Seventeen years ago PayPal took on Wells Fargo’s Billpoint (joint venture with eBay) and Citibank’s (C2IT) fledgling P2P payment services. It wasn’t a fair fight. With a $400 million VC war chest and an all-star exec team (Elon Musk, Peter Thiel, Max Levchin, David Sacks, Reid Hoffman and so on), the fight didn’t make it past the first round. Within a year PayPal had a stranglehold on eBay payments due to its superior UX and aggressive business model.

Seventeen years ago PayPal took on Wells Fargo’s Billpoint (joint venture with eBay) and Citibank’s (C2IT) fledgling P2P payment services. It wasn’t a fair fight. With a $400 million VC war chest and an all-star exec team (Elon Musk, Peter Thiel, Max Levchin, David Sacks, Reid Hoffman and so on), the fight didn’t make it past the first round. Within a year PayPal had a stranglehold on eBay payments due to its superior UX and aggressive business model.

Now the banks are back with Zelle, a rebranded version of the clearXchange that has been up and running for six years. The service already has great traction. In 2016, Early Warning, the bank-owned operator (see note 1), processed 170 million transfers totaling $55 billion for the 85 million customers of their big-bank owners. That works out to exactly 2 transactions per customer annually with an average of $320 per transfer.

The value transferred is three times the size of Venmo’s $17.6 billion in volume, though the number of Venmo transactions is probably higher, perhaps considerably higher if its average transaction size is in the $15 to $20 range implying 1 billion venmos last year.

Using Zelle

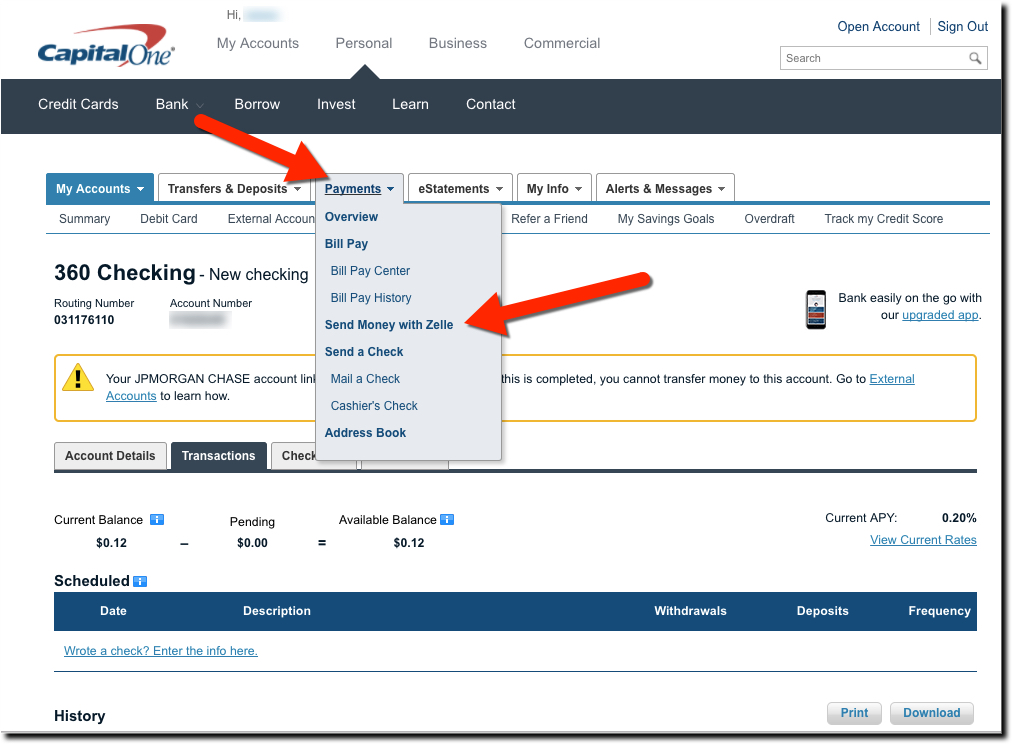

Yesterday and today I used the mobile and desktop Zelle from Capital One for the first time. Other than the glitch with my mobile phone number (see note 3), which would stop many consumers from going further, setup was quick and easy. The desktop version is pretty straightforward, with a Send Money with Zelle link in the middle of the Payments menu (see screenshot below). This assumes you know what Zelle is, or you just ignore it since it comes after the key words, “Send Money.”

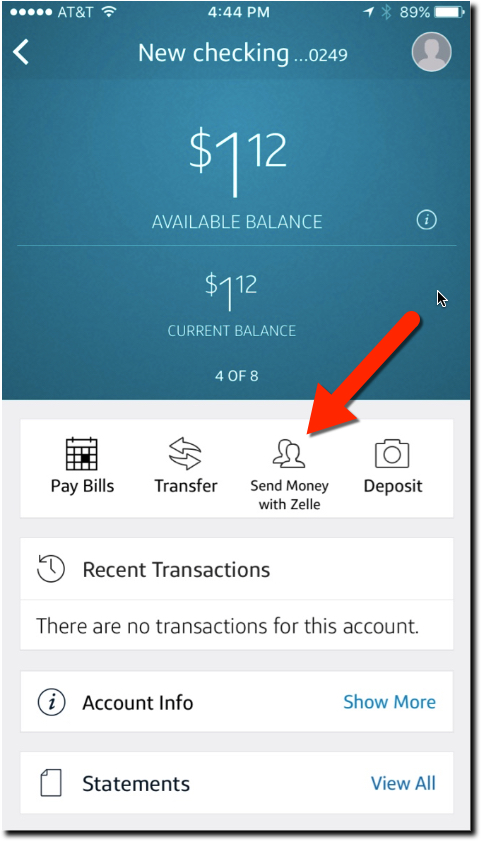

But the mobile UI is less intuitive. It wasn’t initially obvious how to use it because there is no Zelle or payments navigation item in the Capital One app…yet (it’s only been out since June 12). However, once you go to your checking account section, it’s one of the main navigation items at the top (see inset below).

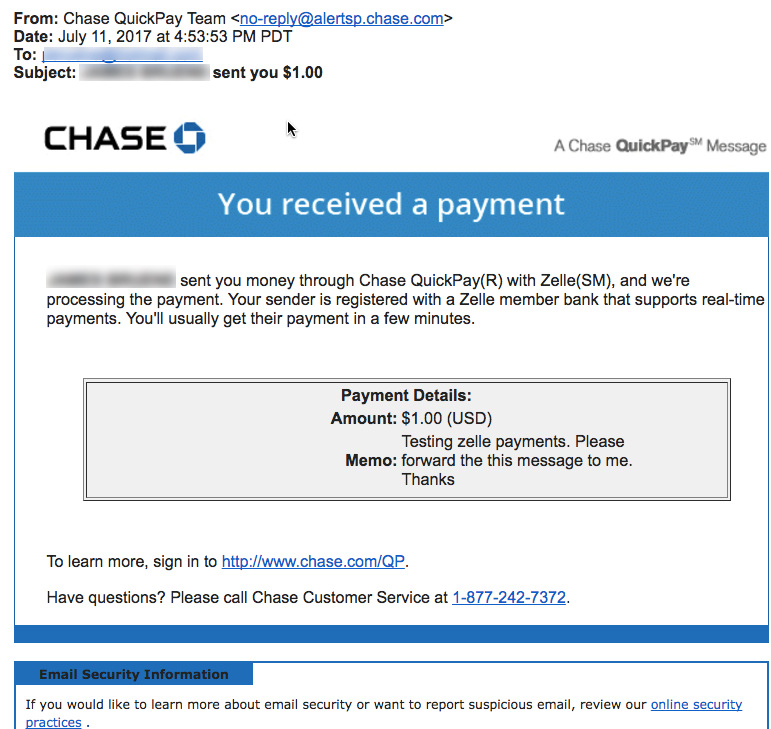

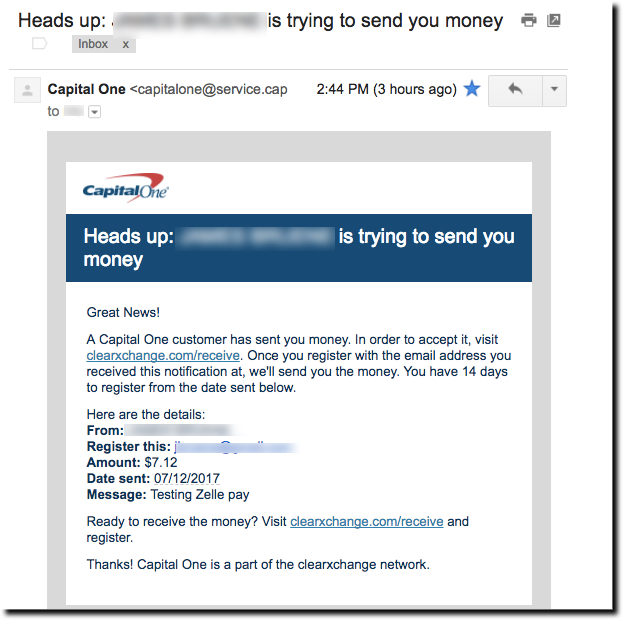

I was initially surprised at what happened with my test payment. I sent a buck to my son (sorry, Paul I only had $1.12 in my account) and I was pleasantly surprised to find that my payment had been “qualified for expedited deposit” and he’d have the cash right away without the usual ACH delay.

But when my son forwarded the email he received, I was surprised to find that my Capital One payment has morphed into a branded Chase QuickPay with Zelle. There was no mention of Capital One anywhere in the message (see screenshot #1).

That makes sense now. My son has a Chase account and was already registered with Chase QuickPay. If he’d not already been registered, he would have received a Capital One branded email (see screenshot #2 below).

Why the new brand?

Zelle/clearXchange will continue to grow at a good clip if its big-bank owners stick with it. It’s already 3x the size of media darling Venmo (owned by PayPal). But I’m not sure the massive investment in creating a new payments brand is worthwhile (cut to the boardroom discussion of a 2018 Super Bowl ad).

I get that they are trying to create another Visa/Mastercard network that consumers recognize and trust. But unlike credit transactions at the POS in the 1950s and 60s, p2p payments are relatively understood by consumers and have much less need of a third-party organization to achieve the network effects. The big banks are already wired to each other and what’s needed, what clearXchange was already offering, is just a simpler UX inside each bank’s online and mobile application. Adding the Zelle name to the mix seems like a step backwards on that front.

Maybe I’m wrong and we’ll all be Zelling money to Mars in a few decades. But I’m not convinced the new brand will stand the test of time.

Bottom line: Love the service, which I expect to flourish, but confused by the branding.

#1: Email to a pre-registered Zelle recipient banking at Chase

#2 Email to a Zelle recipient not registered with a participating bank

Author: Jim Bruene is Founder & Senior Advisor to Finovate as well as Principal of BUX Advisors, a financial services user-experience consultancy.

Notes:

- Owners of Early Warning (aka Zelle) are: Bank of America, BB&T, Capital One, JPMorgan Chase, PNC, U.S. Bank, and Wells Fargo.

- If I were any bank other than BofA and Capital One, I’d be crying foul over how the banks are listed in alphabetic order. On the desktop, it doesn’t matter (yet) since they are all above the fold. But on mobile, you can only see BofA and Capital One, and there is no indicator that you should scroll for more.

- I received a fatal error message when I tried to use my mobile number as contact to send Zelle payments (see inset) from Capital One’s mobile app. This could be something particular to my account, but from the cryptic popup message, it sounds like my phone is registered at another bank. And that would be a big concern for most customers who would fear that identity thieves are hard at work draining their accounts.

- Image credit