From the rise of the superapp to financial inclusion 3.0, the insights of our Fintech What’s Hot/What’s Not analysts at FinovateEurope last week continue to artfully disrupt our signature demo-only format.

Mixed in with live demonstrations of the latest innovations in payments and customer engagement (see our Best of Show coverage), our main stage analysts reminded us of the critical differences between machine learning and AI, the opportunities of 5G connectivity, and how open innovation helps companies maximize technological change.

Does the rise of the super app in Asia anticipate the future of apps in the West? Ratna Sita Handayani, Senior Research Manager with Euromonitor International, looked at the rapid growth in mobile payments in Asia, and the way that companies outside of traditional financial services such as ridesharing firm Grab have moved effectively into the payment space. Highlighting similar accomplishments from Japanese social media giant LINE and the continued rise of AliPay, Handayani considered how hyperlocalization and other strategies are helping these new offerings gain ground.

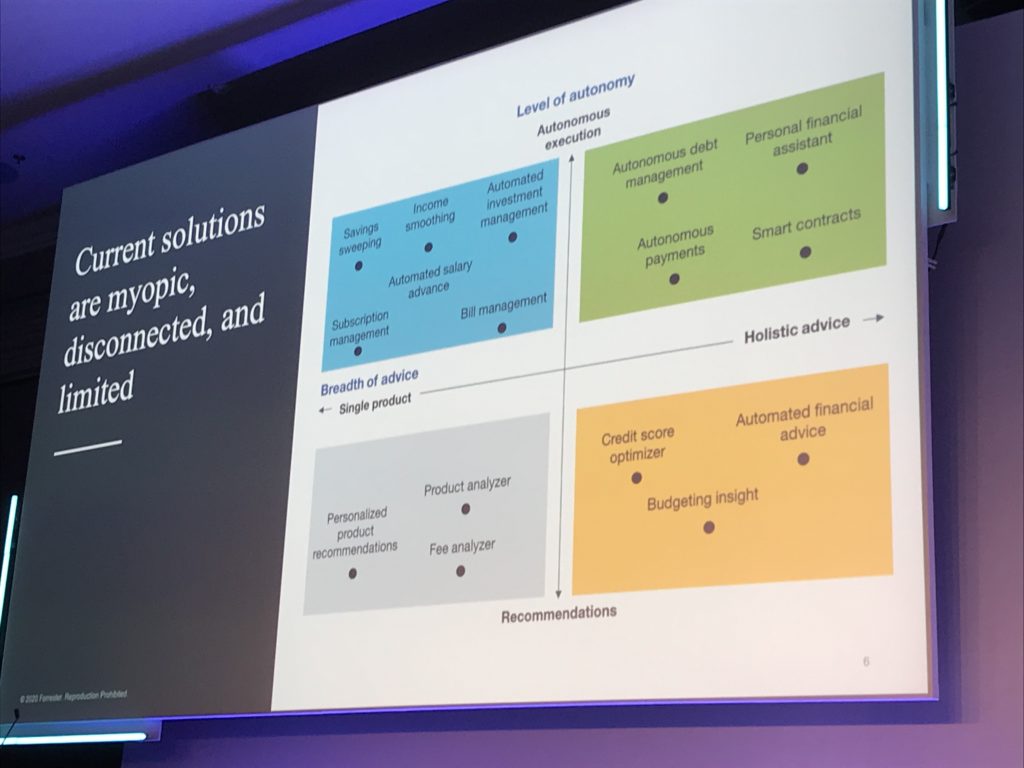

Promoting a “more autonomous, more distributed, and more ethical” fintech industry, Forrester VP and Research Director Oliwia Berdak encouraged innovators to move from thinking about the “next best product” to a value-for-value exchange in which interests align. Berdak compared many of the more limited fintech offerings of today with solutions such as smart contracts and even autonomous debt management that more fully take advantage of the latest technologies like advanced machine learning.

This is necessary in large part, Berdak suggested, to help manage the cognitive load of all the information that technology delivers in the first place. In other words, we need technology to “take the human” out of the technological equation we’ve created.

Tosin Agbabiaka, an Early Stage Investor with Octopus Ventures, leveraged his own experience – from frontier through the periphery to an increasingly divided developed world – to paint a vivid portrait of Financial Inclusion 3.0. Agbabiaka provided a deep, nuanced understanding of the challenges of developing countries like Nigeria in the 1990s where basic financial access was a principal obstacle to progress (Financial Inclusion 1.0). He then explained the difficulty periphery nations have when boom times stall and a lack of liquidity threatens to turn financial crises into catastrophe – like Greece in the late 2010s (Financial Inclusion 2.0).

If the first stage of financial inclusion is about optimizing for basic access, and the second stage is about optimizing for quality and efficiency, as Agbabiaka indicated, the third stage of financial inclusion is about optimizing for affordability. This is the world we see in North America and Europe where the benefits of a digital, interconnected economy exist in abundance, but are harder for a growing number to obtain. These are places characterized by gig economics and alternative financing in response to low wages, funding challenges for micro- and small businesses, and the debt burden of higher education.

This is a critical challenge for fintech, Agbabiaka suggested, but it is not a challenge that needs to be pursued out of a sense of social good alone. Financial inclusion 3.0 represents the union of access, quality, affordability and, to coin a phrase used by another analyst above, aligns the interests of the frontier, the periphery, and the center when it comes to technological innovation. In this world, as Agbabiaka explained, “those served benefit as much as the newly-served.”