tracking fintech, banking & financial services innovations since 1994

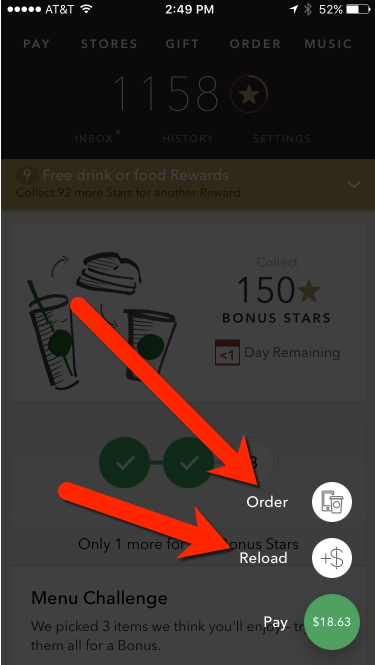

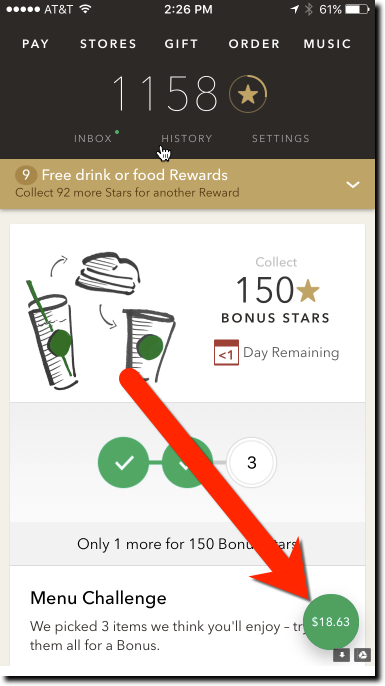

In a major update last week (v4.3.2, 30 Jan 2017), Starbucks added a floating balance to its mobile app main page. So instead of navigating to the pay tab within the app, users always see their card balance as soon as they launch the app. And the balance stays floating in the lower right corner no matter how far down the page you scroll.

Furthermore, clicking the green button grays out the page and brings up two options tethered to the green button (see screenshot below):

Order

Reload

It’s a small thing, but it helps users know before they get to the front of the line whether they have enough funds in their prepaid account. It is also a good shortcut to the card reload function, though I’m not sure how many users will know/remember it’s there.

Bottom line: Banks should make sure that the balance is visible on all areas of their debit card interfaces. It’s an even worse user experience to find out you don’t have the funds after you’ve ordered your meal or rung up your grocery store purchases.

Author: Jim Bruene is Founder & Senior Advisor to Finovate as well as

Principal of BUX Advisors, a financial services UX consultancy.

Email from Starbucks announcing Lyft promo (23 Sep 2013)

Given how many times “coffee” has appeared in my blog titles, you might think I’m obsessed (or addicted). You might be right. Nevertheless, I love the combination of these two important parts of my life, so I’m going to keep on posting. But unlike my last coffee post dealing with the branch experience, today’s subject returns back to my comfort zone, the digital world.

Starbucks recently opened their rewards platform so that third parties could issue Starbucks stars as a reward. The first major brand leveraging this massive platform is ride-sharing service Lyft (promo landing page). In an email today, they offered 125 stars for the first ride (through 9 Nov 2016) plus 5 stars per “morning commute” on an ongoing basis.

Given that 125 stars earns a free item at Starbucks, the Lyft program is essentially a free coffee for the first ride, then one free drink after every 25 morning commutes (e.g., about $0.20 value per ride). That’s probably a little stingy, but with rewards, even small numbers can be motivating. In addition, Starbucks is selling Lyft gift cards in its stores, offering an extra $5 Starbucks card for every $20 Lyft card back. That’s far more generous, but is likely a short-term promotion.

Bank opportunity

With the Durbin-induced death of debit-card rewards, combined with ultra-low interest rates, it’s difficult to find rewards that are affordable and meaningful. But the Starbucks Star has potential, though you have to dole out rewards judiciously.

Let’s assume you can buy stars in bulk for 2 cents each (for major partners, I’m guessing it’s less than that, probably closer to a penny per star). You could incent deposits at 1 star per $10 annually with a balance cap of $5,000 or $10,000. For a $5,000 savings account, the account holder would receive 40 stars per month, enough for a free cup of coffee (or better, a sandwich).

Transaction accounts could provide 5 stars for every debit transaction; 10 for credit card charges; 5 for mobile deposits; 100 for paperless; and so on. That could easily add up to a free drink every month, a meaningful incentive. Perhaps even enough to get a bit of viral lift (aka word-of-mouth).

Yes, it adds costs, but free caffeine is one of the best retention devices on the planet. You already provide free coffee in the branch, why not extend the same courtesy to your digital customers?

—–

Looking for more integrations? Don’t miss our upcoming techfest, FinDEVr, in Santa Clara, 18/19 Oct 2016.

The Starbucks is on us!

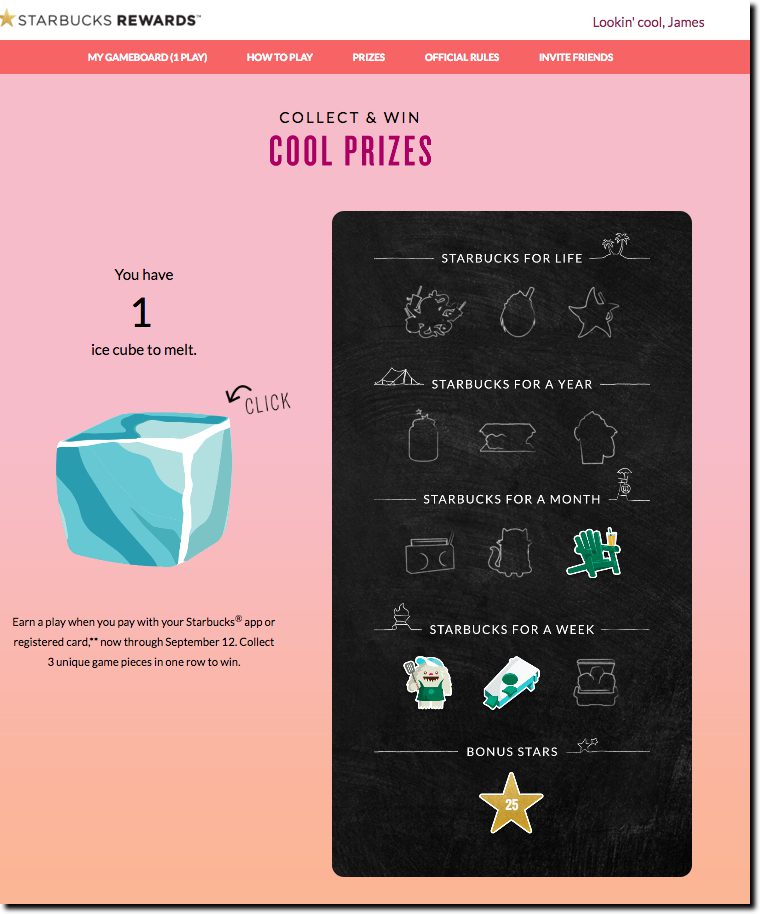

Just when I thought I’d shaken my Starbucks habit after their April devaluation of rewards for my relatively low-cost Americano, they reprised their Starbucks for Life game which last appeared around the year-end holidays. And I’ve been there four days in a row.

Starbucks for Life is no Pokemon Go, but it’s a lot simpler. Customers earn a virtual game piece with every purchase through 12 Sep ’16 (see inset, rules here). In the summer version, it’s an ice cube that melts away with a mouse click to reveal game pieces that fit on a virtual bingo card.

The main prize is free Starbucks for the rest of your life (30 years max). Or you can win a year, month or week’s worth of caffeine as well. And just to keep people interested, there are 2 million 25-star bonuses, which are worth about $0.50 in your chase to a free drink. My only complaint is lack of integration with the mobile app, but I’m sure they’ll get to that next time.

Sweepstakes are a tried-and-true method of encouraging usage, and costwise, they needn’t break the bank. Merchant partners can supply the prizes, and your mobile app provides a low-cost way to amplify the effectiveness with alerts, redemptions, and extra features. And email keeps pulling customers back to the game.

I’d like to earn a game piece with every:

Credit/debit card transaction

Bill payment

ACH debit

Recurring ecommerce transaction (e.g., Uber, Amazon, Apple iTunes, etc)

ATM visit

Customer self-service session

Check reorder

Increase in my savings account balance

Bottom line: Sure, you may not have anything quite as addictive as coffee to maintain interest. But people are pretty happy with free anything, so don’t shy away from gamifying your mobile banking. It’s a marketing tactic that works across a variety of demographics and is flexible enough to support multiple bank goals.

Living in the epicenter of the Starbucks empire, I have followed the caffeine-dispensing giant closely since the beginning. What I would not have guessed 20 years ago, is that it would emerge as a payment pioneer. First, the company was at least five years ahead of its time with gift cards. Now, it’s doing the same with mobile payments/rewards.

And Starbucks continues to innovate. Just this week, the company widened the beta rollout of its remote ordering option, Mobile Order & Pay, to 650 stores in the Northwest. And luckily this includes my home turf in Seattle, so I had a chance to use the service on its first and second day (March 17 & 18).

Here’s my first impressions:

It’s no gimmick: There are real user experience and operational gains. Unlike Apple Pay, or even the Starbucks app, which arguably take longer than a simple credit card swipe, there is a material time saving for the mobile order & payment process. Once your drink order is saved (see screenshot below), it takes only about 15 seconds to order AND pay. Even if there were no queue (unlikely), that’s still a significant time savings over the usual ordering process. And the labor savings over time could be significant, especially in relatively high-wage areas, such as Seattle where the minimum wage is scheduled to move to $15 .

Pushes usage to stored payment credentials: There’s a reason why Starbucks added “Pay” to the name. They clearly like making the payment invisible. In the past, I’ve opted to top up my Starbucks account (via credit card) at the counter, since I was there ordering anyway. Now, I’m going to do all that in the mobile app. Again, another labor savings for Starbucks and an opportunity for issuers to make sure their card is loaded into the Starbucks app, PayPal, or in Apple Pay, since those are all reload options.

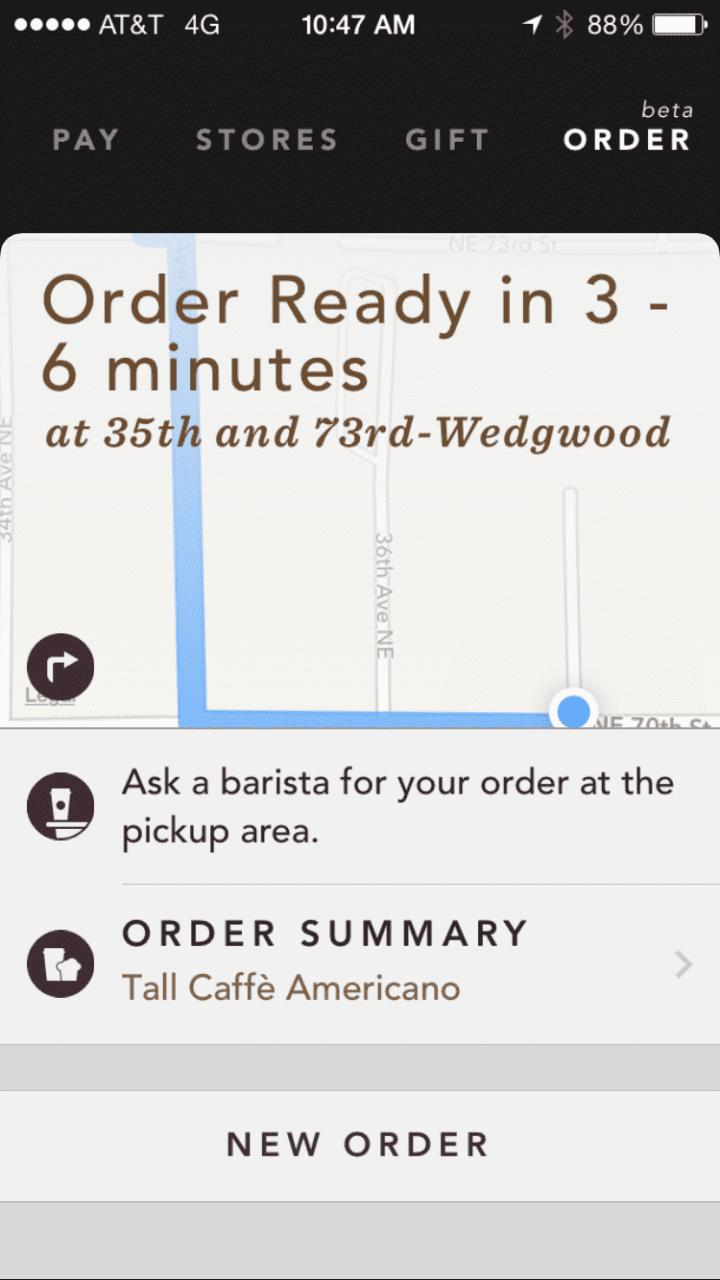

Drives more business: While remote ordering is seen initially as a convenience for existing users, it’s also a powerful tool to drive additional store traffic. In an unfamiliar area, you simply open the orders tab and instantly see the closest store, GPS-guided directions and an estimated time to get there, either walking or driving. A great use of map

Screenshots

The app shows 3-minute window when order will be ready along with driving directions.

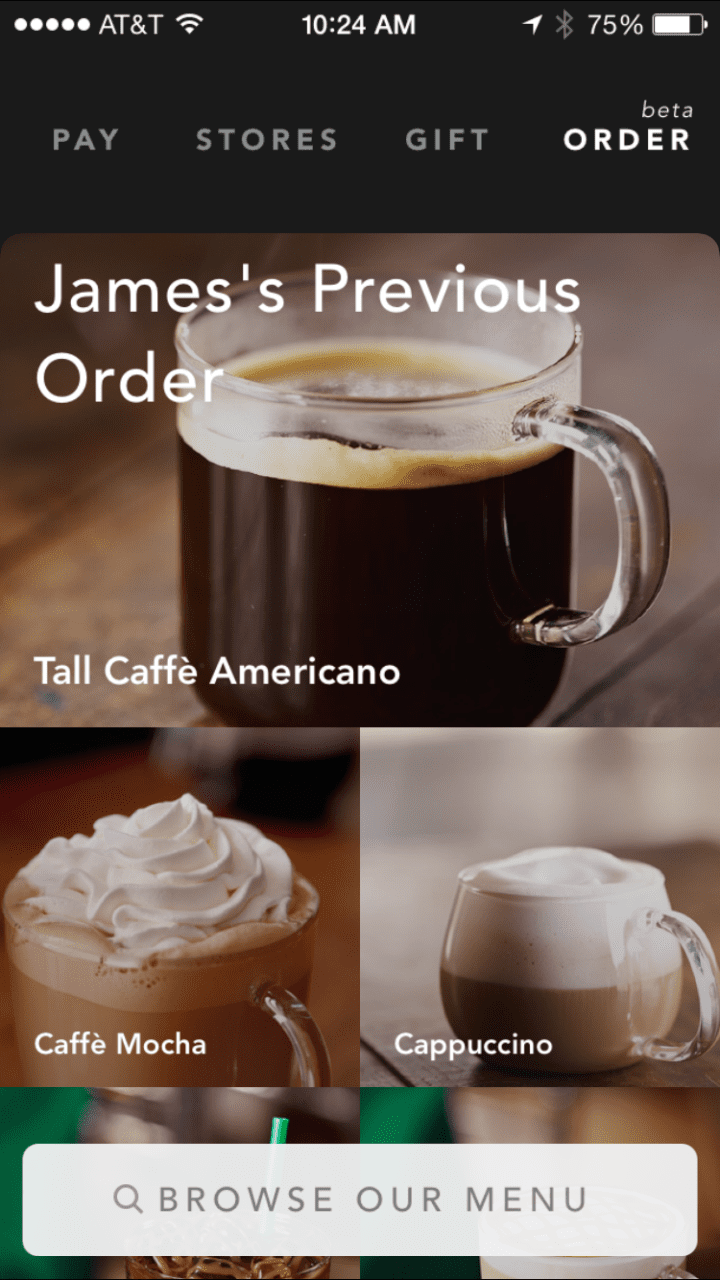

Previous orders are saved in the app for quick reordering.

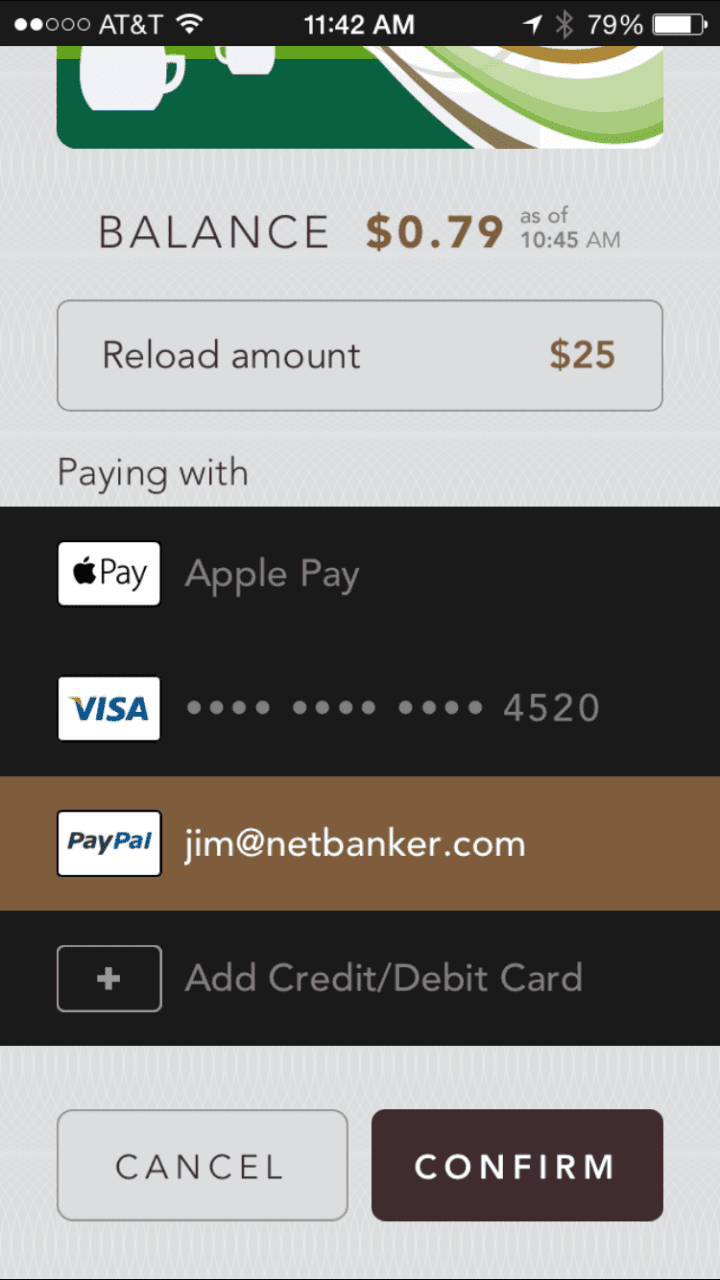

Users can reload the Starbucks mobile app using Apple Pay, PayPal, or credit card

In a major update last week (v4.3.2, 30 Jan 2017), Starbucks added a floating balance to its mobile app main page. So instead of navigating to the pay tab within the app, users always see their card balance as soon as they launch the app. And the balance stays floating in the lower right corner no matter how far down the page you scroll.

In a major update last week (v4.3.2, 30 Jan 2017), Starbucks added a floating balance to its mobile app main page. So instead of navigating to the pay tab within the app, users always see their card balance as soon as they launch the app. And the balance stays floating in the lower right corner no matter how far down the page you scroll.