Online banking usage

Up until a few years ago, small business usage of online banking trailed

consumer adoption. In late 2000, 13% of small and microbusinesses used

online banking compared to 16% of consumers . Three years later, online banking penetration is similar to that of

consumers, an estimated 30% overall. At the largest small businesses, those

with sales between $5 and $10 million, usage is now more than 40%, double

the rate three years earlier.

It’s likely we’ll see continued rapid growth for a few more years. Almost

all (99%) small businesses are computerized, either at the business or at

the owner’s home, or both (see Table 18, above) and more than 75% are

using their personal computers for financial activity (see Table 21, next

page). It’s only a matter of time before the majority of small

businesses bank online. Looking at the 7.3 million small and microbusinesses

universe, we predict that we’ll pass the 50% penetration point within four

years. However, we may reach that point much sooner. One researcher,

Synergistics Research, is already saying that online banking usage

has passed the 50% mark in the $100,000- to $10-million segment, with the

largest small businesses

($5 to $10 million) topping out at 75% penetration.

Table 21

Small business online and PC financial services usage,

2002

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use

Reasons for not banking online are typical, with security and

inconvenience (compared to current methods) the most-cited reasons (see

Table 22, below). Only 8% mentioned it was too expensive and only 5%

said they didn’t have the necessary equipment (presumably convenient online

access).

Table 22

Reasons for not conducting either business banking or

investing online

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use

Table 23

Online banking, billing, payment and other online activities

Q. Does your company use the Internet …?

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use, April 2003

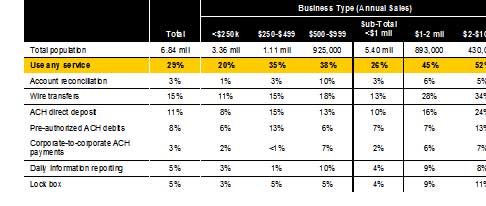

Table 24

Cash Management Usage

Q. Please indicate if the service is

used?

Source: NFO Financial Services Group SOHO/Small Business Owner 2002

Online and Channel Use, April 2003

Advisor usage

While small businesses still turn to their banker for loan

advice, only 17% use a banker for cash management advice, and just 4% for

retirement planning (see Table 25, below). Because small businesses are

skeptical of bankers’ expertise in non-traditional areas, banking organizations

must first explain why they are selling the product, and why the bank’s solution

is superior to more traditional sources. It may be advantageous to partner with

brand names that are more closely associated with the non-traditional product,

e.g., Safeco for business insurance.

Regardless of the channel the customer chooses to get

information and make transactions, a human is usually needed to close the sale.

In a recent Synergistics Research survey of 600 small businesses, only 7% had

opened bank accounts remotely (see Table 26, below). The sales process

can be assisted by email and phone with a branch manager, business banking

officer, or a special small business liaison.