Apple today introduced its latest invention, a gigantic $499 iPod Touch called the iPad (inset shows iPad, Kindle, vs. iPhone; note 1).

Apple today introduced its latest invention, a gigantic $499 iPod Touch called the iPad (inset shows iPad, Kindle, vs. iPhone; note 1).

It’s a gorgeous piece of technology that will soon be the movie-watching, ebook-reading device of choice for the rich and famous. But what does it mean for the average financial institution?

Tactically, it should have almost zero impact. Your iPhone/iTouch app should work pretty much the same on the iPad. There may be some design tweaks your programmers will need to understand, but the basic functionality is the same.

It would make a wonderful giveaway item, either as part of a high-end business/private banking package (note 2), or as a sweepstakes prize.

So those of you who already have an iPhone app launched, or in the pipeline, can stop reading now. But read on if you haven’t yet hopped on the app bandwagon.

___________________________________________________________________________

The movement to apps, and away from old-school “browsing,” is unstoppable. The iPad joins a growing list of new devices (Android, Kindle, etc.) that are app-primary, browser-secondary (note 3).

It’s a massive shift that’s happened in less than two years, beginning in July 2008 when Apple opened the iPhone platform.

The popularity of apps is changing how users tap online info. Even power laptop/desktop users are making dramatic changes in their information consumption. For example, within a few months of the Apple app store launch, I had already moved 12 of my routine info-gathering tasks to the iPhone. The speed/convenience of pressing a single button vs. navigating to a website via the browser is a significant improvement in user experience. More than a year later, my habits have changed little.

The change from serving customers who were “online browsers” and are now “mobile app users” has profound implications for banking. Instead of talking to your customers in batch- mode with built-in time delays, you are now real-time, feeding data to customer on the go, where they need up-to-the-minute status on their cash situation.

In many ways, the ROI for real-time banking (and here) is more dramatic than online-batch banking. The ability to stamp out POS fraud, to nip budding customer service nightmares, and just plain get closer to the customer, all bring nice returns on the mobile investment (note 3).

Notes:

1. Photo credit: TechCrunch post today.

2. For more info on using a dedicated device for small business customers, see our October Online Banking Report.

3. Groundswell author and Forrester analyst Josh Bernoff calls this the “splinternet.”

4. For more info on financial services opportunities on the iPhone, see our March Online Banking Report.

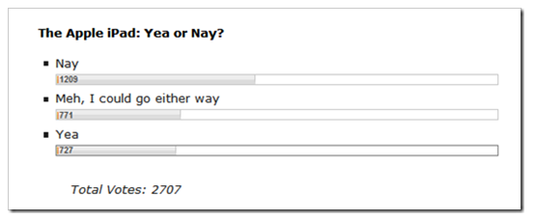

5. Initial response online was mixed, 2,700 readers of CrunchGear, voted “thumbs sideways” today (link, results at 4PM Pacific below)